TL;DR:

- Passive income is earned from assets or activities that require little ongoing active work. It is taxed at your marginal rate, but franking credits and capital gains discounts can reduce the tax burden. Building a diversified portfolio of dividend stocks, property, bonds, and REITs requires patience and regular management to achieve sustainable income.

Passive income is money earned from assets or activities that require little to no ongoing active work. The Australian Taxation Office and financial institutions broadly define it as earnings from rental properties, dividend-paying stocks, royalties, or silent business partnerships where you do not materially participate day to day. Unlike active income, which you earn by trading your time for a salary or wage, passive income works independently of your hours. Passive income is not a get-rich-quick scheme but a slow compounding process that, built correctly, supports genuine financial independence in Australia.

What is passive income and how does it differ from active income?

Passive income is defined as earnings generated from assets or business interests where your direct, ongoing labour is not the primary driver. Active income, by contrast, stops the moment you stop working. A salary, consulting fee, or hourly wage all require your continuous participation to keep flowing.

The clearest way to see the difference is through examples. A rental property generates rent whether you are at your desk or on holiday. A portfolio of dividend-paying shares from companies like BHP or Commonwealth Bank deposits income into your account each quarter. Royalties from a published book or licensed patent pay you each time someone uses that work. None of these require you to clock in.

The core philosophy of passive income is shifting the relationship between time and money. Once an asset is established and producing income, your time is freed for other priorities, whether that is building more assets, spending time with family, or retiring earlier than the standard age.

What are the common types and examples of passive income in Australia?

Australia offers several well-established avenues for generating passive income. Each carries a different risk profile, capital requirement, and level of ongoing involvement.

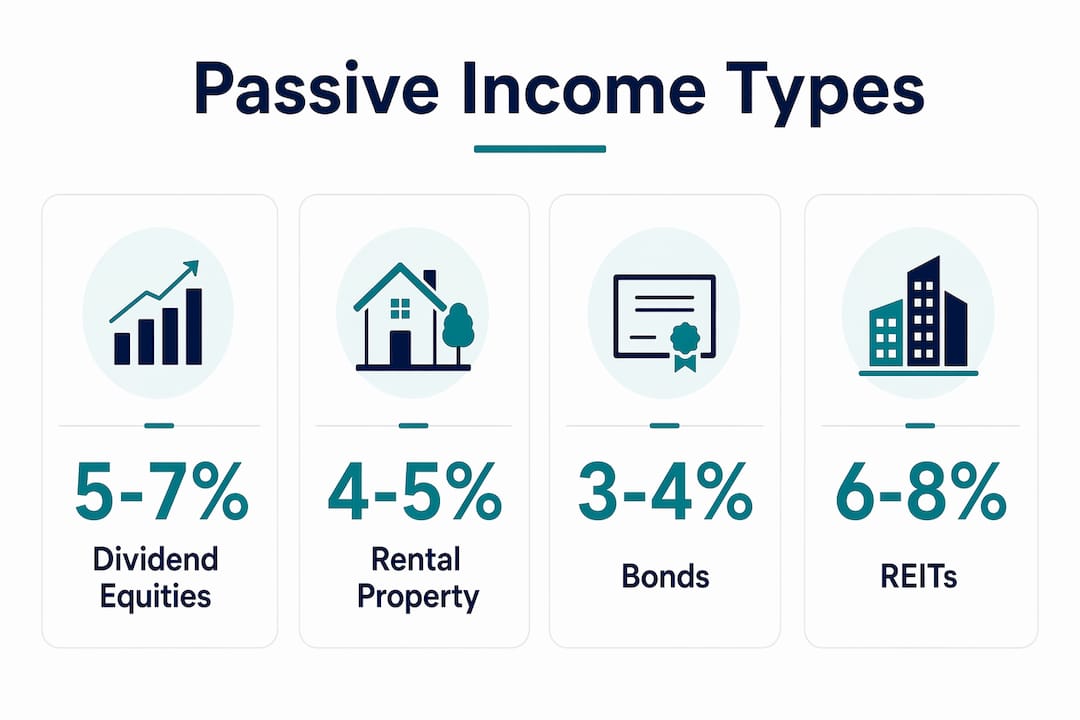

- Dividend stocks: Shares in ASX-listed companies pay regular dividends. Australian dividends often come with franking credits, which reduce your tax liability by passing on tax already paid at the company level.

