TL;DR:

- Wealth optimisation involves structuring investments to maximize net returns after fees and taxes.

- Key pillars include asset allocation, tax efficiency, cost control, rebalancing, and goal alignment.

- Continuous review and disciplined habits are essential for lasting wealth growth regardless of asset size.

Most self-directed investors assume wealth optimisation is reserved for those with millions in the bank or a dedicated family office. That assumption is costing ordinary Australians real money. Wealth optimisation is simply the practice of structuring your investments, superannuation, and property so they work together as efficiently as possible, after fees and after tax. Whether you hold $200,000 or $2 million across various assets, the principles remain the same. This guide breaks down what wealth optimisation actually means, the core pillars behind it, how it works in practice, and the most common mistakes to avoid as you build a stronger financial position.

Table of Contents

- What is wealth optimisation?

- The key pillars of wealth optimisation

- How wealth optimisation strategies work in practice

- Common mistakes and how to avoid them

- Our perspective: Why true wealth optimisation is about mindset, not products

- Optimise your wealth with smart tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Optimisation is accessible | Any investor can apply optimisation, not just high-net-worth individuals. |

| Core pillars matter | Efficiency, tax strategy, cost minimisation, and asset allocation are key for wealth growth. |

| Avoid common mistakes | Ignoring fees and taxes can undermine returns—stay disciplined and review regularly. |

| Tools can help | Technology and platforms make optimisation easier and more effective for all investors. |

What is wealth optimisation?

Wealth optimisation is often confused with wealth creation, speculation, or simply "getting richer." In reality, it's a far more deliberate and structured activity. Wealth optimisation is a structured process to maximise financial outcome across assets, meaning you're not just focused on return, but on how efficiently that return reaches your pocket after all costs are stripped away.

Think of it this way: two investors each earn 8% on their portfolios. One pays 1.5% in fees, holds assets in the wrong structure, and triggers unnecessary capital gains events. The other minimises fees, uses tax-advantaged accounts, and plans disposals strategically. Over 20 years, the second investor finishes significantly ahead, without taking any extra risk.

For Australian self-directed investors, optimising personal assets goes well beyond picking better stocks. It involves:

- Asset allocation: Distributing investments across growth, income, and defensive assets in a way that matches your risk tolerance and time horizon

- Tax efficiency: Structuring ownership, using concessional superannuation contributions, and timing asset disposals to minimise tax drag

- Cost management: Keeping management fees, brokerage, and platform costs as low as possible

- Regular review: Adjusting your approach as your circumstances, market conditions, and legislation evolve

- Goal alignment: Connecting each investment decision back to your specific financial objectives, whether that's retiring at 60, funding a child's education, or preserving capital

"Optimisation isn't about chasing the highest return. It's about keeping the most of what you earn, and making sure every dollar is positioned to serve your long-term goals."

Many investors focus exclusively on asset selection while neglecting the structural elements that determine how much of their return actually compounds over time. That's where genuine intelligent wealth strategies separate thoughtful investors from reactive ones.

