TL;DR:

- Personal wealth platforms enable self-directed investors to manage diversified markets without ongoing advice costs.

- These platforms offer lower fees, direct ownership, and better transparency for Australian investors and SMSF trustees.

- Success depends on investor engagement and disciplined decision-making, not just platform features or low fees.

For years, many Australians assumed that optimising wealth across investments, superannuation, and retirement required an ongoing relationship with a financial adviser. That assumption is rapidly becoming outdated. Personal wealth platforms now give self-directed investors direct access to diversified markets, SMSF tools, and performance analytics, all without the cost of continuous professional advice. Whether you are in your late 30s building a portfolio or approaching 60 and fine-tuning your retirement income, these platforms have fundamentally shifted what is possible for the engaged, self-managed investor.

Table of Contents

- What are personal wealth platforms?

- Core benefits for self-directed Australian investors

- Comparing major platform types: Brokerage, robo-advisors, and hybrids

- Cautions, limitations, and compliance for self-managed users

- Our perspective: What most guides miss about personal wealth platforms

- Optimise your wealth with innovative platforms

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Direct access | Personal wealth platforms give self-directed investors hands-on access to diversified markets and super control without ongoing advice. |

| Cost efficiency | Platforms offer evidence-backed lower fees compared to traditional financial advice or managed funds. |

| Know your platform type | Brokerage, robo, and hybrid platforms each suit different investing styles and goals—understand what fits your needs. |

| Compliance is crucial | SMSF and DIY investors must stay on top of compliance, ownership, and reporting rules to avoid costly missteps. |

| Success requires discipline | The best outcomes come to investors who pair platform usage with ongoing learning and discipline. |

What are personal wealth platforms?

Personal wealth platforms are digital tools that allow you to manage, track, and grow your financial assets in one place. They sit at the intersection of technology and financial services, giving you direct control over decisions that were once the exclusive domain of advisers and fund managers.

These platforms typically fall into three main categories:

- Online brokers: Platforms like CommSec, SelfWealth, and Stake let you buy and sell shares directly on exchanges such as the ASX, US markets, and Hong Kong. You control every trade and pay per transaction.

- Robo-advisors: Services like Stockspot, Raiz, and Spaceship use algorithms to build and rebalance diversified portfolios automatically. You set your risk profile and the platform does the rest.

- Bank-integrated platforms: Offered by major banks, these combine everyday banking with investment access, making them convenient but sometimes more expensive.

For SMSF (self-managed super fund) trustees, many brokers now offer dedicated SMSF accounts that allow direct share ownership, transparent reporting, and integration with accounting software. This is a significant advantage for those wanting genuine control over their superannuation strategy.

The core capabilities that make these platforms valuable include:

- Access to multiple markets including the ASX, US, and Hong Kong exchanges

- Real-time portfolio tracking and performance analytics

- Tax reporting tools and capital gains summaries

- SMSF account support with audit-ready reporting

- Automated rebalancing (for robo-advisors)

As robo-advisor research for 2026 confirms, platforms enable diversification across ASX, US, and HK markets, SMSF support for super control, and tools for performance tracking, all without the need for ongoing advice. This makes them a natural fit for self-directed investors who want professional-grade capability without the associated cost.

For a broader overview of wealth platforms and how they integrate into a complete financial picture, it is worth understanding how each type serves different investor profiles. You can also explore the wealth intelligence blog for deeper comparisons, including AussieQuant alternatives for modelling and analytics tools.

Core benefits for self-directed Australian investors

With the fundamentals defined, let us zero in on the main benefits Australian self-directed investors are experiencing from using personal wealth platforms.

The most immediate benefit is cost reduction. Traditional financial advice can cost $3,000 to $5,000 per year or more for ongoing service. Most brokerage platforms charge between $0 and $9.50 per trade, and robo-advisors typically charge between 0.1% and 0.66% per annum on your balance. For a $300,000 portfolio, that is a potential saving of several thousand dollars annually.

Key insight: Cost savings compound over time just like returns do. Reducing fees by $3,000 per year over 15 years, assuming that money is reinvested, can add tens of thousands of dollars to your final balance.

For SMSF trustees specifically, the advantages are substantial. Direct share ownership via CHESS-sponsored accounts means you hold legal title to your investments, not a custodian. This matters for transparency, estate planning, and compliance. SMSF platform benefits are particularly relevant for those with balances above $200,000, where the cost-to-benefit ratio of an SMSF becomes more favourable.

Platforms like SelfWealth, which manages over $16 billion in FUA across more than 130,000 users, demonstrate the scale of this shift. SMSF sector performance studies show that well-managed SMSFs can match or outperform industry funds, particularly when investors are engaged and costs are controlled.

