TL;DR:

- Successful Australian property investors focus on managing their entire portfolio system rather than just individual properties. They track key metrics like IRR, cash-on-cash return, and LVR across all assets to optimize risk and growth collectively. Regular, disciplined review and system-based strategies are essential for sustainable wealth building rather than relying solely on property acquisition.

Most Australian property investors spend years obsessing over which suburb to buy in, which property type to choose, or which agent to trust. Yet the investors who genuinely build wealth over time are not necessarily the ones who picked the perfect property. They are the ones who learnt to manage, measure, and optimise their portfolio as a whole system. That distinction is where real financial leverage lives, and it is the focus of everything that follows.

Table of Contents

- What does it mean to optimise your property portfolio?

- Key reasons to optimise your portfolio, not just properties

- The most important metrics for portfolio optimisation

- Nuances and pitfalls: what most investors miss about optimisation

- How to get started: practical steps for optimising your portfolio

- The uncomfortable truth about portfolio optimisation in Australia

- Take the next steps with AlphaIQ tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Look at the whole portfolio | True progress comes from managing your entire portfolio, not just individual properties. |

| Track the right metrics | Use internal rate of return, cash-on-cash returns, and other portfolio-level indicators for real insight. |

| Beware common pitfalls | Overfocusing on yield or ignoring credit limits can stall your growth. |

| Discipline beats cleverness | Consistent tracking and action will outperform one-off clever tricks every time. |

What does it mean to optimise your property portfolio?

Portfolio optimisation is frequently misunderstood. Many investors assume it simply means buying more properties or swapping underperformers for better ones. In reality, it means something far more deliberate and measurable.

To optimise your investment portfolio is to enhance your net total returns while simultaneously reducing risk across the entire collection of assets you hold. That is a portfolio-wide goal, not a property-by-property one. The focus shifts from "how is this property performing?" to "how is my portfolio performing as a system?"

This means tracking indicators that reflect the whole picture:

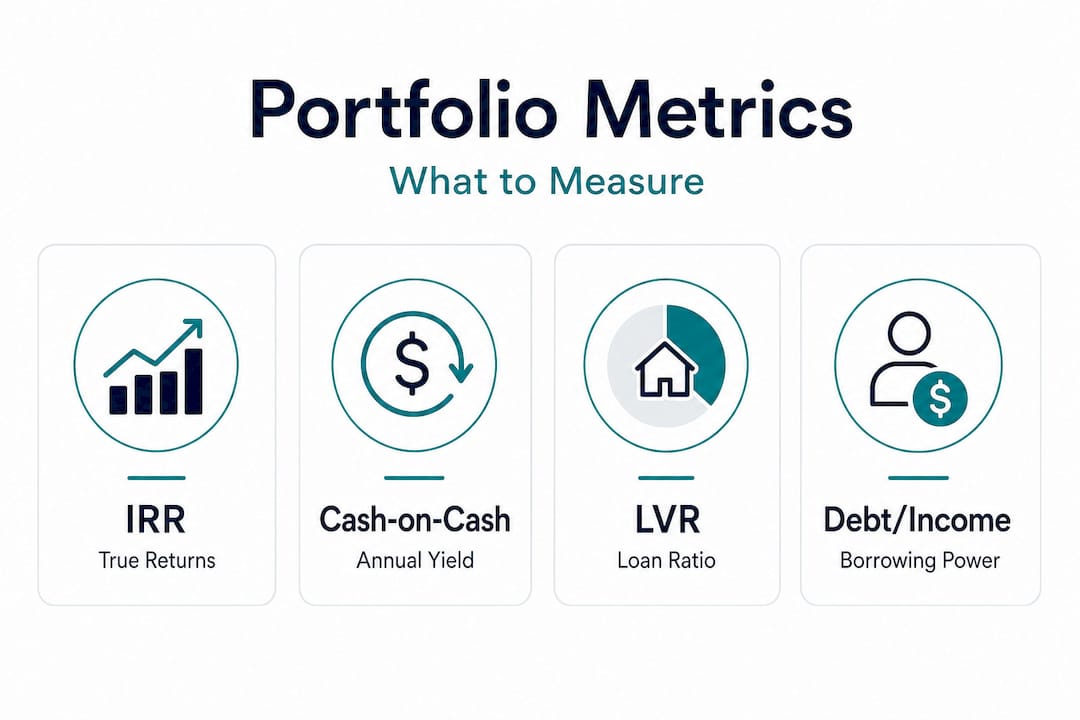

- Internal rate of return (IRR): The true annualised return across all capital invested over time, accounting for timing of cash flows

