TL;DR:

- Building lasting wealth in Australia depends on deliberate, long-term decisions across assets, tax, and investments, rather than high income alone. Genuine wealth is sustainable asset growth that provides security, choice, and resilience beyond working years, emphasizing compounding, low costs, and tax efficiency. A disciplined mindset, avoiding lifestyle creep and emotional responses, ensures wealth accumulation; leveraging tools like AlphaIQ can help model and optimize your strategy confidently over time.

Building lasting wealth in Australia is less about earning a high salary and more about making deliberate, sustained decisions across superannuation, investments, property, and tax over many decades. Many self-directed investors aged 35 to 65 find themselves asset-rich but strategically uncertain, unsure whether their current portfolio choices will actually deliver the security and flexibility they want in retirement. This guide cuts through that confusion by explaining what long-term wealth really means, which mechanisms drive it, and how you can structure a personal plan that holds up over time.

Table of Contents

- Defining long-term wealth: what it really means

- The drivers of long-term wealth: compounding, asset selection and discipline

- Comparing major strategies: equities, ETFs and property

- Avoiding common pitfalls: taxes, debt and lifestyle inflation

- Putting it together: building your personal long-term wealth plan

- The uncomfortable truth about wealth: why mindset trumps tactics

- Supporting your long-term wealth journey with the right tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Wealth is more than income | True long-term wealth is about sustainable asset growth and financial security into retirement. |

| Compounding unlocks growth | Unrealised gains and disciplined reinvestment build substantial wealth over decades. |

| Asset choice matters | Diversifying between shares, ETFs, and property provides resilience and growth potential. |

| Avoid common pitfalls | Tax leakage, lifestyle creep and debt often erode wealth without consistent discipline. |

| Mindset drives success | Long-term focus and the right financial habits ultimately determine your wealth journey. |

Defining long-term wealth: what it really means

With that context, it is crucial to properly define long-term wealth so you can evaluate your own position. Most people conflate wealth with income or consumption. A high salary feels like wealth. An expensive car feels like wealth. But neither produces lasting financial security unless it is channelled into productive assets that grow and compound over time.

Long-term wealth is best understood as sustainable asset growth that outlasts your working years. It is the capacity to fund your lifestyle, weather unexpected costs, and retain meaningful financial choices well into and beyond retirement, without being dependent on employment income. That definition shifts your focus from what you earn to what you keep and grow.

A few important outcomes distinguish genuine long-term wealth:

- Security: assets sufficient to fund your lifestyle without relying on employment

- Choice: the flexibility to retire early, change careers, or support family when needed

- Resilience: a financial position that can absorb setbacks like illness, market downturns, or property vacancies

One of the most damaging forces working against this outcome is lifestyle creep, the gradual expansion of spending as income rises. If every pay rise is absorbed by a bigger mortgage, a newer car, or more expensive holidays, net wealth barely moves. Poor tax settings compound the problem. Many investors miss the fundamentals of wealth optimisation principles and hold assets structured in ways that generate unnecessary tax, reducing the compounding base over time.

"Long-term wealth is not just about high income — you must avoid lifestyle creep, tax leakage, and excessive consumption."

A useful mental framework here is the Forever Test: only choose assets you would be genuinely happy to hold past age 60. If you would not want the ongoing costs, management burden, or illiquidity of an asset in retirement, think carefully before acquiring it now. Applying this test to each financial decision helps filter out noise and keeps your portfolio aligned with your actual long-term goals. Reviewing wealth management best practices can also sharpen your understanding of which strategies genuinely hold up over decades.

The drivers of long-term wealth: compounding, asset selection and discipline

Understanding the definition is one thing; now, let us clarify the specific ingredients that allow long-term wealth to flourish. The mechanics behind sustained wealth creation are well understood, even if they are under-appreciated in practice.

The four core drivers of long-term wealth are:

- Compounding: returns generated on previous returns, which accelerates growth exponentially over time

- Low-cost investing: minimising fees and transaction costs, which silently erode wealth over decades

- Tax efficiency: structuring assets and income to reduce the proportion lost to tax at each stage

- Protection from lifestyle inflation: keeping consumption growth below income growth, consistently

Compounding deserves particular emphasis. A portfolio earning 8% per annum doubles roughly every nine years. At that rate, $200,000 at age 40 becomes approximately $800,000 by age 58, without a single additional dollar invested. The catch is that compounding requires patience and discipline. Every time you sell and switch assets, you interrupt the process, trigger a potential capital gains tax (CGT) event, and reset the compounding clock.

