TL;DR:

- Tax-aware investing consistently preserves more wealth than focusing solely on stock selection or market timing.

- Strategies like tax-loss harvesting, holding assets for CGT discounts, and asset location optimize after-tax returns.

- Choosing appropriate investment structures and understanding ATO rules are crucial for long-term tax-efficient wealth building.

Most self-directed investors spend enormous energy researching stocks, comparing ETFs, and watching market movements. Yet one factor quietly erodes more of their wealth than poor stock picks or high fees ever could: tax. Research confirms that taxes erode returns more than market timing or fund costs in many cases. The investors who consistently build the most wealth are not necessarily the best stock pickers. They are the ones who understand how to keep more of what they earn. This guide explains how tax-aware investing works, which strategies matter most for Australians, and how a few structural decisions can dramatically improve your after-tax outcomes over time.

Table of Contents

- What is tax-aware investing and why does it matter?

- Essential tax-aware strategies for Australian investors

- Common pitfalls and advanced tax-nuance scenarios

- Structuring your investments for optimum after-tax outcomes

- The uncomfortable truth about tax-aware investing most miss

- Boost your wealth with smarter tax-aware tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Tax drag matters | Ignoring tax can quietly erode wealth more than poor investment choices. |

| Simple strategies work | Tax-loss harvesting, franking credits, and asset location all meaningfully boost after-tax returns. |

| Avoid common pitfalls | Stick to ATO guidelines on wash sales and choose the right structure to avoid tax traps. |

| Structures impact results | Using trusts, super, or companies appropriately may save you thousands every year. |

What is tax-aware investing and why does it matter?

Tax-aware investing means structuring your portfolio with tax consequences in mind at every step. It is not about avoiding tax illegally. It is about making deliberate choices around what you buy, when you sell, how you hold assets, and in whose name, so that you legally minimise the tax you pay and maximise the returns you actually keep.

The concept of tax drag is central here. Tax drag refers to the reduction in your compound returns caused by paying tax on gains, dividends, or income along the way. Even a 1 to 2 percentage point drag per year sounds modest, but over 20 years it can reduce your final portfolio value by 30% or more. That is a significant cost, and it compounds in reverse, meaning the longer it runs, the more damaging it becomes.

Key insight: After-tax returns matter more than gross returns. Two portfolios with identical pre-tax performance can produce vastly different wealth outcomes depending on how tax is managed.

Here is why tax-aware investing deserves your attention:

- It beats fee optimisation. Reducing your management expense ratio from 0.5% to 0.2% saves 0.3% annually. But reducing your effective tax rate from 47% to 25% on the same gains saves far more.

- It is more reliable than market timing. You cannot consistently predict market movements, but you can consistently apply tax strategies that work every year.

- It supercharges compounding. Every dollar you do not pay in tax stays invested and compounds. Over decades, this effect is substantial.

- It applies to all asset classes. Shares, property, super, and cash all have different tax treatments, and understanding each one lets you allocate smarter.

Exploring capital gains tax strategies is one of the most practical starting points for any self-directed investor. You can also find a broad range of wealth intelligence tips to sharpen your overall approach. For those approaching retirement, understanding tax-free retirement income can be especially powerful.

