TL;DR:

- Personal finance modeling helps project wealth, test scenarios, and improve decision-making with accurate data.

- Regularly update your inputs and assumptions to keep projections realistic and aligned with current benchmarks.

- Building a habit of revisiting and adjusting your model ensures effective retirement planning and financial resilience.

You've spent years building your wealth, contributing to super, and making investment decisions. But without a clear picture of where you're headed, it's hard to know if you're on track. Personal finance modelling changes that. It gives you a structured, evidence-based way to project your future wealth, test different scenarios, and make decisions backed by real numbers, not guesswork. This guide walks you through everything you need: what to prepare, how to build your model, common mistakes to sidestep, and how to know it's working. Whether you're 15 years from retirement or 5, this process gives you genuine control.

Table of Contents

- What you need before you start

- Step-by-step finance modelling process

- Common mistakes and pitfalls in modelling

- How to know your model is working

- Our perspective: What most people miss in finance modelling

- Try advanced tools to streamline your modelling

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Start with the right data | Accurate, up-to-date inputs are essential for reliable modelling outcomes. |

| Use trusted calculators | Combine online tools with spreadsheets to cross-check and enhance your finance model. |

| Regularly update benchmarks | Stay aligned with evolving standards by reviewing your model against ASFA and Moneysmart figures. |

| Avoid common mistakes | Stress-test for negative events and adjust for personal factors like career breaks and health. |

| Let your model evolve | Make your finance model a living plan, not a one-off exercise—review it annually and after major life changes. |

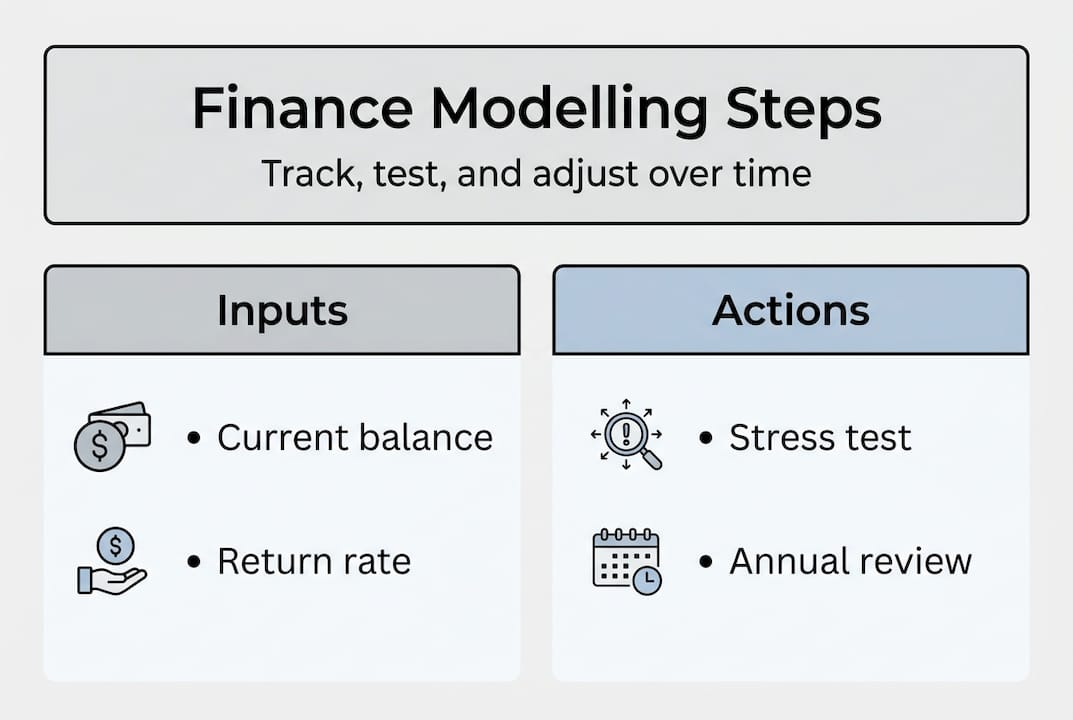

What you need before you start

Now that you appreciate why modelling matters, let's clarify what you'll need before starting. The single biggest mistake most people make is diving into a spreadsheet before they have accurate data. Garbage in, garbage out. Your model is only as good as the numbers you feed it.

Start by documenting your current financial position. That means:

- Income: Your salary, investment distributions, rental income, and any other regular sources

- Savings and investments: Bank balances, share portfolios, managed funds, and ETFs

- Superannuation balance: Your current balance and which fund you're in

- Debts: Mortgage, personal loans, credit cards, and their interest rates

- Age and retirement target: When you plan to stop working and what lifestyle you want

Knowing your super balance relative to your peers is a useful reality check. Super benchmarks by age show that the average for Australians aged 35 to 39 is around $80,900. If you're significantly below that, your model needs to reflect a more aggressive contribution strategy.