- Cash-on-cash return: The annual pre-tax cash income divided by the total cash you have invested, giving a realistic income performance figure

- Portfolio loan-to-value ratio (LVR): The percentage of your combined property values that is funded by debt

- Vacancy rates: Across your portfolio, not just for one tenancy at a time

- Debt-to-income ratio: How much of your gross income is consumed by debt repayments

As portfolio benchmarking research confirms, tracking portfolio-wide returns and risk indicators such as cash-on-cash and IRR is a practical and necessary optimisation mechanism. Relying on a single property's yield figure tells you very little about whether your overall position is improving or deteriorating.

"The goal of portfolio optimisation is not to hold only perfect properties. It is to ensure your collection of assets works together to produce the best possible risk-adjusted outcome over time."

Four goals sit at the centre of genuine optimisation: capital growth, income stability, risk reduction, and finance efficiency. When you measure and manage all four together, you move from being a property collector to being a property investor.

Key reasons to optimise your portfolio, not just properties

Many investors fall into a pattern of making decisions in isolation. They buy one property, then another, often guided by different advisers, market conditions, or opportunistic timing. The result is a collection of unconnected assets rather than a coordinated portfolio. This is sometimes called a "property silo" approach, and it has real financial consequences.

Here are the three most important reasons to shift to a portfolio-level focus:

- Risk diversification: When you view properties individually, you miss how concentrated or correlated your risk actually is. Two investment properties in the same suburb, financed through the same lender, with leases expiring in the same month, represent compounding risk. A portfolio lens makes that visible.

- Leverage management: Debt across your portfolio must be managed strategically, not just serviced property by property. The way you structure and sequence your borrowings has a significant impact on your ability to keep growing and to weather rate cycles.

- The weakest link effect: One underperforming property with poor cash flow, a structural maintenance burden, or an unfavourable loan structure can constrain your entire borrowing capacity and drag down your portfolio's overall IRR.

Property investment workflow matters enormously here. As real estate asset management guidance points out, for many investors the biggest gains come not from acquiring or swapping properties, but from measuring and managing debt, vacancy and lease events, and compliance cohorts across the whole portfolio. That is a sobering insight for investors who spend most of their energy on acquisition.

| Dimension | Property-level focus | Portfolio-level focus |

|---|---|---|

| Returns measured | Gross yield per property | IRR and cash-on-cash across all assets |

| Risk management | Vacancy in one property | Synchronised vacancy and cash flow risk |

| Finance efficiency | Loan on each property | Portfolio LVR and serviceability headroom |

| Growth capacity | Next property when ready | Structured sequencing of debt and equity |

| Decision making | Reactive and ad hoc | Disciplined, metrics-driven, and proactive |

Portfolio rebalancing is one practical tool that emerges when you adopt this lens. Rather than waiting until something breaks, you periodically assess whether your allocation across asset types, geographies, and loan structures still serves your goals.

Pro Tip: Most portfolio failures stem not from poor property selection, but from poor inter-property management. Vacancy timing, lease synchronisation, debt structure across properties, and lender relationships all sit below the surface of what most investors track.

The most important metrics for portfolio optimisation

Knowing you should track portfolio-wide metrics is one thing. Knowing which specific numbers to focus on is another. Here is a clear breakdown of what actually matters.

IRR (internal rate of return) is arguably the most honest measure of how your portfolio is performing over time. It accounts for when you invested capital, when you received returns, and the time value of money. A property that grew well but required substantial holding costs may have a far lower IRR than you expect.

