TL;DR:

- Most Australians view investment risk as unpredictable weather rather than a layered concept involving uncertainty and outcome variability. Professional investors measure and manage risk through documented strategies, considering factors like diversification, asset allocation, and maximum tolerable losses. Focusing solely on volatility overlooks extreme downside risks, making disciplined long-term behavior and clear planning essential for successful investing.

Most Australians think about investment risk the way they think about bad weather: something unpredictable that might ruin a good day. But reducing risk to "the chance you lose money" is one of the most costly misunderstandings in personal finance. Risk is layered, nuanced, and deeply connected to every decision you make about your portfolio, your super, your property, and your retirement timeline. This guide breaks down what investment risk actually means, how professional investors and regulators treat it, and what practical steps you can take to manage it with confidence and clarity.

Table of Contents

- What investment risk really means

- How professionals and the ATO define and manage risk

- Beyond volatility: Why 'risk' is more than just big swings

- Practical tools for managing your portfolio risk

- A practical perspective: What most guides miss about investment risk

- Take your next confident step with AlphaIQ

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Risk is multi-dimensional | Investment risk involves more than just market swings—it’s about all sources of uncertainty, including rare catastrophic events. |

| Professional risk frameworks work | Applying diversification, written strategies, and regular reviews lets individuals manage risk like top investors. |

| Volatility isn’t the full story | Assets can seem safe yet produce large losses—so go beyond volatility when analysing your portfolio. |

| Behaviour beats theory | Sticking to a plan and managing your reactions is often more important than complex calculations. |

| Tools can empower action | Using smart calculators and disciplined approaches helps Australians make better, less risky decisions. |

What investment risk really means

The simple version of risk goes like this: markets go up, markets go down, and if you're unlucky, you lose money. That framing isn't wrong, but it's dangerously incomplete. Understanding why manage investment risk starts with recognising that risk is really about uncertainty and the variability of outcomes, not just the possibility of a negative result.

Consider the difference between two investments. One earns 7% per year, reliably, for a decade. The other swings between gaining 25% and losing 15%, averaging out to the same 7%. Statistically, the returns match. But the second investment could wipe out years of progress at exactly the wrong moment, say, right before you retire. That variability is the essence of risk.

"All investments carry risk; higher potential return usually means greater risk, including the potential for loss and portfolio value variability." Macquarie Asset Management

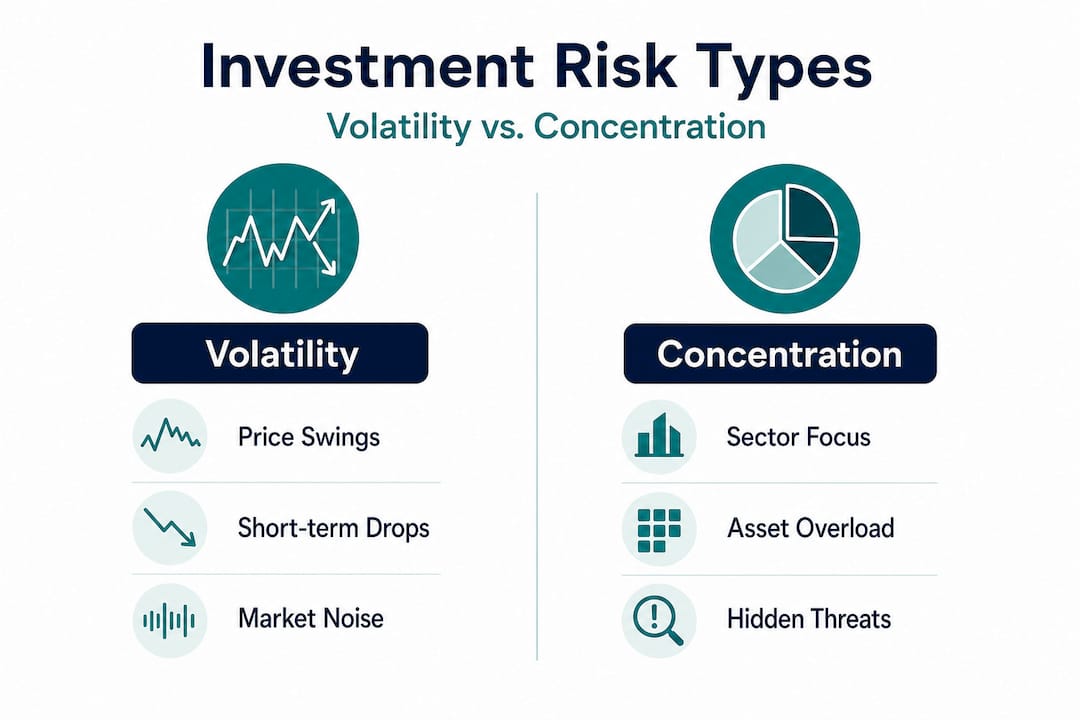

The types of risk you'll encounter in a typical Australian portfolio include:

- Market risk: The risk that broad economic or market conditions pull down your asset values, even when nothing is wrong with your specific investments.