Key benefits at a glance:

- Lower fees compared to traditional managed funds and ongoing advice arrangements

- Direct market access to ASX, US, and international shares

- Transparency over every holding, transaction, and tax event

- SMSF compatibility with audit-ready reporting and direct ownership

- Flexibility to adjust your strategy as your circumstances change

Pro Tip: Use a retirement calculator alongside your platform to model how fee reductions and diversification choices affect your projected retirement balance. Small changes in fees and allocation can have a surprisingly large impact over a 10 to 20 year horizon.

Diversification is another core advantage. Platforms now let you access ASX dividend metrics alongside international ETFs (exchange-traded funds), giving you genuine exposure across asset classes, geographies, and sectors without needing a managed fund.

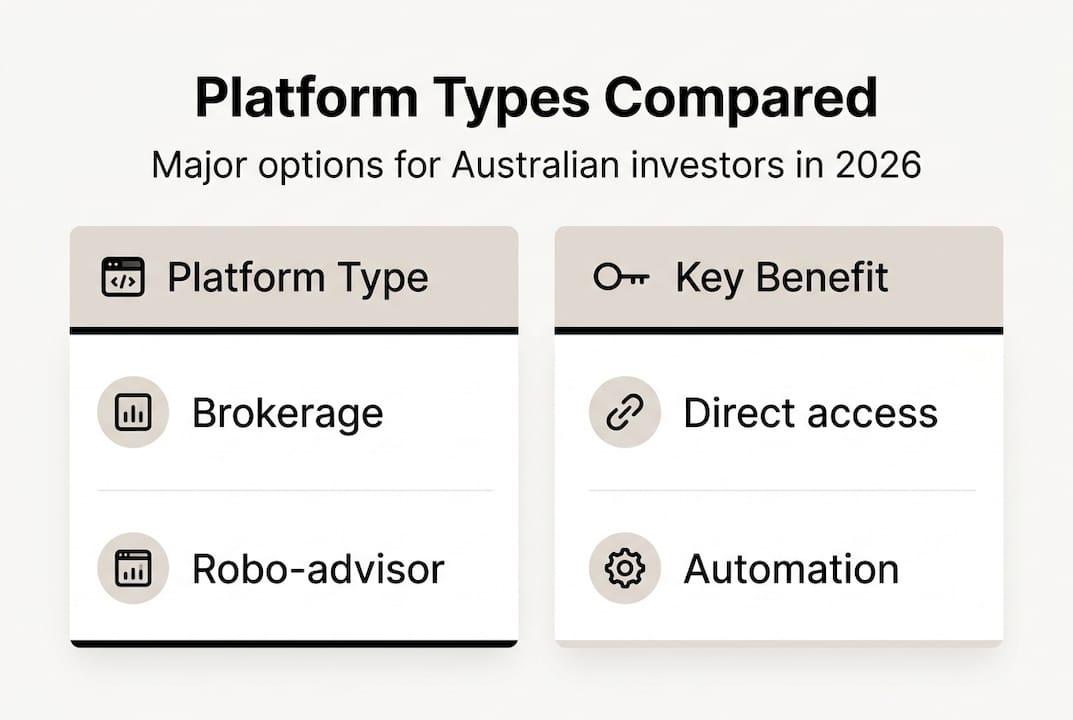

Comparing major platform types: Brokerage, robo-advisors, and hybrids

To maximise results, it is vital to understand the practical differences between Australia's main wealth platform styles.

| Feature | Online broker | Robo-advisor | Bank-integrated |

|---|---|---|---|

| Ownership model | CHESS-sponsored (direct) | Custodial | Custodial |

| Fee structure | $0 to $9.50 per trade | 0.1% to 0.66% p.a. | Varies, often higher |

| Automation level | Manual | Fully automated | Partial |

| Market access | ASX, US, HK | ETFs only (mostly) | ASX focused |

| SMSF support | Yes (most brokers) | Limited | Limited |

| Best for | Active, engaged investors | Set-and-forget investors | Convenience seekers |

As platform fee research shows, brokerage platforms suit active investors who want low per-trade costs and direct ownership via CHESS, while robo-advisors suit those who prefer automated diversification without constant monitoring.

Here is how to think about which type suits you:

- You prefer full control: Choose an online broker. You select every investment, pay per trade, and hold shares directly in your name via CHESS.

- You want automation: Choose a robo-advisor. Your portfolio is built and rebalanced automatically based on your risk profile.

- You want convenience: A bank-integrated platform may suit you, though fees are often higher and asset access is more limited.

- You run an SMSF: An online broker with dedicated SMSF accounts is generally the strongest fit, given CHESS ownership and reporting capabilities.

Pro Tip: Many experienced investors blend both approaches. They use a broker for direct ASX shares and a robo-advisor for international ETF exposure. This hybrid approach gives you control where it matters and automation where it saves time. Understanding the true cost of DIY investing helps you weigh this trade-off clearly.