Cash-on-cash return tells you what you are actually earning each year relative to the cash you have put in. For a negatively geared portfolio, this figure will often be negative in the short term, which is why understanding it clearly matters for cash flow planning.

Debt-to-income ratio is a metric lenders scrutinise heavily, particularly after regulatory tightening by APRA (the Australian Prudential Regulation Authority). Keeping this ratio within a manageable range preserves your capacity to borrow for future purchases or refinancing.

Portfolio LVR is the blended loan-to-value ratio across all properties. As values rise, your LVR improves and equity builds. Tracking this regularly helps you identify when you have usable equity and when you are approaching risk thresholds.

As portfolio benchmarking research highlights, most investors who rely only on property-level metrics miss compounding risks that only appear at the portfolio level. You can model property investment scenarios to see exactly how these metrics interact across different market conditions.

| Metric | Single-property tracking | Portfolio-wide tracking |

|---|---|---|

| Yield | Gross rent divided by value | Weighted average across all properties |

| Return | Capital gain on one asset | IRR across all invested capital and time |

| Debt | Loan balance per property | Combined LVR and debt-to-income ratio |

| Cash flow | Monthly rent vs mortgage | Synchronised net cash position across portfolio |

| Risk | Vacancy in one tenancy | Correlated vacancy and rate exposure |

Warning signs that your current review process is inadequate:

- You can name the yield of each property but not your portfolio IRR

- You have not reviewed your combined LVR in the past 12 months

- Your loan structures were set up at different times with no overarching strategy

- You are not tracking when leases expire across properties in the same financial period

- You have no written benchmark to compare your actual returns against

A personal finance modelling guide can help you build the habit of running consistent, structured reviews. As property portfolio management research shows, portfolio-level reporting and a disciplined review rhythm help prevent "optimise everything" paralysis and ensure you act on the highest-impact issues first.

Nuances and pitfalls: what most investors miss about optimisation

Even experienced investors can fall into traps that subtly undermine their portfolio performance. Some of these are structural, some are behavioural, and some are the result of following advice that was designed for simpler portfolios.

One of the most significant but overlooked factors is lender credit policy. As finance-first strategies for scalable portfolios make clear, portfolio optimisation must account for how lender credit policy and serviceability buffers interact with your household cash flow. Chasing a yield target means very little if your borrowing capacity is exhausted after three properties.

"For many Australian investors, serviceability rather than yield becomes the real bottleneck after property two or three. Optimising for the wrong constraint leads to strategies that simply cannot scale."

Common pitfalls to be aware of:

- Chasing scale over quality: Adding properties to grow the portfolio without assessing whether new debt is sustainable given your current household obligations

- Ignoring cash flow timing: A portfolio where leases, maintenance cycles, and rate resets all cluster in the same quarter creates significant short-term pressure

- Overweighting yield as a signal: High-yield properties in lower-growth markets can look attractive on paper but underperform when total return including capital growth is measured properly

- Neglecting household obligations: Your portfolio does not operate in isolation from your personal finances. School fees, income changes, or major household expenses affect your capacity to service investment debt

- Missing serviceability cliff edges: Each time you apply for new finance, lenders assess your full debt position. An undisclosed credit card or car loan can tip serviceability calculations unexpectedly

Pro Tip: For most Australians, serviceability will become your binding constraint by the time you hold two to three properties. Structure your debt carefully from the start, because the way you set up early loans directly affects how much more you can borrow later. Understanding how RBA rate changes affect investment returns is part of building that awareness.

If you are thinking about optimising property investment for secure retirement outcomes, then keeping a clear view of both portfolio metrics and lender constraints is not optional. It is the foundation of every sustainable strategy. Consider reviewing smart property investment tips tailored to Australian wealth-building contexts as a starting point.

How to get started: practical steps for optimising your portfolio

You do not need to overhaul everything at once. The most effective approach is systematic, incremental, and focused on the highest-impact actions first. Here is a clear five-step process to begin.

