TL;DR:

- Portfolio rebalancing maintains asset allocation and manages risk over time.

- Regular rebalancing improves long-term returns and reduces volatility, especially near retirement.

- Tax considerations, like capital gains tax, influence how and when investors should rebalance.

Your portfolio felt well-balanced when you first set it up. But markets move constantly, and what started as a carefully considered mix of assets can quietly shift into something you never intended. For self-directed Australian investors in their 40s, 50s, and 60s, this invisible drift is one of the most common and costly oversights in retirement planning. Portfolio rebalancing is the disciplined practice that keeps your strategy on track, and understanding how to do it well can make a meaningful difference to your retirement outcome.

Table of Contents

- What is portfolio rebalancing?

- How does portfolio rebalancing work?

- Key benefits of rebalancing your portfolio

- Risks and tax considerations for Australian investors

- Why rebalancing is your most underrated investment tool

- Take your portfolio rebalancing further with smarter tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Stay in control | Regular portfolio rebalancing helps you manage risk and align with your investment goals, especially as retirement approaches. |

| Understand your triggers | Knowing when and how to rebalance—by time or threshold—avoids costly mistakes and emotional decisions. |

| Watch for tax impacts | Consider capital gains tax and timing when selling assets as part of your rebalancing routine. |

| Use smart tools | Leverage calculators and digital platforms to simplify and track your rebalancing for better investment outcomes. |

What is portfolio rebalancing?

Portfolio rebalancing means adjusting your investments to maintain your chosen risk and asset mix. In simple terms, it is the act of buying and selling assets within your portfolio so that your allocation returns to your original target percentages.

Here is why this matters. Markets do not move evenly. Shares might surge 30% in a strong year while bonds remain flat. If you started with a 60% shares and 40% bonds split, that strong year might push your shares weighting to 72% or more. You have not made any active decisions, but your risk exposure has changed significantly.

Key insight: Left unchecked, a portfolio can drift far from its target allocation within just two to three years, especially during periods of strong equity market performance. The result is a risk profile that no longer matches your goals or your stage of life.

The consequences of ignoring this drift are real. As you approach retirement, carrying a higher-than-intended share weighting exposes you to greater volatility. A market correction at the wrong moment could reduce your retirement savings far more than your plan ever accounted for. This is sometimes called portfolio concentration risk, where too much of your wealth becomes tied to a single asset class or sector.

Common rebalancing timeframes include:

- Annual rebalancing: Reviewed and adjusted once per year, usually at the end of the financial year

- Semi-annual rebalancing: Reviewed every six months, often aligned with contribution cycles

- Threshold-based rebalancing: Triggered when an asset class drifts beyond a set tolerance, such as 5% above or below its target

Each approach has its place, and the right choice depends on your personal situation, the size of your portfolio, and how actively you want to manage your investments.

How does portfolio rebalancing work?

Understanding the mechanics of rebalancing helps you put it into practice with confidence. Financial advisors use scheduled (calendar) and tolerance band (threshold) strategies to rebalance portfolios. Both are legitimate, and many experienced investors use a combination of the two.

Here is a step-by-step overview of how rebalancing works in practice:

- Review your current allocation. Start by checking what percentage each asset class currently represents in your portfolio. Most online brokerage accounts and wealth platforms display this in a dashboard view.

- Compare against your target allocation. Identify which assets have grown beyond their target weighting and which have fallen below.

- Decide what action to take. You can sell overweighted assets and redirect the proceeds to underweighted ones, or simply direct new contributions toward the underweighted categories.

- Execute the trades or contributions. Place the transactions through your brokerage or platform, keeping transaction costs in mind.

- Record and review. Document the rebalancing and set a date for your next review.