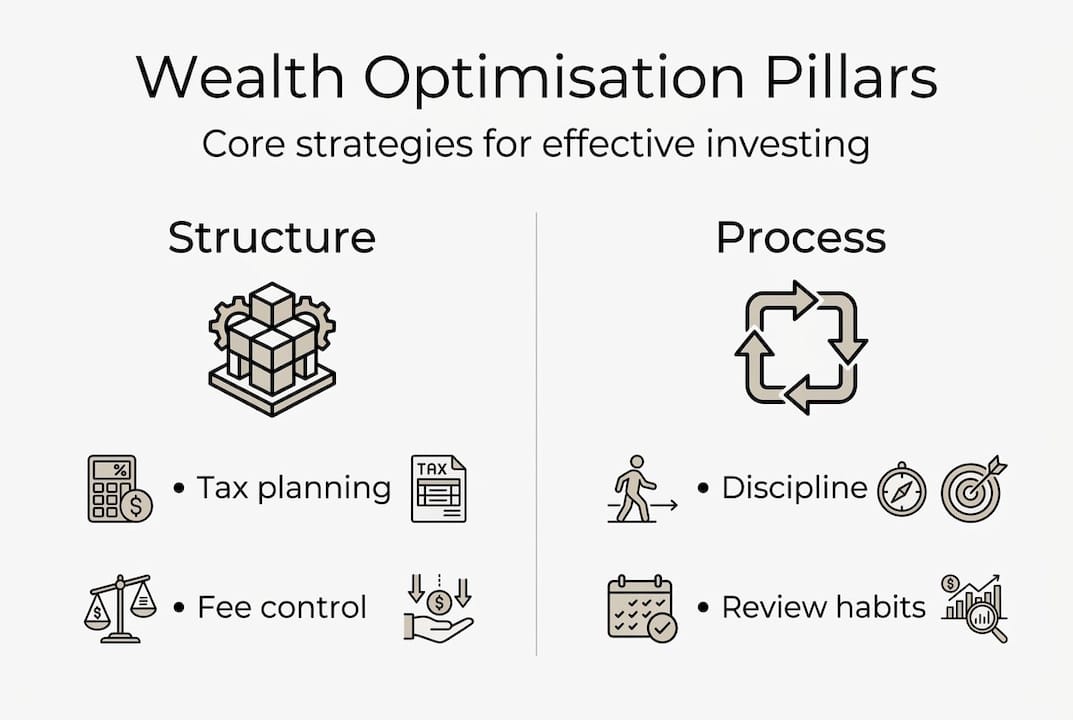

The key pillars of wealth optimisation

An effective wealth optimisation strategy isn't built on one clever idea. It rests on several interconnected pillars that, when working together, produce meaningfully better outcomes over time. Tax strategy and investing efficiency are core pillars of any well-structured approach.

Here's how the main pillars interact:

| Pillar | What it involves | Why it matters |

|---|---|---|

| Asset allocation | Diversifying across asset classes and geographies | Reduces risk without sacrificing long-term growth |

| Tax efficiency | Using super, trusts, and smart disposal timing | Can add 1-2% per year in net returns |

| Cost control | Minimising fees and platform expenses | Compounds powerfully over 10-20 years |

| Regular rebalancing | Adjusting weights as markets move | Keeps your risk profile aligned with your goals |

| Goal alignment | Connecting decisions to timelines and outcomes | Avoids mismatched strategies that undermine progress |

Here's a practical order for building your strategy:

- Define your goals clearly. Know what you're working towards and by when, whether that's a target retirement income or a specific asset milestone.

- Establish the right structure. Consider whether your assets are held personally, in a company, trust, or superannuation fund, since structure drives your tax outcome significantly.

- Allocate deliberately. Match your asset mix to your timeline and risk comfort. A 55-year-old with a 10-year runway needs a different allocation to a 40-year-old with 25 years ahead.

- Automate cost control. Choose low-cost index funds or ETFs where active management doesn't add sufficient value, and review platform fees annually.

- Schedule regular reviews. Set a fixed date each year to assess performance, tax position, and alignment with current goals.

Pro Tip: Australian tax-aware investing should be considered at every stage of portfolio construction, not just at tax time. Decisions made mid-year about contributions, disposals, and franking credits all affect your end-of-year position.

For investors with property, optimising property for retirement means examining not only capital growth projections but also rental yield, depreciation schedules, land tax exposure, and whether the asset fits your overall income and liquidity needs as you approach retirement.

How wealth optimisation strategies work in practice

With a clear framework in mind, let's see how these strategies actually play out for real investors.

Consider a 52-year-old investor with $400,000 in superannuation, a $600,000 investment property, and $150,000 in a direct share portfolio. Without a structured approach, they might be:

- Holding high-growth shares inside super when they're in the accumulation phase but nearing preservation age

- Missing concessional contribution opportunities that would reduce their taxable income

- Holding the investment property in their own name, attracting full marginal tax on rental income

- Trading shares too frequently, triggering short-term capital gains at their full marginal rate

With an optimised approach, the picture looks very different. Contributions are maximised to super to capture the 15% tax rate on earnings. Wealth intelligence tools help model how shifting the property into a different structure affects after-tax cash flow. The share portfolio is managed with a 12-month holding discipline to access the 50% CGT discount available to individual investors.

Technological tools and structured advice help streamline wealth optimisation across asset classes, allowing investors to model scenarios without waiting for a financial adviser appointment.