- Gather your data: Collect current loan balances, interest rates, property values, rental income, vacancy history, and lease expiry dates for every property. If this information is scattered across folders and statements, consolidating it is your first priority. You cannot optimise what you cannot see.

- Set a review calendar: Commit to a structured review at least every six months. This does not need to be elaborate. A consistent review rhythm, as supported by property portfolio management guidance, is more valuable than an occasional deep dive followed by months of inaction.

- Choose your metrics and benchmarks: Decide which metrics you will track at the portfolio level. At minimum, include portfolio LVR, cash-on-cash return, and IRR. Set a target range for each that reflects your stage of wealth building and risk tolerance.

- Track and compare over time: A single data point means little. What matters is the trend. Are your returns improving? Is your LVR reducing as values grow? Is your vacancy rate within acceptable bounds? Comparing current figures to previous periods reveals whether your optimisation is actually working.

- Triage actions by biggest impact: Resist the urge to fix everything simultaneously. Rank the issues you identify by their financial impact and your ability to act on them. A smarter investment workflow channels your effort toward the changes that move the needle most. Review relevant investment strategy examples to understand how other Australian investors have structured their decision-making processes.

The key discipline here is consistency. Monthly obsessing over metrics you cannot yet act on wastes energy. Quarterly or biannual reviews with clear action items are far more productive.

The uncomfortable truth about portfolio optimisation in Australia

Here is something most property content will not tell you directly: the majority of Australian investors who struggle with their portfolios are not struggling because they lack information. They are struggling because they lack systems.

We have all met the investor who has read every book, attended countless seminars, and can quote rental yield data from memory. Yet their portfolio is stagnant, their cash flow is tighter than it should be, and their next move is unclear. The problem is rarely knowledge. It is the absence of a regular, disciplined process for review and action.

The contrarian insight is this: portfolio optimisation is as much about deciding what to ignore as it is about what to improve. The pressure to constantly improve every property, refinance every loan, or reposition every asset leads to a kind of decision paralysis. As property portfolio management research makes plain, acting on the highest-impact issues first is what separates portfolios that improve from portfolios that stagnate.

Simple, robust systems consistently outperform clever, complex strategies. A straightforward tracking spreadsheet reviewed faithfully every six months beats an elaborate model reviewed never. The investor who acts on three clear metrics outperforms the one chasing fifteen signals across every property.

Your personal wealth optimisation guide does not need to be sophisticated. It needs to be real, honest, and applied consistently. That is the standard most investors avoid because it requires discipline rather than inspiration.

Take the next steps with AlphaIQ tools

Building disciplined systems for portfolio tracking and optimisation is exactly what AlphaIQ is designed to support. If the principles in this article have clarified what you need to track, the platform gives you the tools to actually do it, without the cost of ongoing financial advice.

Whether you are modelling the impact of refinancing on your portfolio LVR, running projections on your super to understand how property fits your retirement picture, or working through debt structuring decisions, AlphaIQ brings it all into one place. Use the debt recycling calculator to see how strategic debt management can improve your after-tax position, or explore the superannuation calculator to understand how your property wealth and super interact across your retirement timeline. The AlphaIQ platform is built for self-directed investors who want real numbers, not guesswork, backing every decision they make.

Frequently asked questions

What are the biggest mistakes people make when trying to optimise a property portfolio?

The biggest mistakes are tracking only individual property figures, neglecting overall debt structure, and failing to review performance regularly using portfolio-wide metrics such as IRR and combined LVR.

How often should you review your property portfolio performance?

A structured review at least every six to twelve months is the practical minimum, ensuring you catch emerging issues and adjust based on portfolio-wide benchmarks rather than reacting to individual property events.

What portfolio metrics actually matter for Australian investors?

The metrics that matter most are IRR, cash-on-cash return, portfolio LVR, debt-to-income ratio, and synchronised lease and cash flow cycles, as consistent benchmarking across these figures reveals your true position.

How do lender credit policies affect property portfolio optimisation?

Lender serviceability rules and credit buffers can block portfolio growth regardless of yield performance, so finance-first planning must account for how policy shifts interact with your household cash flow position.