Here's a practical overview of what's essential versus what's useful but optional:

| Essential inputs | Nice-to-have additions |

|---|---|

| Current super balance | Estimated Age Pension entitlement |

| Gross annual income | Investment portfolio breakdown by asset class |

| Total debts and interest rates | Historical return data for your fund |

| Target retirement age | Expected inheritance or windfalls |

| Expected annual retirement spending | Planned lump sum contributions |

For establishing a solid baseline, use a reliable super calculator to project your balance forward before building anything more complex. Pair that with a review of published retirement benchmarks from ASFA, which are updated regularly and give you a credible target to model towards.

A common misconception is that modelling requires complex software or financial expertise. It doesn't. What it requires is accurate information and a willingness to be realistic. Many investors overestimate future returns, particularly for growth assets, which skews projections and creates false confidence. Use conservative assumptions from the outset.

If you're not sure where to begin with broader planning, reviewing retirement planning steps gives you a useful framework before modelling your numbers.

Pro Tip: Keep a single document or spreadsheet that holds all your key financial figures. Update it every six months. This alone will save you hours each time you revisit your model.

Step-by-step finance modelling process

With your information and tools at hand, follow these core steps to start modelling.

-

Gather all your data. Pull together your income, expenses, super balance, debt levels, and existing investment balances. This is your starting snapshot.

-

Set your base assumptions. Choose conservative but realistic inputs: an investment return between 4% and 7% per year, an inflation rate of 2.5% to 3%, and account for fund fees. These three variables have the most impact on your output.

-

Choose your modelling tool. You can use Excel, Google Sheets, or an online calculator. Why calculators matter for Australian investors comes down to speed and accuracy, especially when you want to run multiple scenarios quickly.

-

Input your current details. Enter your age, super balance, annual contributions (including employer contributions), and current net income. Add your debts and any regular investment contributions outside super.

-

Model contributions, lump sums, and scenarios. Now run variations: What happens if you contribute an extra $10,000 per year to super? What if you retire at 62 instead of 65? What if investment returns average only 4%?

Here's a sample to illustrate how different assumptions shift your outcome:

| Scenario | Return assumption | Retirement age | Projected super at 67 |

|---|---|---|---|

| Conservative | 4% | 67 | $480,000 |

| Moderate | 5.5% | 67 | $620,000 |

| Optimistic | 7% | 67 | $810,000 |

| Early retirement | 5.5% | 62 | $510,000 |

As DIY modelling strategies illustrate, replicating industry super fund approaches in your own model means testing returns across 4% to 7%, accounting for fees, and incorporating Age Pension thresholds.

The Moneysmart super guidance consistently recommends using online calculators to build personal projections, and applying conservative return assumptions to avoid over-confidence in your forecasts.

"Assume investment returns lower than past averages for conservatism." This principle keeps your model grounded in realistic expectations, not the best-case story.

Use your super projection tool to run these variations quickly and see the outputs side by side.

Pro Tip: Always stress-test your model against a negative return year, such as a 10% to 15% portfolio loss. This reveals how resilient your plan is and whether you need a cash buffer in place before retirement.

Common mistakes and pitfalls in modelling

Even with a solid model, avoid the classic mistakes below to stay on track.

-

Ignoring updated benchmarks. Super averages and retirement standards shift every quarter. A model built on two-year-old data may significantly misrepresent your position.

-

Using unrealistic return assumptions. Assuming 8% or 9% annual returns feels optimistic but often leads to a nasty shortfall. Markets go through sustained flat or negative periods. Your model should reflect that.

-

Not modelling Age Pension eligibility. Many Australians will qualify for a part Age Pension, and ignoring this dramatically undersells your retirement income. The assets test and income test both affect what you receive.

-

Neglecting longevity. Australians are living longer. A 65-year-old today may need to fund 25 to 30 years of retirement. Model to age 90 or 95, not 80.

-

Set-and-forget behaviour. A model built three years ago doesn't reflect your current salary, updated super balance, or the property you refinanced. It needs regular attention.

Women and career breaks deserve specific mention here. Super benchmarks and outcomes show that interruptions to contributions due to parenting, illness, or part-time work have a compounding negative effect over time. If this applies to you, your model needs to account for lower contribution years and adjusted projections.

"Optimal: Balance growth assets early, shift conservative near retirement." This insight reflects how asset allocation should evolve over time, and your model needs to mirror that transition rather than holding static assumptions throughout.

