TL;DR:

- Investment risk assessment integrates your financial circumstances, time horizon, and emotional comfort to guide suitable portfolio choices. Regular evaluations prevent mismatches between your risk capacity and tolerance, reducing reactive decisions and enhancing long-term wealth. Ongoing self-assessment aligned with your evolving situation ensures your investments remain genuinely appropriate for your goals.

Most investors spend considerable energy chasing returns, yet give surprisingly little thought to whether those returns are appropriate for their situation. The role of investment risk assessment is to close that gap. It brings together your financial circumstances, your time horizon, and your emotional relationship with uncertainty to create a picture that goes far beyond a simple risk label. When you understand that picture clearly, you stop making reactive decisions and start building a portfolio that genuinely reflects who you are as an investor and what you are trying to achieve.

Table of Contents

- Key takeaways

- What investment risk assessment actually involves

- Risk tolerance vs risk capacity: why the difference matters

- How to conduct your own risk evaluation

- Risk assessment and your portfolio

- Common myths that undermine risk assessment

- My perspective on why investors keep avoiding this

- Model your risk profile with Alphaiq

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Risk assessment is multidimensional | It covers time horizon, financial capacity, and psychological comfort, not just potential returns. |

| Tolerance and capacity are different | Emotional comfort with risk and your financial ability to absorb losses must both be measured separately. |

| Assessment is a recurring process | Your risk profile changes with life events, so annual reviews and quarterly check-ins in volatile markets are recommended. |

| Myths distort investor behaviour | Formulaic risk warnings often deter rather than inform; plain-language communication leads to better decisions. |

| Tools improve accuracy | Standardised questionnaires, financial reviews, and scenario modelling together produce a more complete risk profile. |

What investment risk assessment actually involves

The role of investment risk assessment is often misrepresented as a simple checkbox exercise. In practice, it is a systematic evaluation process that identifies and evaluates financial threats relative to your goals, across three core dimensions.

- Time horizon. How long until you need to access these funds? An investor with a 20-year runway can tolerate more volatility than someone who needs liquidity in three years.

- Financial capacity. What is your objective ability to absorb a loss without disrupting your lifestyle or financial goals? This includes income stability, debt levels, and existing assets.

- Psychological comfort. How do you actually feel when markets fall? Not how you think you would feel, but how you have responded in the past.

These three dimensions work together. A strong time horizon does not automatically mean you should hold a high-risk portfolio if your financial capacity is thin or your emotional response to volatility is severe. The financial risk assessment in investing must account for all three before any portfolio strategy is recommended or chosen.

Pro Tip: Do not rely on a single risk score from a brief questionnaire. Use it as a starting point, then stress-test it against your actual financial position and your real behaviour during past market downturns.

