TL;DR:

- Australian middle managers often have concentrated wealth in property and super, risking financial insecurity.

- Regularly reviewing and diversifying wealth strategies enhances resilience and long-term growth.

- Using tools like AlphaIQ supports precise planning and helps avoid common pitfalls.

Middle management professionals in Australia often find themselves in a frustrating position: solid incomes, genuine ambition, but not enough time or know-how to make their money work as hard as they do. You might be earning $120,000 or more, yet feel no closer to financial security than you did five years ago. That gap between earning well and planning well is where most professionals quietly lose ground. This guide walks you through the essentials of wealth planning tailored specifically for your career stage, covering what you need to know, what to do, common mistakes to sidestep, and how to verify your plan is actually working.

Table of Contents

- Understanding your wealth planning needs as a middle manager

- Laying the groundwork: Key wealth building blocks

- Active wealth management strategies for professionals

- Reviewing progress and updating your plan

- Avoiding the most common mistakes

- Critical perspective: What most managers miss in wealth planning

- How AlphaIQ can support your wealth journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Identify financial foundation | Know your assets, income, and risk to set a solid wealth plan starting point. |

| Diversify and protect | Spread investments across assets and ensure proper insurance for true security. |

| Actively manage progress | Review and adjust your strategies yearly or with major life events to stay on track. |

| Avoid costly mistakes | Learn from common errors like overconcentration and lack of review to keep wealth growing. |

| Leverage expert tools | Use calculators and professional advice to optimise your wealth strategy efficiently. |

Understanding your wealth planning needs as a middle manager

Now that we've set the stage for why middle management requires a tailored approach, let's clarify your starting point.

Australian middle managers typically earn between $100,000 and $180,000 per year, depending on industry and tenure. Many carry a mortgage, have growing families, and hold most of their wealth in a combination of owner-occupied property and superannuation. On paper, that sounds solid. In practice, it leaves a lot of financial risk concentrated in just two asset classes.

Here's what the typical financial picture looks like for a middle manager in Australia:

| Financial element | Typical position |

|---|---|

| Gross annual income | $110,000 to $180,000 |

| Owner-occupied property equity | $200,000 to $600,000 |

| Superannuation balance (age 40) | $80,000 to $180,000 |

| Investment assets outside super | Often minimal |

| Personal debt (mortgage) | $400,000 to $700,000 |

The barriers that hold professionals back at this stage tend to be consistent:

- Time pressure: Long work hours make it easy to push financial planning to the bottom of the list

- Over-reliance on employer super: Assuming super alone will be enough by retirement

- Under-diversification: Wealth concentrated in property and a single super fund

- No clear financial baseline: Many professionals haven't calculated their actual net worth or monthly cash surplus

Understanding your net worth and cash flow is the first step in effective wealth planning. Before you can grow your wealth, you need to know exactly where you stand. Collect your most recent super statement, mortgage balance, and investment accounts, then calculate your true net worth and monthly cash flow.

Your risk profile also matters. A 42-year-old with 20 years until retirement can afford to hold more growth assets than someone five years out. Understanding your career timeline shapes every decision that follows. Reviewing the range of wealth platforms in Australia can help you identify the right tools to track these numbers consistently.

Pro Tip: Set aside two hours this month to list every asset, every liability, and your average monthly cash surplus. That single exercise often reveals opportunities and risks that have been invisible for years.

