TL;DR:

- Property investment modelling estimates performance using detailed financial data and scenario testing.

- It helps uncover hidden costs, compare properties, and assess risks for more confident investment decisions.

- Self-directed investors can use online tools to build models, but complex portfolios may require professional advice.

Property investment is often treated as a guaranteed path to wealth in Australia. Buy the right place, hold it long enough, and the returns will come. But this assumption carries real risk. Markets shift, interest rates climb, vacancies drag on, and unexpected costs stack up quickly. Without a clear picture of the numbers, even experienced investors can find themselves stretched thin. This article explores what property investment modelling actually involves, why it matters for self-directed investors, and how you can start using it to make sharper, more confident decisions with your portfolio.

Table of Contents

- What does it mean to model property investment?

- Benefits of modelling your property investments

- What goes into a property investment model?

- Risks of property investment without robust modelling

- How to start modelling your own property investments

- The real value of modelling: Our perspective

- Model your property investment with confidence

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Better decisions | Modelling your property investment lets you see opportunities and risks before committing your money. |

| Identify hidden costs | Factors like interest changes, repairs and vacancies can be planned for—not just guessed. |

| Compare scenarios | Testing different models side-by-side helps you choose properties that fit your goals and tolerance for risk. |

| DIY tools available | Today’s calculators and online resources make robust modelling accessible for self-directed Australians. |

What does it mean to model property investment?

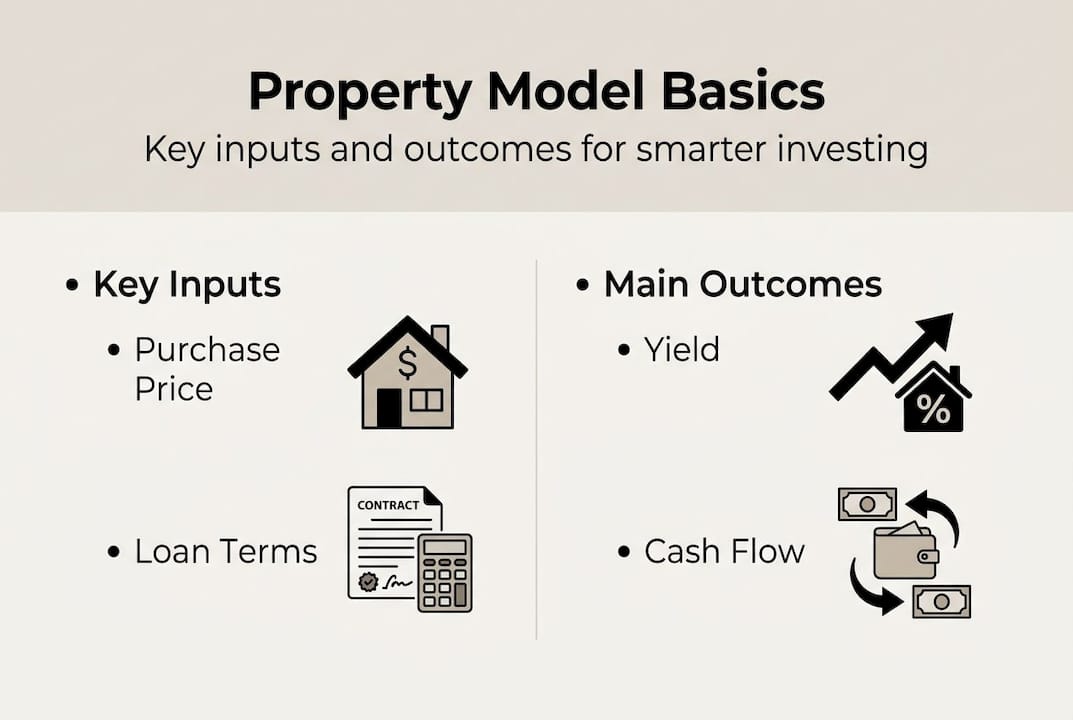

Property investment modelling is the process of using financial data and structured calculations to estimate how a property will perform over time. It moves you away from gut-feel decisions and into a world of clear, testable projections. Think of it as building a detailed financial picture of a property before you commit a single dollar.

Financial modelling estimates the real, after-cost returns of a property over time, accounting for everything from mortgage repayments and maintenance to rental income and capital growth assumptions.

A well-built property model typically draws on inputs like:

- Purchase price and stamp duty

- Loan amount, interest rate, and repayment structure

- Estimated rental yield and vacancy allowance

- Annual costs including rates, insurance, property management fees, and repairs

- Capital growth assumptions based on historical data and suburb trends

- Tax implications such as negative gearing and depreciation benefits

Many investors skip this step because they believe property is inherently low-risk, or because modelling sounds like something only finance professionals do. Neither assumption holds up. The truth is that estimating property returns is now accessible to any motivated investor who is willing to gather reliable data and use the right tools.