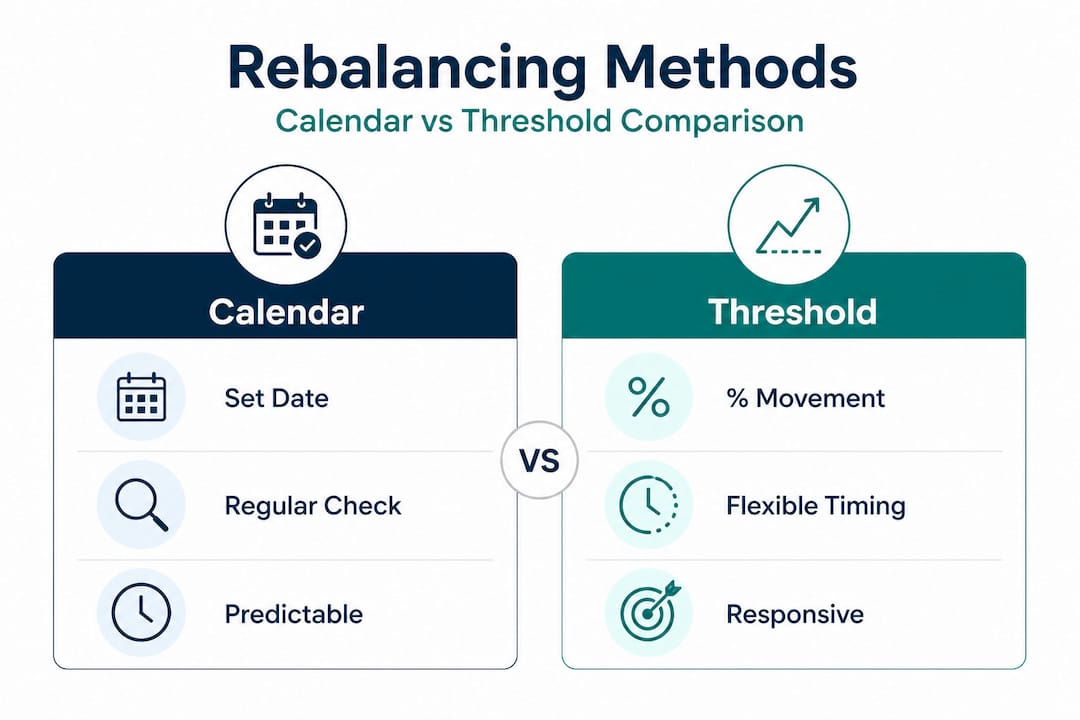

Calendar versus threshold rebalancing: a comparison

| Feature | Calendar rebalancing | Threshold rebalancing |

|---|---|---|

| Trigger | Set date (quarterly, annual) | Asset drifts beyond tolerance (e.g., 5%) |

| Predictability | High, easy to plan for | Variable, depends on market movements |

| Transaction frequency | Fixed and regular | Only when needed |

| Best suited to | Simpler portfolios, lower activity | Larger portfolios or volatile markets |

| Tax planning | Easier to time with financial year | May require more active CGT management |

The personal wealth optimisation guide outlines how combining both approaches, setting a calendar review but also triggering action when thresholds are breached, can give you the structure of a schedule with the responsiveness of a threshold system.

Modern Australian wealth platforms make this process much more manageable. Rather than manually tracking each asset's percentage across multiple accounts, digital tools can alert you when your allocation drifts beyond your tolerance band, making timely rebalancing much easier to achieve.

Pro Tip: Set a calendar reminder every 30 June to review your portfolio allocation. Aligning your rebalancing review with the end of the Australian financial year makes it easier to consider capital gains events in the context of your annual tax position.

Key benefits of rebalancing your portfolio

Now that we have covered the ways to rebalance your portfolio, it is important to look at exactly what you stand to gain by making it a core habit.

Regular rebalancing has been shown to improve returns and reduce portfolio volatility, especially approaching retirement. The advantages go well beyond simply keeping things tidy.

What rebalancing actually delivers

- Risk control you can rely on. Rebalancing prevents unintentional overexposure to a single asset class, which is particularly important as you enter the final decade before retirement. Carrying excess equity risk in your late 50s could leave you exposed to a market downturn at exactly the wrong time.

- Emotional discipline built into your process. One of the hardest aspects of investing is resisting the urge to chase recent performance. Rebalancing forces you to sell high-performing assets (sell high) and buy those that have underperformed (buy low). It is a natural counter to emotional decision-making.

- Long-term risk-adjusted returns. Research consistently shows that disciplined rebalancing tends to improve risk-adjusted outcomes over time, not necessarily because it maximises raw returns in every year, but because it reduces the severity of losses during downturns.

- Clarity for retirement planning. Knowing your portfolio is aligned with your target allocation gives you a clear, accurate picture of your financial position. This makes it far easier to model your retirement income with confidence.

Illustrative impact of rebalancing vs no rebalancing

| Scenario | Starting allocation | Allocation after 5 years (no rebalancing) | Allocation after 5 years (with rebalancing) |

|---|---|---|---|

| Australian shares | 60% | 74% | 60% |

| Fixed income | 30% | 18% | 30% |

| Cash and other | 10% | 8% | 10% |

| Estimated risk level | Moderate | High | Moderate |

The numbers in this illustration are hypothetical, but they reflect a realistic scenario based on how Australian equity markets have performed over multi-year periods. The key point is not the precise figures, but the direction of drift and what it means for your risk profile.

Understanding the value of advice versus DIY investing is also relevant here. Rebalancing is one of the highest-value activities a self-directed investor can perform, and it does not require paying for ongoing financial advice to do it well.

Risks and tax considerations for Australian investors

The benefits of rebalancing only add up when you avoid the pitfalls, especially the tax and cost considerations unique to Australian investors.

Selling assets during rebalancing can trigger tax consequences such as capital gains tax (CGT). CGT applies when you sell an asset for more than you paid for it. In Australia, if you hold an asset for more than 12 months, you are entitled to a 50% CGT discount, which is a significant benefit worth planning around.