Here's how the outcomes can compare:

| Scenario | Annual net return | Over 15 years (estimated) |

|---|---|---|

| Unoptimised portfolio | 5.8% after tax and fees | Base outcome |

| Optimised portfolio | 7.2% after tax and fees | Approximately 28% more accumulated |

Common pitfalls an optimised approach avoids:

- Holding cash or low-return assets unnecessarily due to inertia

- Neglecting to use the bring-forward rule for non-concessional super contributions

- Allowing asset allocation to drift significantly without rebalancing

- Missing franking credit benefits by trading around dividend dates

Pro Tip: Personal wealth platforms now allow you to see your entire portfolio in one place, including super, property, and shares, so you can make connected decisions rather than managing each asset in isolation.

Common mistakes and how to avoid them

As you apply these strategies, it's just as important to be aware of the biggest missteps that threaten your long-term success.

Costly mistakes like ignoring tax or overtrading can erode wealth gains even when the underlying investment performance is solid. Here are the most frequent errors self-directed investors make:

- Ignoring the tax impact of investment decisions. Every buy, sell, or income event has a tax consequence. Failing to factor this in means you're optimising for gross returns rather than net ones.

- Overtrading. Frequent buying and selling not only triggers capital gains tax events but also accumulates brokerage costs that silently reduce your returns.

- Attempting to time the market. Most investors who try to move in and out of assets based on short-term signals underperform those who remain disciplined and invested.

- Neglecting to review as circumstances change. Tax legislation, super contribution caps, and personal income all shift over time. A strategy built in 2022 may need significant adjustment by 2026.

- Overlooking fees. A difference of 0.5% in annual fees compounds dramatically. On a $500,000 portfolio over 20 years, that gap can represent more than $100,000 in lost value.

"The investors who struggle most aren't those who made poor stock picks. They're the ones who never paused to check whether their overall structure was working for or against them."

Practical steps to stay on track:

- Schedule a portfolio review every six months, not just at tax time

- Track your capital gains tax strategies throughout the year and model the impact before you sell

- Set a target fee budget for your portfolio and review costs annually

- Use scenario modelling to test how changes in income, contributions, or asset prices affect your outcomes

Understanding investment return explanations in the context of both before-tax and after-tax figures is essential. Many investors are surprised by how much the net figure differs from the headline return.

Our perspective: Why true wealth optimisation is about mindset, not products

There's a version of wealth optimisation that gets sold constantly: the right product, the right platform, the right fund, and your problems are solved. We don't buy that. The tools matter, but they're secondary.

What actually separates investors who build lasting wealth from those who stall is a consistent mindset. Optimisation is not a one-off project you complete and then ignore. It's an ongoing practice of asking whether your current structure, habits, and decisions are still aligned with where you want to go.

The investors we see succeed over a decade are not the ones who found the cleverest tax structure or picked the best-performing asset class. They're the ones who focus on personal wealth consistently, who review their position regularly, who stay curious about what's changed, and who exercise discipline when markets make it tempting to abandon a solid plan.

Focus on what you can actually control: costs, tax positioning, contribution discipline, and regular review. Don't chase trends or restructure every time a new product appears. Celebrate consistent habits more than big wins.

Pro Tip: The most powerful financial decision you can make isn't a single trade or strategy. It's committing to reviewing and refining your approach every year without fail.

Optimise your wealth with smart tools

Understanding the principles is only the first step. Putting them into action requires visibility across all your assets and the ability to model different scenarios with real numbers.

The AlphaIQ platform is built for exactly this: giving Australian self-directed investors a single place to model their superannuation, property, shares, and retirement position with tax-aware intelligence. Use the superannuation calculator to project your super balance under different contribution strategies, or explore the debt recycling calculator to understand how converting non-deductible debt can improve your investment position. These tools make the next step practical, not theoretical.

Frequently asked questions

How is wealth optimisation different from wealth creation?

Wealth creation is about building assets through saving and investing, while optimisation focuses on structure, not just accumulation, ensuring your existing assets deliver the best possible after-tax returns.

What tools do Australian investors use for wealth optimisation?

Platforms, AI tools, and calculators are commonly used, and technological tools streamline wealth optimisation by allowing investors to model scenarios across super, property, and shares in one place.

What's a quick win for beginners starting wealth optimisation?

Start with the basics: minimising fees and tax efficiency are quick wins that immediately improve your net returns without requiring complex restructuring.

Is wealth optimisation only for high net worth individuals?

Not at all. Wealth optimisation is accessible to all investors, and the principles of tax efficiency, cost control, and disciplined allocation apply equally whether you hold $150,000 or $1.5 million.