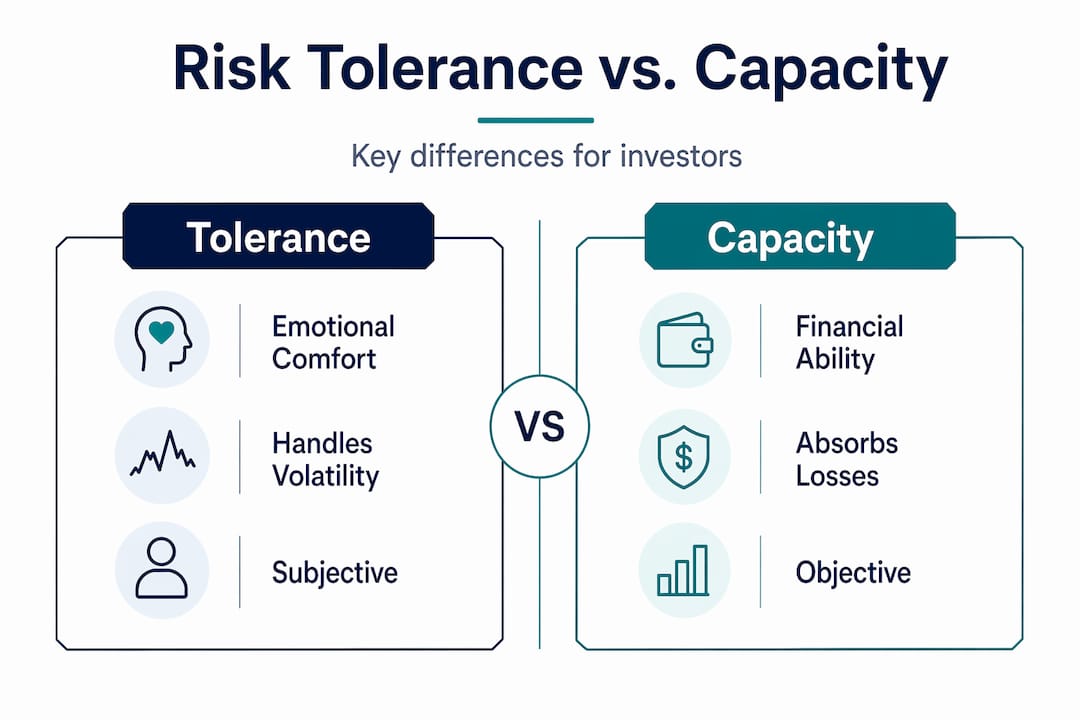

Risk tolerance vs risk capacity: why the difference matters

This is one of the most consequential distinctions in personal investing, and it is one that many investors get wrong.

Risk tolerance refers to your subjective, emotional comfort with volatility. It reflects how you feel when you watch your portfolio lose value. Some people remain calm during a 20% drawdown. Others find it difficult to sleep. Neither response is wrong, but both are relevant to how your portfolio should be structured.

Risk capacity is different. It is your objective ability to absorb losses without materially harming your financial security. Someone with stable employment, no consumer debt, and a six-month emergency fund has considerably more capacity than someone with variable income and significant mortgage obligations.

| Feature | Risk tolerance | Risk capacity |

|---|---|---|

| Nature | Subjective and emotional | Objective and financial |

| Measured by | Questionnaires and self-reflection | Financial data and ratios |

| Changes with | Emotional maturity, experience | Life events, income, debt levels |

| Impact when ignored | Emotional selling during downturns | Investing beyond financial means |

The mismatch between these two is where most investor errors occur. Someone who describes themselves as an "aggressive" investor may still be unsuitable for high-risk products if their liquidity is insufficient or their debt load is high. Equally, a cautious investor with strong financial capacity might be holding an unnecessarily conservative portfolio, limiting their long-term wealth.

A full suitability assessment should always go beyond a self-described risk label. It needs to include your time horizon, liquidity requirements, net worth, income reliability, and your genuine emotional response to loss.

Pro Tip: Ask yourself this: if your portfolio dropped 30% tomorrow and you could not touch it for two years, would that affect your ability to pay bills, service debts, or meet financial commitments? If yes, your risk capacity is lower than your tolerance, and your portfolio should reflect that.

How to conduct your own risk evaluation

Most investors benefit from treating the investment risk evaluation process as a structured exercise rather than an informal reflection. Research supports a four-week implementation framework that works well for self-directed investors.

-

Week 1: Financial assessment. Document your income, expenses, debts, existing assets, and liquidity position. Confirm you have a minimum of six to twelve months of living expenses in an accessible emergency fund before committing capital to higher-risk investments.

-

Week 2: Psychological assessment. Complete a standardised risk questionnaire from a reputable financial institution. Most are nine to ten questions and available at no cost. The result will categorise you as conservative, moderate, or aggressive. Treat this as one data point, not a verdict.

-

Week 3: Profile development. Combine your financial data with your questionnaire result to create a fuller picture. Look for mismatches. If your questionnaire says "aggressive" but your emergency fund is insufficient or you have high personal debt, your actual risk profile is more conservative than the label suggests.

-

Week 4: Implementation and monitoring. Review your current portfolio against your completed risk profile. Identify gaps and make adjustments. Set a schedule for ongoing reviews.

For ongoing management, annual full assessments are recommended as a baseline. In volatile markets or after significant life changes such as a job change, inheritance, or approaching retirement, quarterly reviews are appropriate. Your risk profile is not static, and your review schedule should account for that.

Risk assessment and your portfolio

Understanding your risk profile only delivers value when it is directly connected to how your portfolio is constructed and managed. This is where the role of risk analysis in finance becomes practical rather than theoretical.

Aligning your asset allocation to your risk profile prevents two of the most common investor mistakes. The first is emotional selling. When markets fall sharply, investors who are overexposed to risk relative to their actual profile tend to panic and sell at the worst time. The second is excessive conservatism. Investors who hold portfolios far below their risk capacity often accumulate wealth far more slowly than their situation warrants.

Strategies for investment risk assessment that connect directly to portfolio management include:

- Reviewing your asset allocation annually against your current risk profile, not the one you had when you first invested.

- Setting return expectations that are grounded in your risk level. A conservative portfolio should not be benchmarked against high-growth index returns.

- Treating portfolio rebalancing as a risk management activity, not just a performance optimisation exercise.

- Documenting your investment rationale at each review so you can distinguish between a considered strategy change and an emotional reaction.