Key risks and costs to watch for include:

- CGT on appreciated assets. If your Australian shares have grown significantly and you sell to rebalance, you will likely trigger a CGT event. The taxable gain forms part of your assessable income for that financial year, which could push you into a higher tax bracket.

- Transaction costs. Brokerage fees, buy-sell spreads on managed funds, and platform fees all add up. Frequent rebalancing in smaller portfolios can erode the very gains you are trying to protect.

- Timing matters for CGT. If you are approaching the end of the financial year, consider whether delaying a sale until after 30 June might shift the CGT event into the following financial year, giving you more time to plan.

- Franking credits and tax-effective income. Australian dividend investors should factor in franking credits when assessing the after-tax return of different assets. Selling franked dividend-paying shares to rebalance may reduce the franked income you receive.

Smarter ways to rebalance with tax in mind

Rather than always selling to rebalance, there are gentler approaches:

- Redirect new contributions. Direct your next superannuation contribution, share purchase, or cash investment toward your underweighted asset classes. This rebalances your allocation without triggering a sale and therefore avoids CGT entirely.

- Harvest tax losses. If some holdings are currently at a loss, selling them to offset gains elsewhere can reduce your overall CGT liability.

- Rebalance inside super. Switching between investment options within your superannuation fund generally does not trigger personal CGT, making it one of the most tax-effective rebalancing environments available to Australian investors.

Using a CGT calculator before executing a rebalancing trade can help you understand the after-tax impact before you commit. This is especially valuable for investors holding large positions with significant unrealised gains.

Pro Tip: Always model your rebalancing decisions using a tax-aware investing framework before executing. Knowing the estimated tax cost of each trade allows you to sequence your rebalancing in the most cost-effective way possible, sometimes over two financial years rather than one.

Why rebalancing is your most underrated investment tool

Here is a perspective that many investment conversations overlook. The biggest gains most Australian investors leave on the table are not from picking the wrong stocks or missing a market rally. They come from allowing their portfolio to drift, carrying too much risk when markets are high, and then suffering disproportionate losses when conditions turn.

Rebalancing is rarely celebrated the way stock-picking is. It does not make for exciting conversation at a dinner party. But the investors who consistently build wealth over 20 and 30-year horizons are almost always the ones who stayed disciplined, rebalanced regularly, and did not let their emotions override their strategy.

There is also a psychological element worth naming directly. When a particular asset class has performed well for three or four years running, it feels counterintuitive to sell some of it. Everything tells you to hold on, or even buy more. But that is precisely when your allocation has likely drifted furthest from its target, and when trimming back to your original weighting makes the most sense from a risk management perspective. Letting portfolio risk accumulate silently is far more dangerous than the discomfort of selling a winner.

The Australian market also has its own characteristics that make disciplined rebalancing particularly valuable. Our market is heavily weighted toward financials and resources, which means a passive, untouched portfolio can become very concentrated in a handful of sectors. Self-directed investors who review and rebalance regularly are far better placed to hold a genuinely diversified portfolio over time.

The lesson from decades of investor outcomes is simple. Behaviour matters more than brilliance. Rebalancing is one of the few evidence-based behaviours that consistently improves long-term outcomes, not by increasing your returns in every year, but by reducing the damage in bad years and keeping you in the game long enough for compounding to do its work.

Take your portfolio rebalancing further with smarter tools

Rebalancing is most powerful when it is easy to monitor and act on. The more clearly you can see your current allocation, your drift from target, and the tax implications of any adjustments, the better your decisions will be.

AlphaIQ is built for exactly this kind of active, informed self-direction. With tools like the superannuation calculator and the debt recycling calculator, you can model how rebalancing decisions interact with your broader financial position, including your super balance, your property debt, and your projected retirement income. The AlphaIQ platform brings together tax-aware modelling and scenario simulation so you can see the real numbers before you act, giving you the confidence to rebalance strategically rather than reactively. For self-directed investors who want to stay in control without paying for ongoing financial advice, it is exactly the kind of intelligent support that makes a genuine difference.

Frequently asked questions

How often should I rebalance my portfolio as I approach retirement?

Most experts recommend annual or semi-annual rebalancing, but more frequent reviews may suit those close to retiring or with larger asset fluctuations. The closer you are to your target retirement date, the more important it becomes to maintain your target allocation.

Does portfolio rebalancing trigger capital gains tax in Australia?

Yes, selling appreciated assets during rebalancing can lead to capital gains tax (CGT) events. Planning your rebalancing around the Australian financial year and the 12-month CGT discount can help minimise the tax impact.

Can I use new investment contributions to rebalance?

Yes, directing new contributions to underweighted assets is one of the most tax-effective ways to rebalance, as it avoids selling assets and the potential CGT consequences that follow.

Are there digital tools for monitoring and rebalancing portfolios?

Yes, several personal wealth platforms offer automated tracking and rebalancing alerts for Australian investors, making it far easier to spot drift and act before it significantly changes your risk profile.