Scenario planning is another key part of modelling. Rather than running one set of numbers, a good model tests multiple futures. What happens if the interest rate rises by 1.5%? What if the property sits vacant for three months? What if growth comes in half of what you projected? These scenarios reveal how resilient your investment really is, and whether you can absorb shocks without serious financial damage.

Modelling does not predict the future. It maps out a range of realistic outcomes so you can choose the path that suits your financial position and risk tolerance.

For self-directed investors, this kind of structured thinking is especially valuable. You are the one making the decisions, and the quality of those decisions depends entirely on the quality of your information.

Benefits of modelling your property investments

Modelling delivers practical, measurable advantages that raw research alone simply cannot match. Modelling allows you to forecast cash flow, tax implications, and returns well before you commit, giving you a critical edge in evaluating any opportunity.

Here are four concrete benefits worth understanding:

- Uncovers hidden costs. Maintenance, landlord insurance, strata fees, and property management charges are easy to overlook. A model forces you to account for all of them upfront.

- Compares multiple properties side by side. Rather than relying on instinct, you can evaluate two or three properties against the same set of assumptions and see which one performs better for your goals.

- Clarifies your tax position. Negative gearing, depreciation schedules, and capital gains tax all affect your real return. Modelling integrates these into a single picture.

- Shows how property fits your broader financial plan. A strong investment in isolation can still be a poor fit if it strains your cashflow or derails other secure retirement strategies.

| Scenario | Without modelling | With modelling |

|---|---|---|

| Vacancy of 4 weeks | Surprise shortfall | Already budgeted |

| Rate rise of 1% | Cashflow stress | Pre-tested resilience |

| Below-average growth | Unmet expectations | Adjusted projections |

| Hidden costs emerge | Budget blowout | Factored in advance |

Pro Tip: When comparing two properties, run the same scenario assumptions across both models. Changing variables like growth rate or vacancy period separately for each property makes comparison unreliable.

The property investment tips offered by ASIC's MoneySmart reinforce the importance of understanding total costs and realistic return expectations before purchasing. Good wealth optimisation steps always begin with the numbers, not the narrative.

What goes into a property investment model?

Now that you understand the value modelling delivers, it helps to look more closely at what actually goes into one. Key inputs such as purchase price, loan details, rent, and expenses form the foundation of any property model, with each variable directly influencing your projected outcomes.

| Input | What it affects | Where to source it |

|---|---|---|

| Purchase price | Borrowing capacity, stamp duty, yield | Contract of sale, market comparables |

| Loan interest rate | Monthly repayments, cashflow | Lender quotes, RBA cash rate |

| Rental yield | Weekly income, gross return | Property manager estimates, suburb data |

| Vacancy allowance | Net income, holding costs | Local vacancy rate data |

| Capital growth rate | Long-term wealth projection | Historical suburb performance |

| Maintenance and costs | Net cashflow, tax deductions | Building inspection reports, averages |

Each variable matters. Changing your assumed capital growth rate from 5% to 3.5% across a ten-year model can shift your projected return by hundreds of thousands of dollars. That is not a trivial difference.

Some critical considerations when building your model:

- Use conservative estimates for growth and optimistic estimates for costs. Markets sometimes underperform; costs rarely do.

- Source your data from credible places. Market statistics from the Property Council of Australia and state-specific valuation bodies are reliable benchmarks.

- Factor in RBA rate impacts by testing your model at multiple interest rate levels, not just the current rate.

- Use tax-aware investing principles to ensure your model captures real after-tax returns, not just gross figures.

Pro Tip: Stress-test your model by running a "worst case" scenario where growth is flat, vacancy runs at 8%, and rates rise by 2%. If the property still works within acceptable limits, you have a resilient investment.

Reliable inputs produce reliable projections. Garbage in, garbage out. Taking the time to gather quality data is the most important thing you can do before running a single calculation.

Risks of property investment without robust modelling

Without a structured model, most investors rely on a combination of optimism and incomplete information. That is a vulnerable position. Skipping due diligence and financial modelling is one of the main contributors to poor property investment outcomes.

The most common unmodelled risks include:

- Vacancy gaps. Even a well-located property can sit empty for weeks. Without a vacancy buffer in your cashflow, this creates immediate financial pressure.

- Interest rate spikes. Variable rate loans expose investors to repayment increases that can quickly turn a positively geared property into a cashflow drain.

- Unexpected repairs. Older properties especially carry maintenance risk. A single major repair like a roof replacement or plumbing failure can wipe months of rental income.