- Liquidity risk: The risk that you cannot sell an asset quickly without taking a large price cut. Australian direct property is a classic example.

- Concentration risk: Holding too much in a single company, sector, or asset class. Many Australians unknowingly run concentrated portfolios through a mix of direct property, bank shares, and a super fund heavily weighted to Australian equities.

- Behavioural risk: Perhaps the most underestimated. This is the risk that you make a poor decision under pressure, such as selling during a downturn or chasing a recent winner.

Risk shows up in portfolios in ways that aren't always dramatic. It might be a sharp 20% drop in a single quarter. It might be years of flat returns while inflation quietly erodes your purchasing power. Or it might be missing a major rally because you moved to cash too early. All of these outcomes represent risk materialising, even when no single catastrophic event occurred.

How professionals and the ATO define and manage risk

Experienced investors and major institutions don't treat risk as a gut feeling. They document it, measure it, and build strategies around managing it deliberately. The Australian Tax Office takes a similar approach, particularly for self-managed super funds.

"The ATO expects SMSF trustees to have a written investment strategy that considers risk, diversification, and the dangers of concentration or leverage."

This isn't just red tape. A documented strategy forces you to confront your assumptions. What return do you actually need? How much loss can you absorb without changing your retirement plans? What mix of assets reflects your goals and timeline? These are the questions professionals ask every time they construct or review a portfolio.

Below is a practical framework that mirrors how institutional investors think about risk assessment.

| Risk consideration | Questions to ask yourself | Example |

|---|---|---|

| Return target | What annual return do I need to meet my goals? | 6% p.a. to fund retirement at 65 |

| Risk tolerance | How much loss can I absorb in a bad year? | Maximum 15% portfolio drawdown |

| Diversification | Am I spread across assets, sectors, and geographies? | Mix of Aus equities, international, bonds, property |

| Concentration | Is any single holding more than 20% of my portfolio? | Check direct property as a percentage of net worth |

| Liquidity | Can I access funds if I need them within 30 days? | Cash and liquid assets for short-term needs |

| Leverage | Am I borrowing to invest, and what's my serviceability buffer? | LVR on investment property plus interest rate buffer |

Looking at investment strategy examples used by other Australians can show you how people at different life stages weigh these considerations differently. A 40-year-old might accept higher equity exposure, while someone two years from retirement needs a tighter drawdown limit.

For property investment tips, the liquidity consideration becomes critical. Property can deliver strong long-term returns but carries significant liquidity risk, particularly if you need to rebalance during a downturn.

Pro Tip: Even if you don't have an SMSF, write down your investment strategy. One page is enough. Include your return goal, the maximum loss you can tolerate, your asset mix, and how often you'll review it. The discipline alone is worth more than most tools.

Beyond volatility: Why 'risk' is more than just big swings

Volatility, which is the statistical measure of how much an investment's price moves up and down, is the most commonly cited risk measure. It has genuine value. But relying on it alone gives you an incomplete picture, sometimes a dangerously flattering one.

Here's the problem. Volatility treats upward and downward swings equally. An investment that frequently jumps 10% looks the same to volatility as one that frequently drops 10%, but they feel very different to your portfolio and your retirement timeline. What volatility misses are the shape of those swings and the likelihood of extreme outcomes.

Two more useful concepts come from actuarial science:

- Skewness: If an investment has negative skewness, it means it experiences more large losses than large gains, even if the average looks fine. Your returns are not symmetrically distributed around the average.

- Kurtosis: High kurtosis means rare but extreme events happen more often than a normal statistical distribution would predict. These are the "fat tail" events that wipe out years of gains in weeks.

Australian property trusts are a useful example here. On paper, many have delivered consistent positive average returns over time. But the Actuaries Institute research found that "property trusts can exhibit negative skewness and positive kurtosis, meaning large negative outcomes can occur, even if average returns look solid." The Global Financial Crisis was exactly this kind of event for listed property trusts. Average returns looked acceptable leading up to it, but the distribution of outcomes was hiding extreme downside potential.

| Risk measure | What it tells you | What it misses |

|---|---|---|

| Volatility | Size of typical price swings | Direction and extremity of outcomes |

| Skewness | Whether losses or gains dominate the distribution | Doesn't show average return level |

| Kurtosis | Likelihood of rare extreme outcomes | Normal market behaviour |

| Maximum drawdown | Worst peak-to-trough loss in history | Future scenarios not yet seen |

Understanding portfolio concentration risk is particularly relevant here. When your portfolio is concentrated in one sector, a fat-tail event in that sector hits you with no buffer. Spreading across genuinely different asset classes, not just across 10 Australian bank stocks, reduces your exposure to these asymmetric losses.

Thinking about asset allocation explained in these terms helps you build a portfolio designed to survive the unexpected, not just optimise for the expected.