- Rental properties: Residential and commercial property generates rental income. Costs include mortgage interest, rates, insurance, and property management fees.

- Real Estate Investment Trusts (REITs): Listed on the ASX, REITs let you invest in property without owning it directly. They distribute a large portion of rental income to unitholders.

- Bonds and fixed income: Government and corporate bonds pay regular interest. They provide stability and predictability, though yields are typically lower than equities.

- Royalties: Income from intellectual property such as books, music, software, or patents. Upfront creative or development work generates ongoing payments.

- Peer-to-peer lending and high-yield savings: Less common but growing in Australia, these generate interest income with varying degrees of risk.

Pro Tip: Franking credits on Australian dividends are one of the most tax-efficient passive income features available to local investors. If your marginal tax rate is below the company tax rate of 30%, you may receive a tax refund on top of your dividend income.

A well-constructed passive income portfolio typically blends several of these sources. For property-specific strategies, smart property investment tips for Australian investors outline how to build a property base that supports retirement income.

Is passive income taxable in Australia?

Passive income is generally taxed at your marginal tax rate, similar to earned income. The Australian Taxation Office does not apply a blanket concessional rate simply because income is passive. However, specific investment types do qualify for preferential treatment depending on how and when the income is generated.

Key tax considerations for Australian passive income investors include:

- Rental income: Declared as assessable income in your tax return. Deductible expenses include interest, depreciation, repairs, and management fees. Negative gearing allows losses to offset other income.

- Dividends: Taxed as income, but franking credits offset tax already paid by the company. Investors on lower marginal rates can receive refunds.

- Capital gains: Assets held for more than 12 months attract a 50% capital gains tax discount for individuals.

- Interest income: Fully assessable at your marginal rate with no concessions.

Rental activities are passive unless you qualify as a real estate professional under ATO definitions. This classification affects how losses are treated and whether they can offset your other income. The ATO's rules around material participation mirror the framework used by the IRS in the United States, where passive activities are defined as those in which you work fewer than 500 hours per year.

Pro Tip: Tax planning for passive income is not a once-a-year task. Reviewing your income mix, deductions, and franking credit position before 30 june each year can materially reduce your tax bill.

What strategies build sustainable passive income portfolios?

A sustainable passive income portfolio does not rely on a single source. Concentration in one asset class exposes you to sector-specific risk. A blended approach across equities, property, and fixed income produces more consistent income across different market conditions.

A well-cited model is the three-bucket income portfolio. A diversified portfolio of approximately $1.1 million across dividend equities, bonds, and REITs can yield approximately 5.7%, generating around $5,192 per month. That figure gives you a concrete capital target to work backwards from based on your income needs.

| Asset class | Typical yield range | Role in portfolio |

|---|---|---|

| Dividend equities (ASX) | 4%–6% (plus franking) | Growth and income |

| REITs | 4%–6% | Property exposure without direct ownership |

| Bonds and fixed income | 3%–5% | Stability and predictable cash flow |

| High-yield savings or term deposits | 4%–5% | Liquidity and capital preservation |

Income investing requires a whole portfolio approach that blends income and growth assets. Focusing only on yield without considering capital preservation leads to portfolios that erode in real terms over time.

High dividend yields can indicate company distress rather than strength. Experienced investors assess payout ratios and dividend growth history alongside the headline yield figure. A 10% yield from a company cutting its dividend is worth far less than a 5% yield from a company growing its payout annually.

Regular rebalancing keeps your portfolio aligned with your income targets and risk tolerance. Strategies for rebalancing your portfolio explain how to maintain the right mix without triggering unnecessary capital gains events.

Pro Tip: Reinvesting dividends and distributions during your accumulation phase accelerates compounding significantly. Even a modest portfolio grows faster when income is reinvested rather than spent.

What are the practical steps and common pitfalls for beginners?

Building passive income follows a clear sequence. Skipping steps is the most common reason investors underperform or give up early.

- Define your income target. Work out how much monthly passive income you need and by when. This determines the capital required and the yield you need to target.

- Assess your starting capital. Passive income requires upfront capital or time. A rental property needs a deposit. A dividend portfolio needs seed funds. A royalty stream needs creative output or development time.

- Choose your asset mix. Match your income sources to your risk tolerance, tax position, and time horizon. Younger investors can accept more volatility. Those closer to retirement prioritise stability.

- Automate where possible. Set up dividend reinvestment plans (DRPs) through your broker. Use direct debit for mortgage repayments on investment properties. Automation reduces the ongoing effort required.