This is why efficient wealth building strategies consistently point toward the same habit: hold quality assets for the long term and resist the urge to trade in response to short-term market noise.

"Investors should prefer unrealised capital growth over income for compounding to reduce tax drag."

Capital gains are also more tax efficient than dividends or rental income for most investors. Unrealised gains incur no tax until an asset is sold. If sold after 12 months, the 50% CGT discount applies for individuals. Dividends and rental income, by contrast, are taxed at your marginal rate in the year they are received. Structuring your portfolio to favour growth assets where possible, particularly inside superannuation, is one of the most reliable ways to reduce tax drag over a long investment horizon.

Pro Tip: Automate your regular investment contributions to a low-cost index fund or ETF portfolio. Removing the decision from your hands each month protects you from emotional market timing and keeps compounding uninterrupted. Consider reviewing wealth intelligence strategies to identify where automation and tax efficiency can work together in your situation.

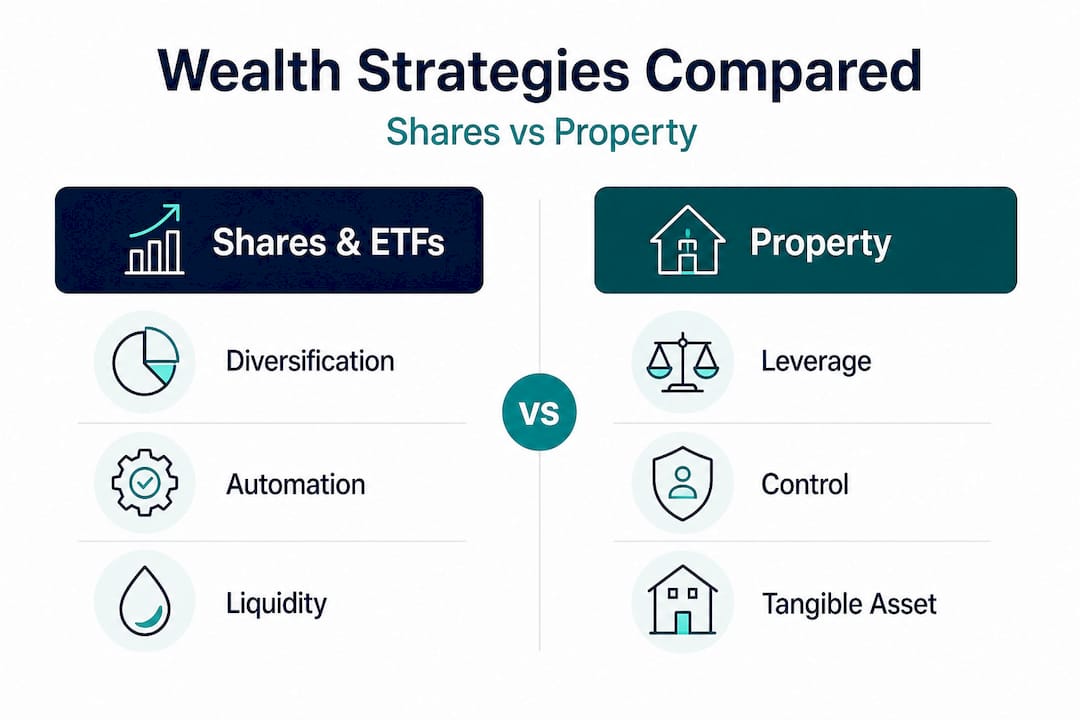

Comparing major strategies: equities, ETFs and property

Armed with an understanding of the drivers, let us compare the most common frameworks Australians adopt for wealth building. The three dominant approaches are direct equities (individual shares), exchange-traded funds (ETFs), and direct property. Each has distinct advantages and trade-offs.

| Feature | Shares and ETFs | Direct property |

|---|---|---|

| Diversification | High (especially ETFs) | Low (single asset) |

| Effort required | Low to moderate | Moderate to high |

| Liquidity | High | Low |

| Leverage available | Limited (margin loans) | High (mortgage) |

| Tax efficiency | High (CGT discount, franking) | Moderate (depreciation, CGT) |

| Entry cost | Low | High |

| Ongoing costs | Low | High (rates, maintenance) |

As the data confirms, shares and ETFs offer low-maintenance diversification while property provides leverage but comes with higher effort and illiquidity. Neither is universally superior. The right choice depends on your time horizon, available capital, tax situation, and personal preference for involvement.