Pro Tip: Pull up your portfolio holdings and ask: which of these look stable on average but could drop 40% in a crisis? Australian listed property and high-yield credit are the most common examples. They don't behave like bonds when you need safety most.

Practical tools for managing your portfolio risk

Understanding risk conceptually is useful. Acting on it is what protects your wealth. Here's a structured approach to putting risk management into practice, regardless of whether you're managing $200,000 or $2 million.

-

Set your return goal first. Work backwards from what you actually need. If you plan to retire at 65 with $60,000 per year in spending, and you have 15 years to get there, calculate the portfolio return required. This gives your risk tolerance a real anchor, not just an abstract comfort level.

-

Define your maximum acceptable loss. How much could your portfolio drop in a single year before it materially changes your plans? 10%? 20%? Write it down. This becomes your practical risk boundary when you're reviewing new investments or rebalancing.

-

Map your asset allocation against your risk boundary. Use historical data to estimate how your current mix would have performed during major downturns (the GFC, COVID, the 2022 rate shock). If the simulated loss exceeds your boundary, adjust the allocation.

-

Apply diversification deliberately, not decoratively. True diversification means assets that don't move together in a crisis. Australian equities and Australian property often correlate strongly during downturns. Adding international shares, infrastructure, or fixed income can smooth outcomes.

-

Review and rebalance at least annually. Markets drift. A portfolio that started at 60% equities can become 75% equities after a strong year, without you doing anything. Regular rebalancing keeps your risk level intentional.

-

Document your plan and stick to it during volatility. The asset allocation guide and your own written strategy are your best defence against panic-driven decisions.

The Future Fund, which manages Australia's sovereign wealth, uses exactly this kind of approach. Their risk management framework targets returns with "acceptable but not excessive" risk, using asset allocation and volatility targets rather than chasing maximum returns. Self-directed investors can apply the same logic at any scale.

Key insight: Managing risk for retirement means recognising that the goal isn't to eliminate risk but to take the right kinds of risk in the right proportions for your timeline and goals.

A practical perspective: What most guides miss about investment risk

Most risk frameworks focus on numbers: volatility percentages, Sharpe ratios, maximum drawdown figures. These tools matter, but they can create a false sense of control. In practice, the biggest investment risk most Australians face isn't a statistical measure at all. It's their own behaviour under pressure.

Warren Buffett's view on risk challenges the standard definition directly: risk may be misunderstood when reduced to a single volatility metric, because drawdowns can reflect opportunities rather than just dangers. The investor who sold Australian equities in March 2020, when markets dropped 36%, locked in a real loss. The one who held on, or better yet added to their portfolio, captured one of the fastest recoveries in market history.

Long-term investing research consistently shows that discipline and time in the market matter more than precise risk modelling. Compounding works when you let it. Behavioural disruption is what stops it.

The uncomfortable truth is this: a highly volatile portfolio held with discipline will often outperform a conservative portfolio traded reactively. Chasing "low risk" through constant adjustment is itself a form of high risk.

Thinking about wealth management best practices means combining technical risk tools with the behavioural discipline to follow through. The plan matters. Sticking to it matters more.

Our view at AlphaIQ is simple. Risk is real, it's layered, and it deserves proper attention. But the investor who understands their own strategy, their own boundaries, and their own tendency to react under pressure is already ahead of most. Numbers clarify. Discipline protects.

Take your next confident step with AlphaIQ

Managing investment risk with confidence requires more than reading about it. You need tools that let you model your actual position, test different scenarios, and see the real numbers behind your decisions.

AlphaIQ is built specifically for self-directed Australian investors who want to do exactly that. The AlphaIQ platform combines tax-aware financial modelling with scenario simulation, so you can see how your portfolio performs under different conditions, model super projections, assess concentration risk, and plan your retirement income without the cost of ongoing financial advice. You can start with the free superannuation calculator to model your super balance at retirement, or use the debt recycling calculator to understand how smart debt structuring could improve your after-tax returns. Real numbers. Real clarity. Your next confident step starts here.

Frequently asked questions

What is the biggest risk in most investment portfolios?

Concentration risk — holding too much in one asset, sector, or geography — is often the biggest hidden threat, because it leaves you without a buffer when that area underperforms.

How do I calculate my portfolio's risk?

Start with volatility and diversification across your holdings, then check for concentration and consider your maximum acceptable drawdown. The Future Fund's approach uses realised volatility targets alongside an "acceptable but not excessive" risk mandate as a practical benchmark.

Is higher return always worth taking more risk for?

Not necessarily. Higher potential returns come with greater risk, including more extreme losses and wider outcome variability, which may not suit your timeline or life stage.

What's the benefit of documenting my investment approach?

A written plan forces clarity on your risk preferences and return goals, and provides a rational anchor when markets are volatile. The ATO requires SMSF trustees to document their strategy including risk considerations, a discipline any investor can benefit from.