TL;DR:

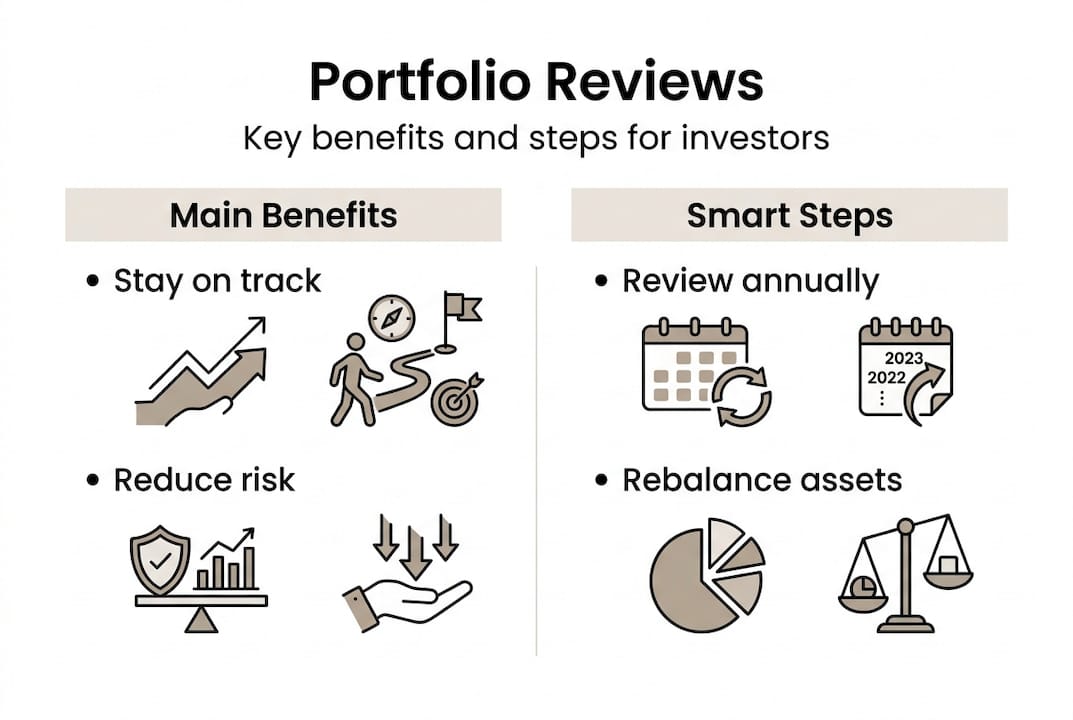

- Regular portfolio reviews help align investments with changing goals and market conditions.

- Without reviews, portfolios risk drift, increased concentration, and missed tax opportunities.

- Using tools and consistent assessments improves investment control and long-term outcomes.

Most investors put real effort into building a portfolio, then quietly assume it will look after itself. That assumption is one of the most common and costly mistakes in self-directed investing. Markets move, interest rates shift, and your personal goals evolve, all of which can push a once-solid portfolio off course without any obvious warning signs. A regular portfolio review is the practical tool that keeps your investments aligned with where you actually want to go. This article explains what a portfolio review involves, why it matters, and how to do one properly as an Australian investor.

Table of Contents

- What does it mean to review your portfolio?

- Why should you review your portfolio regularly?

- Common mistakes: What happens when investors don't review

- How to conduct an effective portfolio review in Australia

- A fresh take on portfolio reviews: It's about control, not just compliance

- Smarter tools for your next portfolio review

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Regular reviews prevent drift | Checking your portfolio annually keeps your investments on track with your goals. |

| Risk and goals change over time | Life events and market shifts mean your portfolio needs updating to fit your needs. |

| Simple tools give clarity | Online calculators and AI platforms make it easier for Australians to assess their investments. |

| Action beats inaction | Reviewing and adjusting your portfolio avoids costly mistakes from neglect. |

What does it mean to review your portfolio?

Having set the urgency for regular checks, let's clarify what a portfolio review actually involves.

A portfolio review is a structured process where you examine your investments against your goals, risk tolerance, and current market conditions. It is not a quick glance at your account balance. Done properly, it is a methodical assessment of whether your money is working the way you intended.

The key components of any thorough review include:

- Asset allocation: Are your holdings still split across asset classes (shares, property, cash, bonds) in the proportions you originally intended?

- Individual investment performance: Which holdings are performing well, which are lagging, and is underperformance temporary or structural?

- Risk exposure: Has your overall risk level changed due to market movements or new positions?

- Goal alignment: Do your investments still match your financial objectives, whether that is building a retirement nest egg, funding a property purchase, or generating passive income?

- Cash flows and tax position: Are you managing distributions, dividends, and capital gains efficiently?

- Major market changes: Have interest rate movements, inflation shifts, or sector trends altered the assumptions behind your original strategy?