A lazy portfolio, typically a three-ETF structure covering Australian equities, international equities, and bonds, is an elegant solution for investors who want broad exposure without complexity. You invest in three funds, rebalance annually, and let compounding do the work. For investors who want slightly more control, a core-satellite strategy pairs a low-cost ETF core (70 to 80% of the portfolio) with targeted satellite positions in specific sectors or assets.

Age plays a significant role in asset selection. Consider understanding asset allocation explained for your life stage:

- Ages 35 to 45: higher growth exposure (70 to 100% equities) makes sense given a long time horizon and capacity to absorb market volatility

- Ages 45 to 55: gradual shift toward balanced allocations (60 to 70% growth) as retirement becomes more concrete

- Ages 55 to 65: capital preservation becomes more important, though maintaining meaningful growth exposure remains essential to fund a 25 to 30 year retirement

Pro Tip: Review property investment tips if you are considering adding or adjusting property in your portfolio. The decision should factor in your existing tax position, available equity, and how property fits your Forever Test criteria. Also review investment strategy examples to see how other Australians in similar situations have structured their approach.

Avoiding common pitfalls: taxes, debt and lifestyle inflation

No matter how robust your plan, certain recurring mistakes can derail even the best efforts. Let us break these down clearly so you can recognise them before they take hold.

High earners often lose wealth through taxes, debt, and lifestyle creep. This is one of the most counterintuitive findings in personal finance. A household earning $300,000 per year can end up with less wealth at 60 than one earning $120,000, if the higher earners consistently spend more, carry consumer debt, and hold assets in tax-inefficient structures.

The most common wealth-eroding pitfalls include:

- Tax drag: holding growth assets in personal names at high marginal rates when a trust, company, or super structure would be more efficient

- Consumer debt: credit cards, car loans, and personal loans at 10 to 20% interest rates that absorb money which could otherwise compound

- Lifestyle inflation: upgrading housing, cars, and travel every time income rises, preventing meaningful savings rate improvement

- Inaction on super: not making voluntary super contributions during high-earning years and missing the benefit of the low 15% tax rate inside super

Here is a simplified illustration of how these factors affect a $500,000 portfolio over 20 years at 8% gross return:

| Risk factor | Annual cost | Portfolio impact over 20 years |

|---|---|---|

| Tax drag (extra 15%) | ~$6,000 | Reduces end balance by ~$275,000 |

| Consumer debt (at 15%) | ~$3,000 | Reduces investable base by ~$138,000 |

| Lifestyle inflation (1% extra spend) | ~$5,000 | Reduces savings contribution by ~$229,000 |

The numbers are stark. Small, persistent leaks add up to hundreds of thousands of dollars in foregone wealth. Reviewing wealth platforms for Australians can help you model your own numbers with precision, rather than guessing at the impact.

A practical checklist to protect your wealth from these risks:

- Consolidate and eliminate consumer debt before prioritising discretionary investing

- Review your asset ownership structure (personal, trust, super) with tax outcomes in mind

- Set a fixed savings rate target (e.g., 20 to 30% of take-home pay) and automate transfers

- Avoid increasing lifestyle spending until surplus is first directed to wealth-building assets

Learning from wealth planning strategies used by other Australians in similar income brackets can also reveal blind spots in your own approach.

Putting it together: building your personal long-term wealth plan

Now, let us put these ideas into practice by outlining a simple, actionable roadmap you can follow. A long-term wealth plan does not need to be complicated. It needs to be honest, consistent, and regularly reviewed.

Follow these steps to create a workable plan:

- Define your time horizon: how many years until you want to retire or gain financial independence? This drives every other decision.

- Assess your current position: list all assets, liabilities, super balances, income streams, and current savings rate

- Select your asset strategy: apply the Forever Test to each existing and planned asset. Would you hold this past age 60?