When thinking about planning retirement income, the sequencing of withdrawals and the tax treatment of different income streams makes a material difference. Build those considerations into your model, not just the accumulation phase.

Pro Tip: Set a calendar reminder for the same time each year to review your model. Treat it like an annual tax return. It keeps your assumptions current and your decisions grounded in reality.

How to know your model is working

Once you're avoiding pitfalls, keep your model aligned with reality using these strategies.

The clearest way to validate your model is to compare its outputs against published benchmarks. ASFA retirement standards confirm that a single person needs $54,840 per year and approximately $630,000 in superannuation at age 67 to fund a comfortable retirement (December 2025 figures). If your model projects well below this, it's a signal to adjust contributions or expectations.

Checkpoints to assess model accuracy:

- Annual super balance check: Compare your actual balance to your model's projection for this year

- Income tracking: Does your current gross income match what you entered? Update if you've had a pay rise or career change

- Net wealth comparison: Add up assets minus liabilities and compare to your model's net wealth projection

- Age Pension eligibility test: Run the current assets and income test figures to see if your model's estimate still holds

- Drawdown rate review: In retirement, confirm that your withdrawal rate (typically 4% to 5% per year) remains sustainable given your actual balance

Here's a practical comparison to illustrate how to track model accuracy:

| Measure | Model projection | Actual figure | Action if gap exists |

|---|---|---|---|

| Super balance at 50 | $320,000 | $295,000 | Increase contributions or review fund performance |

| Annual investment return | 5.5% | 3.8% | Lower return assumption; stress-test plan |

| Retirement spending target | $65,000/yr | $72,000/yr | Adjust spending assumptions or extend working years |

| Net wealth at 60 | $1.1M | $980,000 | Review debt reduction and savings strategy |

For context on how much super you need to retire at 60, the threshold is meaningfully different to retiring at 67, and your model should capture that gap clearly. Exploring tax-free retirement income tips can also help you model the tax side of your retirement income more accurately, since not all income sources are taxed the same way.

The goal isn't perfection. It's consistent tracking and small corrections over time. A model reviewed and adjusted annually is far more valuable than a perfect model built once and abandoned.

Our perspective: What most people miss in finance modelling

Here's an uncomfortable truth. Most self-directed investors spend 80% of their effort getting the spreadsheet formula right and almost no time actually using the model to change their behaviour.

The maths matters, but it's not what creates wealth. What creates wealth is the habit of returning to your model, updating it honestly, and letting it inform real decisions: whether to make a voluntary super contribution before 30 June, whether to optimise property investment ahead of retirement, or whether your current trajectory is genuinely on track.

The investors who get the most from modelling treat it as a living document, not a one-off calculation. They're not chasing a perfect model. They're building a planning habit. When a career change happens, a property is sold, or markets fall sharply, they already have a framework to assess the impact and adjust. That responsiveness is what separates people who reach retirement with clarity from those who arrive uncertain and underprepared. Build the model, yes. But more importantly, build the habit of using it.

Try advanced tools to streamline your modelling

If you're ready to take the next step, explore tools that can simplify and amplify your finance modelling.

Manually updating spreadsheets is time-consuming and easy to get wrong. AlphaIQ removes that friction.

The AlphaIQ platform brings together tax-aware super projections, scenario modelling, and retirement income planning in one place. You can run your numbers against current benchmarks, model the impact of extra contributions, and stress-test your plan without needing a financial adviser on retainer. Tools like the AlphaIQ super calculator and the debt recycling calculator give you the kind of clarity that used to require an expensive consultation. Start modelling with confidence today.

Frequently asked questions

What is personal finance modelling in Australia?

Personal finance modelling means projecting your future wealth, income, and superannuation based on your own inputs and goals, using calculators or spreadsheets. Moneysmart recommends calculators for building these personal projections accurately.

How often should I update my finance model?

Review and update your model at least once a year and after any major financial change, such as a new role, property transaction, or significant market event. Benchmarks evolve quarterly, so keeping your inputs current ensures your projections remain reliable.

Do I need an accountant or adviser for personal finance modelling?

Most Australians can manage DIY modelling effectively using online tools, and many replicate industry fund strategies in their own models without professional help. For complex situations involving SMSFs or tax structuring, a professional check is worthwhile.

What return rate should I assume in my model?

A conservative range of 4% to 7% per year is standard for personal modelling, with lower figures used for stress-testing. The ASFA Retirement Standard uses a 6% investment return assumption for comfortable retirement modelling.

How can I tell if my model is on track?

Compare your projected super balance and net wealth against current ASFA benchmarks each year, and adjust your assumptions whenever there's a meaningful gap between your model and reality.