As investment returns explained outlines, portfolio reviews should assess asset allocation, risk exposure, and investment performance as a baseline for every check. Without that baseline, you are reviewing numbers without context.

The most effective reviews are supported by consistent record-keeping. If you have not tracked changes in your goals alongside performance data, a review becomes guesswork rather than analysis.

Pro Tip: Each time you sit down to review your portfolio, write down any changes in your personal financial goals alongside your performance numbers. A portfolio that was right for you two years ago may need adjustment now, and your notes will show you exactly why.

Why should you review your portfolio regularly?

Now that you know what's involved, let's explore why these reviews can make or break your investment outcomes.

The core reason is simple: portfolios drift. Even if you make no changes, the market does. A share that grows strongly will become a larger slice of your portfolio over time, increasing your concentration in that asset without you ever making an active decision to do so. That drift can feel harmless until a correction arrives and your overexposed position takes a significant hit.

Risk levels change without you acting

Imagine you started with a balanced allocation of 60% growth assets and 40% defensive assets. After a strong equities run, that split might now sit at 75% growth and 25% defensive. Your risk exposure has increased substantially, yet you made no deliberate choice to take on more risk. Portfolio concentration risk is one of the most underestimated threats for self-directed investors, and periodic reviews are the primary tool for keeping it under control.

"Concentration risk builds silently. By the time most investors notice it, the damage is already priced in."

Your goals evolve over time

A 38-year-old building wealth aggressively has a very different risk profile to a 57-year-old approaching retirement. Optimising your wealth requires aligning investments with changing objectives at every stage of life. That alignment does not happen automatically. It requires deliberate, regular attention.

Here is a straightforward comparison of what regular reviewing versus a set-and-forget approach typically delivers:

| Factor | Annual review | Set and forget |

|---|---|---|

| Asset allocation accuracy | Maintained within target range | Drifts significantly over time |

| Risk management | Adjusted as life stage changes | Often increases without intent |

| Tax efficiency | Optimised through timely decisions | Opportunities frequently missed |

| Goal alignment | Regularly recalibrated | Gradually misaligned |

| Response to market change | Proactive and informed | Reactive or absent |

Market volatility amplifies the cost of inaction

Periods of significant market impacts on investments, such as rapid RBA rate changes or global equity corrections, can reshape the risk profile of your entire portfolio very quickly. Without a scheduled review, you may not realise how exposed you are until a specific event forces your hand. By then, your options for managing the damage are limited.

The benefits of regular reviews are cumulative. A single review might save you from a poor allocation. Five consistent annual reviews might meaningfully improve your long-term retirement income.

Common mistakes: What happens when investors don't review

Understanding the positives, it's just as important to face what goes wrong without reviews.

Neglecting reviews is rarely dramatic in the short term. The costs are gradual, quiet, and compounding. By the time they become visible, recovering ground takes considerably more effort than the review itself would have required.

Here are the four most common and costly consequences of skipping reviews:

-

Asset drift and unintended concentration. As mentioned earlier, weightings shift with market performance. Without a review to rebalance, one or two strong performers can dominate your portfolio, creating concentrated risk you never signed up for.

-

Goals misalignment. Life changes. A promotion, a redundancy, a new mortgage, children finishing university, or the approach of retirement all change what you need your portfolio to do. As wealth platforms in Australia highlight, failing to review can mean your portfolio no longer matches your objectives, which is a silent but serious problem.

-

Missed tax optimisation. Australian investors have access to meaningful tax advantages, including franking credits on Australian shares, the 50% capital gains tax discount for assets held over twelve months, and tax-effective superannuation contributions. Without a regular review, these opportunities are easily missed. Timing the sale of underperforming assets, for example, to offset capital gains elsewhere is a straightforward strategy that requires you to actually look at your portfolio.

-

Holding underperformers for too long. It is human nature to avoid realising a loss. But a stock or fund that has fundamentally changed in character, whether due to structural industry shifts or poor management, rarely recovers simply through patience. A review forces you to assess each holding on its current merits, not its historical promise. Combining that with a review of your property investment strategies gives you a complete picture of where your wealth actually stands.

Pro Tip: Set a recurring calendar reminder to review your portfolio at least once a year, ideally at the same time each year, such as just before the end of the financial year. Pair it with your tax preparation to make it a natural habit rather than an afterthought.

How to conduct an effective portfolio review in Australia

With the risks clear, let's focus on how you can take action.

A portfolio review does not require a financial planner or an expensive adviser. With the right process and the right tools, self-directed investors can conduct thorough and meaningful reviews independently. Here is a straightforward framework.

Step 1: Gather your data. Collect your current holdings list, most recent account statements, any records of contributions or withdrawals, and a written note of your current financial goals. Do not rely on memory for the goals part. Write them down. Be specific about timelines and dollar targets.