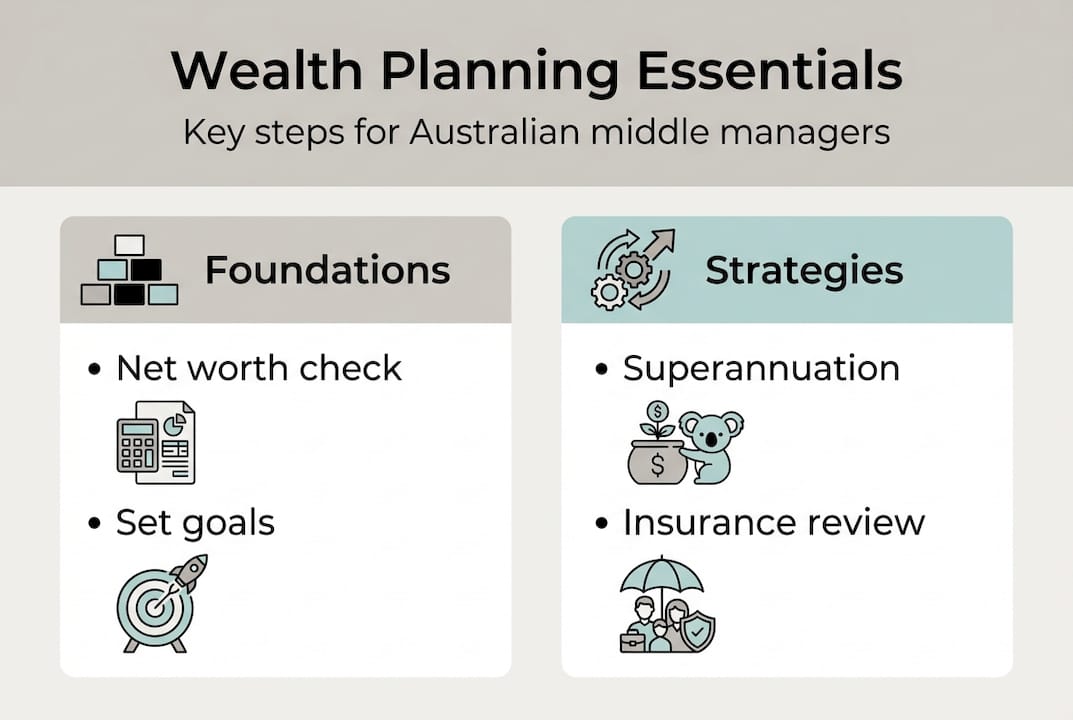

Laying the groundwork: Key wealth building blocks

With a clear view of your financial standing, it's time to focus on the core pillars for building and protecting your wealth.

Superannuation is often the cornerstone of retirement planning for Australians. But it shouldn't be the only pillar. A genuinely resilient wealth plan draws from multiple sources.

Here's how the main asset classes compare for middle managers:

| Asset class | Growth potential | Liquidity | Risk level | Tax efficiency |

|---|---|---|---|---|

| Superannuation | High | Low (until preservation age) | Medium | Very high |

| Australian shares | High | High | Medium to high | High (franking credits) |

| Investment property | Medium to high | Low | Medium | Moderate |

| Managed funds | Medium to high | Medium | Varies | Moderate |

| Cash/term deposits | Low | High | Very low | Low |

Building a diversified financial base is a step-by-step process:

- Maximise concessional super contributions up to the $30,000 annual cap (2026 limit) to reduce taxable income and grow your retirement savings efficiently.

- Establish an investment portfolio outside super using shares or managed funds so you have accessible wealth before preservation age (typically 60).

- Review your property position and assess whether your equity is working for you or simply sitting idle.

- Secure appropriate insurance including income protection, life cover, and total permanent disability cover to protect the financial plan you're building.

Using retirement calculators lets you model different contribution levels and investment returns to project your retirement readiness over time. It's far more powerful than guessing. If you're weighing up different super structures, comparing self-managed super vs industry funds can clarify which approach suits your balance and involvement level.

Pro Tip: Income protection insurance is often undervalued by professionals. If you earn $150,000 and are unable to work for 12 months, the financial impact can wipe out years of accumulated savings. Check your cover today.

Active wealth management strategies for professionals

Once your plan's bedrock is set, you can start using advanced strategies to accelerate your financial growth.

Diversification is more than just owning different things. It means spreading risk across asset classes that don't all move in the same direction at the same time. For middle managers with strong incomes, there are several practical ways to do this:

- Salary packaging: Where available, use pre-tax salary for benefits like novated leases or additional super contributions to reduce your taxable income

- Debt recycling: Convert non-deductible mortgage debt into tax-deductible investment debt, accelerating both debt reduction and portfolio growth

- Tax-effective investment structures: Consider holding investments in a family trust or company structure if your wealth reaches a level where asset protection and tax planning are priorities

- Franking credits: Prioritise Australian shares that pay fully franked dividends to improve after-tax returns on your investment portfolio

Overconcentration in a single asset or sector is a common risk among professionals. This often happens when company shares from an employer equity scheme form a large part of your investment portfolio without being rebalanced. A single bad year for that company can undo significant progress.

Balancing salary, bonuses, and investment income also requires discipline. When a bonus arrives, it's tempting to spend it. A better approach is to direct at least 50% toward your investment goals before lifestyle spending is considered.

Key insight: Australians who invest consistently over a 20-year period, even in modest amounts, typically build significantly more wealth than those who wait for the 'right moment' to invest larger sums.

Exploring wealth intelligence strategies can help you identify which structures and approaches are most suitable for your income and asset mix. Reviewing asset optimisation techniques regularly ensures you're not leaving money on the table.

Reviewing progress and updating your plan

Putting your plan into action is only part of the equation. Staying on track and adapting is equally important.

Regular check-ins help ensure you're on track for retirement and major life goals. Life changes fast in middle management. Promotions, redundancies, new children, property purchases and inheritances all shift your financial picture significantly.