- Over-leverage. Borrowing at maximum capacity leaves no room to absorb shocks. Poor liquidity planning is one of the fastest routes to a forced sale at the wrong time.

Emotional decision-making in property often means buying based on how a suburb "feels" rather than what the numbers actually support. Feelings do not pay mortgages.

Consider a real-world scenario. An investor purchases a property based on an agent's optimistic rental appraisal and projected suburb growth. No formal model is run. Within 18 months, the property sits vacant for six weeks, two rate rises push repayments up significantly, and a plumbing issue costs $8,000 to fix. The investor had not budgeted for any of these events.

Tracking market volatility through ABS building approval data can also signal shifts in supply that affect rental demand. This is the kind of contextual data that strengthens a model and sharpens decisions.

Understanding the costs of DIY investing also means acknowledging when missing information creates real financial exposure. Investors who model risk factors upfront are far better placed to respond calmly when conditions change.

How to start modelling your own property investments

Getting started is more straightforward than most investors expect. DIY investors now have access to sophisticated calculators and modelling tools, once reserved for professionals.

Follow these steps to build your first property model:

- Gather your data. Collect the purchase price, current rental estimates from a local property manager, a building inspection report, and your preferred loan terms. This is your raw material.

- Choose your scenarios. Define a base case, a conservative case, and a stress case. Vary your growth rate, vacancy, and interest rate across each one.

- Run the numbers. Use an online calculator or spreadsheet to calculate weekly cashflow, annual return, and projected equity over five, ten, and twenty years.

- Interpret the results. Look at how sensitive the investment is to changes in key variables. If a 1% rate rise moves you from positive to deeply negative cashflow, that is a risk you need to price consciously.

- Apply to your search. Use the model as a filter, not just an evaluation tool. Properties that do not pass your base-case criteria can be set aside quickly.

For property investment optimisation, tools like the negative gearing calculator from AlphaIQ let you test tax outcomes across different scenarios before you commit. Canstar's property investing guide also offers useful benchmarks for comparing loan structures and return expectations.

Pro Tip: Review your retirement calculators alongside your property model. Seeing how property income integrates with your superannuation projections gives you a far more complete picture of your retirement readiness.

When your model flags something you are unsure how to interpret, that is a good time to seek professional input. Modelling does not replace expertise, but it makes any professional conversation far more productive.

The real value of modelling: Our perspective

Most investors we hear from assume modelling is something you do after you have found a property you love. We think that gets it backwards. Modelling should shape the search, not follow it.

The real shift that modelling creates is not technical. It is psychological. When you have clear numbers in front of you, emotions take a back seat. You stop asking "does this feel right?" and start asking "does this work?"

The investors who consistently outperform are rarely those with the best instincts. They are the ones who run the numbers with rigour, test the downside scenarios, and make decisions from a position of clarity rather than excitement. This approach to maximising your wealth is not reserved for professionals with Bloomberg terminals. It is available to any self-directed investor willing to spend a few hours with the right tools.

Property wealth is built over decades. Small improvements in decision quality, repeated consistently, produce significantly better outcomes. Modelling is how you make better decisions, consistently.

Model your property investment with confidence

If you are ready to move from guesswork to clarity, AlphaIQ gives you the tools to do exactly that.

The AlphaIQ platform brings together tax-aware property modelling, scenario simulation, and retirement projections in one place, designed specifically for self-directed Australian investors. You can model negative gearing outcomes, test different loan structures, and see how property integrates with your superannuation using the superannuation calculator. For investors carrying home loan debt, the debt recycling calculator shows how strategic debt management can accelerate your wealth position. No ongoing advice fees. Just real numbers, built around your situation.

Frequently asked questions

What is property investment modelling in plain terms?

It uses formulas and financial data to predict how a property investment will perform over time, accounting for purchase cost, rent, expenses, and market growth. Financial modelling estimates the real, after-cost returns of a property over its full holding period.

What are common risks if I don't model my property investments?

You could underestimate costs, overestimate returns, and be completely unprepared for vacancies or interest rate jumps, leading to serious financial stress. Skipping financial modelling is one of the main contributors to poor property investment outcomes.

Which inputs are most important for a solid property investment model?

The most critical variables are purchase price, loan terms, likely rental income, ongoing costs, expected growth, and market volatility. Key inputs such as purchase price, loan details, rent, and expenses form the foundation of any reliable model.

Can I model property investments myself, or do I need an expert?

Self-directed investors can use online calculators and simple models with confidence, though complex multi-property portfolios may benefit from professional review. DIY investors now have access to sophisticated modelling tools that were once only available to professionals.