If you are working towards financial independence, knowing how to calculate your FI number alongside your platform choice gives you a concrete target to build towards.

Cautions, limitations, and compliance for self-managed users

No approach is risk-free, so let us explore the key drawbacks, caveats, and compliance considerations you should understand before fully relying on these platforms.

The first caution is around ownership structure. International shares on most platforms are held via a custodian, meaning you are the beneficial owner but not the direct legal owner. This is standard practice and generally safe, but it matters in the event of platform insolvency or estate administration.

Important: For SMSF trustees, custodial ownership of international assets is permissible, but you must ensure the arrangement complies with the sole purpose test and is documented correctly in your investment strategy.

SMSF-specific limitations include:

- No margin lending within an SMSF (borrowing to invest is only permitted under limited recourse borrowing arrangements)

- No CFDs or certain derivatives within an SMSF structure

- Strict reporting obligations including annual audits, tax returns, and ATO reporting

- Trustee responsibilities that cannot be delegated to the platform itself

As platform compliance guidance highlights, custodial arrangements for international markets, restrictions on margin and CFDs in SMSFs, and compliance reporting are all areas where investor responsibility remains firmly with the trustee, not the platform.

For robo-advisors, the main limitation is reduced control. The algorithm rebalances according to its model, not your personal tax situation. If you have significant capital gains to manage, automated rebalancing could trigger tax events at the wrong time.

Common pitfalls to avoid:

- Assuming the platform handles your compliance obligations (it does not)

- Choosing custodial ownership without understanding what it means for your SMSF

- Underestimating the time required to stay informed and make good decisions

- Ignoring platform disclaimers around financial advice limitations

If you are planning how much super to retire at 60, understanding these limitations helps you build a realistic strategy. Always review the platform limitations disclaimer before committing to any tool.

Our perspective: What most guides miss about personal wealth platforms

Armed with an honest view of the pros and cons, let us step back for some perspective on what really matters when using wealth platforms.

Most guides focus on fees and features. That is useful, but it misses the bigger picture. The investors who genuinely succeed with self-directed platforms are not simply the ones who found the cheapest broker. They are the ones who treat the platform as a tool for ongoing learning and accountability, not a shortcut to passive wealth.

The uncomfortable truth is that a low-cost platform in the hands of a disengaged investor often produces worse outcomes than a slightly more expensive managed fund. Platforms remove the guardrails. That is their strength and their risk.

Understanding the real cost of financial advice versus DIY investing is not just a fee comparison. It is a question of whether you are genuinely prepared to stay engaged, keep learning, and make disciplined decisions across market cycles. Those who do that consistently are the ones who build real wealth through these platforms.

Optimise your wealth with innovative platforms

Ready to put these insights into practice? Here is how innovative tools can take your approach further.

AlphaIQ is built specifically for self-directed Australian investors who want to model and optimise their financial position across investments, superannuation, property, and retirement in one place. It combines tax-aware financial modelling with scenario simulation, so you can see the real numbers behind every decision.

Whether you want to run projections through the AI wealth intelligence platform, estimate your retirement balance with the super calculator, or model a debt recycling strategy with the debt recycling calculator, AlphaIQ gives you the clarity to act with confidence. No ongoing advice fees. Just real numbers, built for your situation.

Frequently asked questions

Are personal wealth platforms safe for self-managed super funds (SMSFs)?

Yes, leading platforms offer dedicated SMSF account support, but trustees remain responsible for all compliance, reporting, and audit obligations. The platform is a tool, not a compliance solution, so SMSF reporting responsibilities always rest with the trustee.

What's the key difference between CHESS-sponsored and custodial platforms?

CHESS-sponsored brokers register shares directly in your name, giving you legal ownership. Custodial platforms hold assets on your behalf, which is standard for international share access but means you are the beneficial rather than legal owner.

How do fees compare between broker and robo-advisor platforms?

Online brokers typically charge between $0 and $9.50 per trade, while robo-advisors charge between 0.1% and 0.66% per annum on your portfolio balance, making the right choice dependent on your trading frequency and balance size.

Is ongoing paid financial advice required to use personal wealth platforms?

No. Most platforms are designed for self-directed use without ongoing advice, but consistent self-education and disciplined decision-making are essential to achieving good long-term outcomes.

Recommended

- AlphaIQ — AI Wealth Intelligence Platform for Australian Investors

- AlphaIQ Blog — Wealth Intelligence for Australian Investors

- Top 5 AussieQuant Alternatives 2026

- Financial Independence in Australia: Calculating Your FI Number | AlphaIQ

- Best wealth management tools for global professionals 2026 | Settel Blog | Settel