- Review regularly. Passive income requires upfront effort and ongoing maintenance, even if that maintenance is minimal. Managing tenants, rebalancing portfolios, and reviewing tax obligations are all recurring tasks.

Common pitfalls to avoid:

- Chasing the highest yield without assessing sustainability

- Ignoring tax obligations until they become a problem

- Failing to diversify across asset classes or geographies

- Underestimating the time and cost of property management

- Expecting meaningful income from a small starting capital base

Income investing is not set-and-forget. Investors who treat it as fully automatic tend to find their portfolios drifting out of alignment with their goals over time.

For a broader framework on building a diversified base, portfolio diversification strategies for Australians cover how to spread risk across asset classes without overcomplicating your structure.

Key takeaways

Passive income is most reliably built through a diversified portfolio of dividend equities, property, bonds, and REITs, maintained with regular reviews and realistic capital targets.

| Point | Details |

|---|---|

| Definition is clear | Passive income comes from assets or activities where you do not actively work day to day. |

| Tax treatment matters | Australian passive income is taxed at your marginal rate, but franking credits and the CGT discount reduce the burden. |

| Capital targets are concrete | A portfolio of around $1.1 million at a 5.7% yield can generate approximately $5,192 per month. |

| Diversification reduces risk | Blending dividend stocks, REITs, and bonds produces more consistent income than any single source. |

| Ongoing management is required | Passive income is not fully automatic. Regular reviews, rebalancing, and tax planning are necessary. |

Why I think most people misunderstand passive income

Most people hear "passive income" and picture a beach, a laptop, and money arriving while they sleep. That image is not wrong, but it skips the years of deliberate work that precede it.

What I have observed is that the investors who build genuine passive income streams treat it like a second job in the early years. They research asset quality carefully, they reinvest distributions rather than spending them, and they review their portfolios at least twice a year. The "passive" part only kicks in once the foundation is solid.

The other thing I would push back on is the obsession with yield. A 9% yield sounds compelling until you realise the underlying asset is deteriorating. I have seen investors lock into high-yield REITs or dividend stocks that looked attractive on paper but were distributing capital rather than genuine earnings. Payout ratios and dividend growth history tell you far more than the headline number.

For Australians specifically, the franking credit system is genuinely underutilised. Many investors in the 25–45 age bracket do not realise that franking credits can result in tax refunds, not just offsets. That is a structural advantage that does not exist in most other countries, and it makes Australian dividend investing particularly attractive for self-directed investors.

The realistic path to meaningful passive income in Australia is patient, methodical, and grounded in real numbers. It is not fast, but it is achievable with the right structure and consistent effort over time.

— Jonathan

How Alphaiq helps you model your passive income position

Building a passive income portfolio is straightforward in theory. Knowing exactly where you stand, what your after-tax income will be, and how different scenarios affect your retirement position is where most self-directed investors get stuck.

Alphaiq is an Australian personal wealth intelligence platform built for investors who want real numbers, not rough estimates. The platform models your investment portfolio, superannuation, property, and retirement income in one place, with tax-aware scenario simulation covering franking credits, capital gains, and income projections. You can test different asset allocations, adjust your yield targets, and see the impact on your retirement date without paying for ongoing financial advice. Model your passive income position with Alphaiq and make decisions backed by your actual numbers.

FAQ

What is the simplest definition of passive income?

Passive income is earnings from assets or activities that do not require your active, ongoing participation. Common examples include rental income, dividends, and royalties.

Is passive income taxed differently in Australia?

Passive income is generally taxed at your marginal tax rate in Australia. However, dividends may carry franking credits that reduce your tax liability, and capital gains on assets held over 12 months attract a 50% discount.

How much capital do I need to generate meaningful passive income?

A diversified portfolio of approximately $1.1 million across dividend equities, bonds, and REITs can generate around $5,192 per month at a 5.7% yield. Smaller portfolios generate proportionally less, so starting early and reinvesting returns accelerates the timeline.

Does passive income require any ongoing work?

Passive income requires upfront capital or effort and ongoing maintenance. Managing tenants, rebalancing a portfolio, and meeting tax obligations are recurring tasks even for well-established income streams.

What are the best passive income sources for Australian investors?

The most reliable sources for Australian investors are ASX dividend stocks with franking credits, residential or commercial rental properties, REITs, and bonds. A blended approach across these asset classes produces the most consistent income over time.