Step 2: Evaluate your asset allocation. Compare your current allocation against your target allocation. Most investors work with a target mix across Australian shares, international shares, property, fixed income, and cash. If any category has drifted by more than 5% from its target, it warrants attention.

Step 3: Assess individual investment performance. Benchmark each holding against a relevant index. An Australian large-cap share fund should be compared against the ASX 200 total return. An international equity allocation should be compared against a global benchmark like the MSCI World Index. Underperformance against a benchmark over three or more years is a meaningful signal.

Step 4: Consider tax implications before acting. Before selling anything, assess the tax impact. Are you within the twelve-month threshold for the CGT discount? Do you have losses elsewhere that can offset gains? This is where using retirement calculators and tax-modelling tools can genuinely clarify your position and required adjustments.

Step 5: Rebalance or redefine. Either rebalance your holdings back toward your targets, or update your targets if your circumstances have changed. Both are valid outcomes of a review. The key is intentionality.

Here is how traditional manual reviews compare to using modern digital tools:

| Approach | Time required | Depth of analysis | Tax awareness | Ease of scenario modelling |

|---|---|---|---|---|

| Manual spreadsheet review | High | Moderate | Limited | Difficult |

| Online calculators | Moderate | Good | Partial | Some scenarios |

| AI-driven wealth platforms | Low | High | Strong | Extensive |

Three tools that make portfolio reviews easier for Australian investors:

- Superannuation calculators: Help you model whether your current super balance and contributions are on track for your intended retirement income.

- Retirement income planners: Allow you to work backwards from your desired spending in retirement to understand required portfolio size and drawdown rates.

- Tax-aware modelling tools: Quantify the after-tax impact of rebalancing decisions, including the effect of franking credits, CGT events, and debt recycling on your overall position.

A fresh take on portfolio reviews: It's about control, not just compliance

After understanding the process, it's time for a truly practical perspective.

Here is something most financial content will not say plainly: most portfolios fail from neglect, not from poor initial decisions. The investment thesis was sound. The fund selection was reasonable. The allocation made sense at the time. What went wrong was the absence of any ongoing engagement.

Passive investing is a legitimate strategy. Low-cost index funds outperform most actively managed alternatives over the long run. But passive investment strategy is not the same as passive investor behaviour. You can hold passive investments and still review your portfolio actively. In fact, that combination is arguably the most powerful approach available to a self-directed investor.

The cost of DIY investing is often framed purely in terms of fees saved versus advice costs. But there is a third category that rarely gets enough attention: the cost of inaction. Markets do not reward you for having a great strategy in 2021 if you haven't revisited it since. Inflation, rate changes, super legislation, and personal circumstances all alter the playing field continuously.

We have observed that investors who treat reviews as a form of financial control, rather than an annual chore, make better decisions. They are not reacting to noise. They are checking in with purpose, confirming what is working, and adjusting what isn't. That mindset shift is significant.

"Smart investors treat the review process as an advantage, not an obligation."

Real success in self-directed investing is not about waiting for perfect conditions. It is about building a practice of regular, informed engagement with your money. Every time you review your portfolio with genuine intent, you take back control from the forces (markets, inflation, legislative change) that would otherwise shape your financial outcome for you.

Smarter tools for your next portfolio review

If this article has made one thing clear, it is that regular, structured portfolio reviews are the cornerstone of effective self-directed investing. The next step is making that process as straightforward and insightful as possible.

The AlphaIQ platform is built specifically for Australian investors who want to take control of their financial position without the cost of ongoing advice. From the superannuation calculator that models your retirement readiness, to the debt recycling calculator that helps you understand the tax-efficient use of equity, AlphaIQ brings together the tools you need for a genuinely informed portfolio review. Whether you are reviewing for the first time or looking to sharpen an already disciplined process, AlphaIQ gives you clarity, grounded in real numbers and tailored to Australian tax and super rules.

Frequently asked questions

How often should I review my investment portfolio?

Most experts suggest reviewing your portfolio at least once a year, or whenever your financial situation or markets change significantly. Periodic reviews help control concentration risk and keep your allocation on track.

What is the main goal of a portfolio review?

A portfolio review checks that your investments match your goals, risk tolerance, and current market conditions. As outlined when assessing investment performance, it should cover asset allocation, risk exposure, and individual returns.

What tools can help with portfolio reviews in Australia?

Australian investors use superannuation calculators, online platforms, and retirement planning tools for more informed reviews. Retirement tools can clarify your goals and highlight the adjustments needed to stay on track.

Is it risky to leave my portfolio on autopilot?

Neglecting reviews raises real risks, including misalignment with goals, unintended concentration, and missed tax opportunities. As noted across personal wealth platforms, failing to review regularly can mean your portfolio gradually drifts away from what you actually need it to do.