- Optimise for tax: consider whether current asset structures (personal, trust, company, super) are delivering the best after-tax outcomes

- Automate contributions: set up regular transfers to investment accounts and salary sacrifice contributions to super

- Schedule annual reviews: reassess allocation, balance contributions, and adjust as your life stage or tax situation changes

As noted in the Forever Test framework, you should only own assets you would be happy to hold past age 60. Applying this consistently clears out speculative positions and keeps your portfolio focused on durable, compounding assets.

Key considerations as you approach retirement:

- Gradually transition to a more conservative allocation, but do not abandon growth assets entirely

- Maximise concessional super contributions in the years before preservation age (currently 60) to benefit from low tax rates

- Model your projected retirement income using tools designed for investment options for pre-retirees

- Consider whether a bucket strategy (separating short, medium and long-term funds) suits your income needs

The uncomfortable truth about wealth: why mindset trumps tactics

Having mapped out the action steps, it is time for a hard truth: strategy means very little without the right mindset behind it.

Every experienced investor has encountered the temptation to abandon a long-term plan for something shinier. Cryptocurrency in 2021. Speculative mining stocks. Micro-cap growth plays that friends swear by. The pattern is consistent. The investors who build genuine long-term wealth are rarely the cleverest or the most active. They are the most patient.

As the evidence consistently shows, time horizon matters more than clever tactics. Discipline and the ability to avoid lifestyle creep are the true differentiators in long-term wealth outcomes. You do not need a more sophisticated strategy. You need the psychological ability to stick with a straightforward one.

This means confronting three specific mindset traps:

FOMO (fear of missing out) drives investors to chase recent winners, often buying high and selling low. The antidote is a written investment policy statement, a simple document that defines what you invest in, why, and under what conditions you would change course.

Lifestyle expansion is the quiet enemy. Each upgrade feels reasonable in isolation. The new kitchen, the private school fees, the European holiday. But the cumulative effect is a savings rate that stagnates regardless of income growth. Ask yourself annually whether your lifestyle spending is growing faster than your wealth.

The pursuit of "more" over "enough" is perhaps the most overlooked trap. Many investors continue taking on excess risk or complexity well past the point where they have already won. Knowing when you have reached a position of genuine security and defending it is a form of financial intelligence that wealth management best practices rarely discuss, but it matters enormously.

The investors who reach retirement with genuine freedom and options are typically those who mastered these basics, not those who found a sophisticated edge.

Supporting your long-term wealth journey with the right tools

To confidently take the next step in building long-term wealth, leveraging smart digital tools makes the journey easier and more effective. Knowing the principles is one thing; seeing the real numbers in your specific situation is another entirely.

AlphaIQ is an Australian personal wealth intelligence platform built for self-directed investors who want to model and optimise their financial position across investments, superannuation, property, and retirement. The platform combines tax-aware financial modelling with scenario simulation, so you can see the impact of decisions before you make them. Whether you are testing the effect of extra super contributions, modelling a debt recycling strategy, or projecting your retirement income, AlphaIQ delivers clarity grounded in real numbers. Explore the platform at alphaiq.pro and take control of your long-term wealth with confidence.

Frequently asked questions

What types of assets are best for long-term wealth in Australia?

Diversified shares, ETFs, and suitable property can all build wealth over time. The right blend depends on your age, risk tolerance, and time horizon, with shares and ETFs offering low-maintenance diversification and property providing leverage with higher management requirements.

How important is compounding for long-term wealth?

Compounding is the single most powerful mechanism for growing wealth over decades, magnifying returns on top of previous returns. Minimising tax drag by preferring unrealised capital growth is essential to keeping compounding working at full force.

How can high income earners avoid losing wealth in the long term?

By limiting tax leakage, eliminating consumer debt, and keeping lifestyle inflation in check, high-income earners can retain and meaningfully grow wealth. Research confirms that high earners leak wealth through taxes, debt, and lifestyle creep more often than lower earners realise.

Is property or shares better for building wealth in Australia?

Both can be highly effective depending on your circumstances. Shares and ETFs suit investors seeking low-maintenance diversification, while property suits those comfortable with leverage and higher ongoing management, each with its own tax and risk profile.

Recommended

- Wealth management best practices for Australian investors

- Personal wealth optimisation: 5 steps to maximise assets

- Why tax-aware investing maximises your wealth in Australia

- Smart property investment tips: retire with 3–5 assets

- HODL: The Long-Term Crypto Strategy That's Here to Stay - Tickerly

- Demivolt | News – How to spot (and avoid) the old tricks of the real estate game