The disciplined alignment of your portfolio with your long-term financial goals, rather than reacting to short-term market movements, is what separates investors who build wealth consistently from those who experience avoidable setbacks.

Regular portfolio reviews also serve as a natural trigger to revisit your risk assessment. Life changes affect both your financial capacity and your investment goals, so scheduled reviews should be built into your investment routine from the outset.

Common myths that undermine risk assessment

Even investors who understand the concept of risk assessment can be undermined by persistent misconceptions about how it works in practice.

"Formulaic risk warnings such as 'capital at risk' are widely misunderstood and often deter retail investors from participating in markets that are genuinely suitable for them. Balanced, plain-language communication about risk consistently produces better investor behaviour and engagement than compliance-style warnings."

The first myth is that a risk label is the same as a full suitability profile. It is not. Labelling yourself as "balanced" does not tell you whether your current portfolio is appropriate. It tells you approximately how much volatility you expect to tolerate. A complete picture requires the financial and liquidity context underneath that label.

The second myth is that your risk profile is fixed. Most investors find that their risk capacity changes significantly over time, even when their emotional tolerance for volatility remains similar. A pay rise, a property purchase, a redundancy, or the birth of a child all affect what you can afford to lose. Professional assessments also look for red flags such as insufficient liquidity or high debt that may not be visible from a questionnaire alone.

The third myth is that a questionnaire guarantees accurate self-knowledge. Research shows that most investors overestimate their risk tolerance, particularly when markets are performing well. When a downturn arrives, stated tolerance and actual behaviour often diverge sharply. Understanding this bias in advance allows you to build in safeguards, such as maintaining a larger cash buffer or committing in writing to a rebalancing plan before volatility arrives.

My perspective on why investors keep avoiding this

I have spent years watching investors who genuinely know better skip a thorough risk assessment. They do not skip it because they are uninformed. They skip it because honest self-reflection about risk means confronting the possibility of loss, and that is uncomfortable.

What I have learned is that the discomfort is actually useful data. If you sit down to complete a financial risk assessment and the exercise makes you anxious, that anxiety is telling you something about your real risk tolerance. Ignoring it does not make you a more disciplined investor. It makes you a less prepared one.

The most effective investors I have observed treat risk assessment as a living process. They revisit it after major life changes, after strong market runs, and after sharp downturns. They do not ask "what is my risk profile?" once and move on. They ask "is my profile still accurate given where I am today?" That question, asked consistently, is what keeps a portfolio genuinely suited to the person holding it.

The investment strategy you commit to is only as good as the self-knowledge behind it.

— Jonathan

Model your risk profile with Alphaiq

If you have worked through this article and realised your risk profile needs a closer look, Alphaiq gives you the tools to act on that insight without waiting for an adviser appointment.

The Alphaiq platform is built specifically for Australian self-directed investors who want to model their financial position across investments, superannuation, and property in one place. You can run scenario simulations to see how different asset allocations perform under varying market conditions, and stress-test your portfolio against your actual financial capacity. For investors factoring debt into their risk capacity, the debt recycling calculator helps you understand how to convert non-deductible debt into investment capacity. If your super balance is part of your risk equation, the retirement projection tool shows you how different contribution and investment strategies interact with your timeline and goals. Risk assessment becomes far more useful when it is grounded in your real numbers.

FAQ

What is investment risk assessment?

Investment risk assessment is the process of identifying and evaluating financial risks relative to your goals, time horizon, financial capacity, and emotional comfort with volatility. It helps you determine which investments are genuinely suitable for your situation.

How often should I reassess my investment risk profile?

Annual full assessments are recommended as a standard baseline, with quarterly reviews during volatile markets. You should also reassess after major life events such as a change in income, significant debt changes, or approaching retirement.

What is the difference between risk tolerance and risk capacity?

Risk tolerance is your emotional comfort with investment volatility, while risk capacity is your objective financial ability to absorb losses without harming your financial security. Both must be measured and aligned for a suitable investment strategy.

Can I trust a risk questionnaire to give an accurate profile?

Questionnaires provide a useful starting point but cannot guarantee that your stated tolerance matches your actual behaviour. Most investors overestimate their tolerance during strong market conditions, so questionnaire results should be cross-checked against your real financial position and past responses to market downturns.

Why does my risk profile change over time?

Your risk capacity shifts with life events such as job changes, debt levels, family circumstances, and proximity to retirement, even if your emotional tolerance for volatility stays broadly similar. Treating risk assessment as a recurring process rather than a one-off task keeps your portfolio genuinely suited to where you are now.