Here's a practical review process you can follow:

- Annual review: Reassess your net worth, investment returns, super balance growth, and insurance cover

- Quarterly check-in: Monitor cash flow, debt levels, and contribution rates

- Event-triggered review: After any major life change, sit down and reassess your goals and strategies

The data points worth tracking at each review include:

- Super balance growth versus your retirement target

- Portfolio performance against relevant benchmarks

- Mortgage offset balance and debt reduction progress

- Any changes to tax position or income

- Insurance cover adequacy relative to current income and liabilities

Using a retirement planning checklist keeps each review structured and ensures nothing is overlooked. For those closer to retirement, understanding how to approach planning retirement income transforms your focus from accumulation to sustainable drawdown. If property is part of your wealth mix, revisiting property investment strategies can reveal whether your property is genuinely contributing or simply consuming cash flow.

When your financial situation becomes genuinely complex, such as when you're managing multiple investment properties, a large super balance, and business interests, professional financial advice becomes worthwhile. The cost of good advice at that point is almost always justified by the outcomes.

Avoiding the most common mistakes

Just as crucial as what to do is what not to do on your path to financial security.

Middle managers are capable, analytical, and used to making decisions under pressure. Those strengths sometimes become weaknesses when applied to personal wealth. Here are the mistakes that appear most often:

- Ignoring insurance: Many professionals are adequately covered by default super insurance at age 30 but fail to review cover as income and liabilities grow

- Neglecting tax: Investment decisions made without considering capital gains tax, marginal tax rates, or franking credits can quietly erode returns

- Delaying plan updates: Busy schedules mean annual reviews get pushed back, then forgotten entirely for two or three years

- Overconfidence after a good year: A strong market return or bonus can create a false sense that no action is needed

- Ignoring portfolio concentration risk: Letting employer shares or a single property dominate total net worth without rebalancing

Failing to update your wealth plan after major life events can undermine years of disciplined strategy. A career change, divorce, or property sale all demand an immediate reassessment of your financial direction.

Pro Tip: Create a recurring calendar event every six months labelled 'Wealth plan review.' Treat it like a work meeting. Even a 30-minute review twice a year is far better than none at all, and it keeps your financial goals in active focus rather than passive hope.

Critical perspective: What most managers miss in wealth planning

Beyond the mechanics and checklists, there's a deeper reality most wealth guides overlook.

The biggest threat to middle management wealth isn't bad investment decisions. It's inertia dressed up as caution. Most professionals know they should be doing more. They research options, read articles, and then wait for conditions to feel right before acting. That waiting is almost always more costly than the imperfect action they avoided.

Career and policy changes also move faster than most people anticipate. A restructure at 48, a change to super contribution caps, or a shift in property values can overturn financial assumptions built over a decade. The professionals who navigate these moments best aren't the ones with perfect plans. They're the ones who review and adjust regularly, keeping their strategy flexible rather than fixed.

True wealth planning isn't about maximising every dollar. It's about building enough resilience that when life changes, as it always does, your financial position doesn't collapse with it. Using wealth intelligence tools gives you the visibility to spot those shifts early and respond with confidence.

How AlphaIQ can support your wealth journey

For those who want smarter ways to track and grow their wealth, here's how AlphaIQ can help.

The AlphaIQ platform brings together superannuation modelling, investment scenario analysis, property planning, and retirement projections in one place, designed specifically for self-directed Australian investors like you.

Whether you want to model the impact of extra super contributions, explore debt recycling calculator scenarios for your mortgage, or run projections using the super calculator, AlphaIQ gives you the clarity to act with confidence. You get tax-aware modelling and real numbers, without the cost of ongoing financial advice. If you're ready to move beyond guessing and start planning with precision, AlphaIQ is built for exactly that.

Frequently asked questions

What is the biggest financial challenge for middle management in Australia?

Balancing income growth with rising expenses and ensuring sufficient retirement savings are the most common challenges. Understanding cash flow and tracking expenses is crucial for effective wealth planning at this career stage.

How often should I review my wealth plan?

You should review your plan at least annually, or immediately after major life changes such as promotions, job loss, or shifts in family circumstances. Regular check-ins help ensure you remain on track for your financial goals.

What role does superannuation play in my overall wealth?

Superannuation is often the cornerstone of retirement planning for Australians, and a growing super balance can significantly strengthen your long-term financial security when combined with investments outside the fund.

Is it better to manage investments myself or seek professional advice?

A mix of self-directed strategies and professional guidance works well, particularly as your finances grow in complexity. Getting professional advice is important when you're managing multiple assets, structures, or approaching retirement.

How can I avoid common mistakes in wealth planning?

Regular reviews, genuine diversification, and a clear understanding of insurance and tax implications help you sidestep the most frequent pitfalls. Failing to update your plan after life events is one of the most damaging errors you can make.