Essential tax-aware strategies for Australian investors

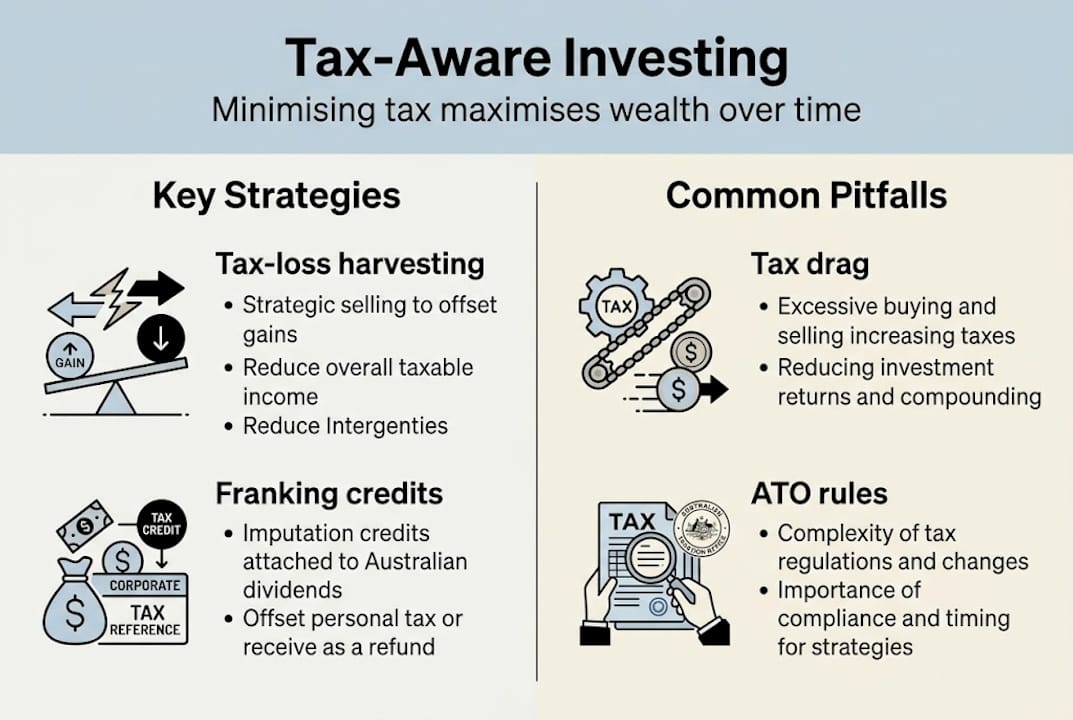

After understanding the stakes of tax drag, it is time to explore the practical strategies that significantly improve your after-tax results. Key methods include tax-loss harvesting, using low-turnover funds, preferring assets with franking credits, and smart asset location.

-

Tax-loss harvesting. This involves selling an investment that has fallen in value to realise a capital loss, which you then use to offset capital gains elsewhere in your portfolio. Losses not used in the current year carry forward indefinitely, giving you future flexibility. The key is to act deliberately and avoid the ATO's wash sale rules (covered in the next section).

-

Hold for the CGT discount. Holding an asset for more than 12 months before selling entitles individuals and trusts to a 50% capital gains tax discount. This alone can halve your CGT liability on a profitable investment. Low-turnover ETFs are ideal here because they rarely trigger internal capital gains events. Understanding CGT discount strategies is essential before you sell anything.

-

Prioritise franking credits. Australian shares and ETFs that pay fully franked dividends come with attached tax credits representing company tax already paid. These credits reduce your personal tax bill, and in some cases generate a refund. You can calculate after-tax dividends to see exactly how much franking credits improve your real yield. Use the franking credit calculator to model your specific situation.

-

Asset location. Place growth-oriented assets inside superannuation where the tax rate on earnings is just 15%, and capital gains are taxed at 10% after 12 months. Keep income-generating assets in structures suited to income splitting, such as trusts or companies, where appropriate.

Pro Tip: Do not just look at a fund's headline yield. Always calculate the after-tax yield including franking credits, especially if you are in a lower tax bracket where those credits may generate a cash refund.

| Strategy | Tax benefit | Best suited to |

|---|---|---|

| Tax-loss harvesting | Offsets capital gains | Investors with mixed gains and losses |

| Hold 12+ months | 50% CGT discount | Long-term equity investors |

| Franked dividends | Reduces or eliminates tax on income | Australian share investors |

| Super asset location | 15% earnings tax rate | Growth-focused pre-retirees |

Common pitfalls and advanced tax-nuance scenarios

Once you know the right strategies, watch out for common mistakes and subtle ATO rules that can trip investors up.

ATO wash sale rules are one of the most misunderstood areas. The ATO does not set a fixed number of days you must wait before repurchasing an asset. Instead, the rule is substance-based: if the ATO determines that a sale and repurchase was designed to manufacture a tax loss without any genuine change in economic exposure, it will deny the deduction. This means you need a real reason for selling, not just a tax motive.

Here are the most common pitfalls to avoid:

- Repurchasing too quickly. Selling an ETF and buying an almost identical one the next day may still trigger wash sale scrutiny if the ATO views it as artificial.

- High-turnover funds. Actively managed funds that trade frequently crystallise capital gains inside the fund, which flow through to you as a taxable distribution, even if you did not sell your units.

- Confusing capital losses with income offsets. Capital losses can only offset capital gains. They cannot reduce your salary, rental income, or dividends. Many investors make this mistake and are surprised at tax time.

- Ignoring ownership structure. Holding investments in your own name when a trust or company structure would be more tax-efficient is a missed opportunity, particularly for high-income earners.

Important: Couples who own investment property or shares as tenants in common can split income in any proportion they choose, directing more income to the lower-earning partner and reducing the household tax bill.

The bucket company approach is worth noting here. A discretionary trust distributes income to a company (the bucket company), which pays tax at the corporate rate of 25 to 30%, rather than the individual's marginal rate of up to 47%. This strategy is particularly effective for high-income households. Watch out for capital gains traps and understand the rules around holding for CGT discount before acting.

Pro Tip: Always document your reason for selling an investment at a loss. A clear record showing that the decision was based on a genuine reassessment of the asset, not purely tax motivation, provides important protection if the ATO ever questions the transaction.

Structuring your investments for optimum after-tax outcomes

To finish, let us bring structure into focus and see what strategy mix best boosts your after-tax wealth. Structures like trusts and bucket companies allow income splitting, while asset location across super versus personal ownership changes the tax rate landscape significantly.

The structure you use to hold investments is one of the most powerful levers available to you. Here is a comparison of the four main options:

| Structure | Tax rate on income | CGT treatment | Key advantage |

|---|---|---|---|

| Personal name | Marginal rate (up to 47%) | 50% discount after 12 months | Simplest, most flexible |

| Superannuation | 15% (0% in pension phase) | 10% after 12 months | Best for long-term growth |

| Discretionary trust | Distributed at beneficiary rates | 50% discount flows through | Flexible income splitting |

| Company/bucket co. | 25 to 30% | No CGT discount | Caps tax rate for retained income |

Here is a practical order of action for structuring your investments:

- Review your current structure. Identify what you hold personally versus in super, and whether a trust or company structure is appropriate for your household income level.

- Match assets to structures. Place high-growth, low-yield assets in super to benefit from the 15% earnings tax rate. Place income-producing assets in a trust if you have lower-income beneficiaries to distribute to.

- Assess household income distribution. If your partner earns significantly less, consider how ownership splits or trust distributions can reduce your combined tax bill.

- Model the outcomes. Use tools to project your retirement wealth under different structural assumptions before making changes.

These decisions are not one-off. As your income, family situation, and portfolio grow, revisiting your structure every few years ensures it continues to serve your goals.

The uncomfortable truth about tax-aware investing most miss

Here is something the financial industry rarely says loudly: tax planning consistently outperforms stock picking as a wealth-building tool. Most investors obsess over finding the next great investment, but the returns from smart tax management are more reliable, more predictable, and often larger in dollar terms.

Consider this. A 1.5% annual tax saving on a $500,000 portfolio is $7,500 per year. Compounded over 20 years, that difference in retained capital adds hundreds of thousands of dollars to your final wealth. No stock tip delivers that kind of certainty.

The financial industry underplays tax-aware strategies because they require personalisation. They cannot be packaged into a product and sold at scale. That means the responsibility falls on you as a self-directed investor to seek this knowledge out.

The good news is that you do not need to overhaul your entire financial life. A few structural tweaks, such as holding the right assets in super, using franked dividend investments, and applying the CGT discount consistently, can deliver compounding benefits year after year. The investors who get this right do not just beat the market. They beat their past selves, quietly and reliably, every single year.

Boost your wealth with smarter tax-aware tools

If you are ready to make your investments truly tax-aware, AlphaIQ can help simplify and optimise your strategy with tools built specifically for self-directed Australian investors.

The AI Wealth Intelligence Platform brings together tax-aware modelling, scenario simulation, and personalised projections across super, property, and investments in one place. You can project your retirement under different structural and tax assumptions, or run the numbers on strategies like debt recycling using the Debt Recycling Calculator. AlphaIQ gives you the clarity to act with confidence, backed by real numbers, without the ongoing cost of financial advice.

Frequently asked questions

Why is tax-aware investing more important than just chasing returns?

Minimising tax often boosts your net wealth more reliably than seeking high returns or timing the market, because tax erodes investment gains consistently and predictably, year after year, regardless of market conditions.

What is tax-loss harvesting and does the ATO allow it in Australia?

Tax-loss harvesting means selling investments at a loss to offset capital gains; the ATO allows it but disallows artificial wash sales where no genuine change in economic exposure occurs.

How do franking credits help Australian investors?

Franking credits attached to dividends represent company tax already paid, reducing or eliminating double taxation and boosting after-tax yields for Australian shareholders, particularly those in lower tax brackets who may receive a cash refund.

Is there an easy way to compare taxes across investment structures?

Yes, use comparison tables and modelling calculators to evaluate how personal, super, trust, and company structures each affect your effective investment tax rate and long-term wealth outcomes.