TL;DR:

- Most investors prioritize stock selection over asset allocation, which actually drives over 93% of portfolio performance.

- Understanding risk tolerance, investment horizon, and diversification is essential before constructing a well-balanced, resilient portfolio.

Most investors spend far more time researching individual stocks than they do deciding how to split their money across different asset classes. That's a problem, because the asset allocation step by step decisions you make about your portfolio structure matter far more than which specific shares you pick. The landmark Brinson study on asset allocation found that 93.6% of portfolio performance variance is determined by asset allocation, not stock selection or market timing. This guide walks you through the full process, from foundational principles to ongoing maintenance, in a way that is practical and directly relevant to Australian investors.

Table of Contents

- Key takeaways

- Foundational principles of asset allocation

- Step-by-step guide to building your allocation

- Common mistakes and how to avoid them

- Tracking effectiveness and adjusting over time

- My honest take on asset allocation

- How Alphaiq helps you take control

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Allocation drives returns | Asset allocation accounts for over 93% of portfolio performance variance, making it the most important decision you will make. |

| Risk tolerance comes first | Assess your risk profile and time horizon before selecting any asset class mix or fund. |

| Rebalance with contributions | Direct new super or investment contributions to underweight assets to avoid triggering capital gains tax. |

| Simple rules outperform complexity | Straightforward allocation rules beat complex optimisation models, especially in volatile or uncertain markets. |

| Review on a schedule | Set a calendar trigger at least annually to check whether your allocation still matches your goals and circumstances. |

Foundational principles of asset allocation

Understanding what asset allocation actually means, and why it matters, is the right place to start before you touch a single calculator or open a brokerage account.

What asset allocation is. Asset allocation is the process of dividing your investment portfolio across different asset classes, typically growth assets like Australian and international shares, and defensive assets like bonds, cash, and fixed interest. The goal is not to maximise returns in isolation. It is to construct a portfolio that balances expected return against the level of risk you are genuinely willing and able to accept.

This is where most investors go wrong. They focus on finding the next winning stock or calling the market's direction, when the research is clear that these activities explain almost none of the variation in long-term results. A solid asset allocation explained framework sets the foundation that all other decisions rest on.

Three concepts you need to understand before you start:

- Risk tolerance. This is your psychological and financial capacity to absorb losses without abandoning your strategy. It is not simply about how much volatility you can stomach emotionally. It also reflects your income stability, existing debts, and how much time you have to recover from a market downturn.

- Investment horizon. The number of years before you need to draw on your invested capital shapes everything. A 45-year-old with 20 years until retirement can accept far more short-term volatility than a 62-year-old with three years to go. Age-based allocation rules exist precisely for this reason.

- Diversification and correlation. Holding assets that do not move in the same direction at the same time reduces portfolio volatility without necessarily reducing return. Australian shares and Australian bonds, for example, often behave differently during market stress, which is why most allocation frameworks include both.

Tools to prepare before you start planning:

| Tool or resource | Purpose |

|---|---|

| Risk tolerance questionnaire | Identifies your psychological and financial risk capacity |

| Superannuation statement | Shows existing allocation inside your super fund |

| Investment account summary | Documents current holdings outside super |

| Net worth spreadsheet | Captures full picture including property, debts, and liquid assets |

| Portfolio tracking platform | Monitors allocation drift and performance over time |

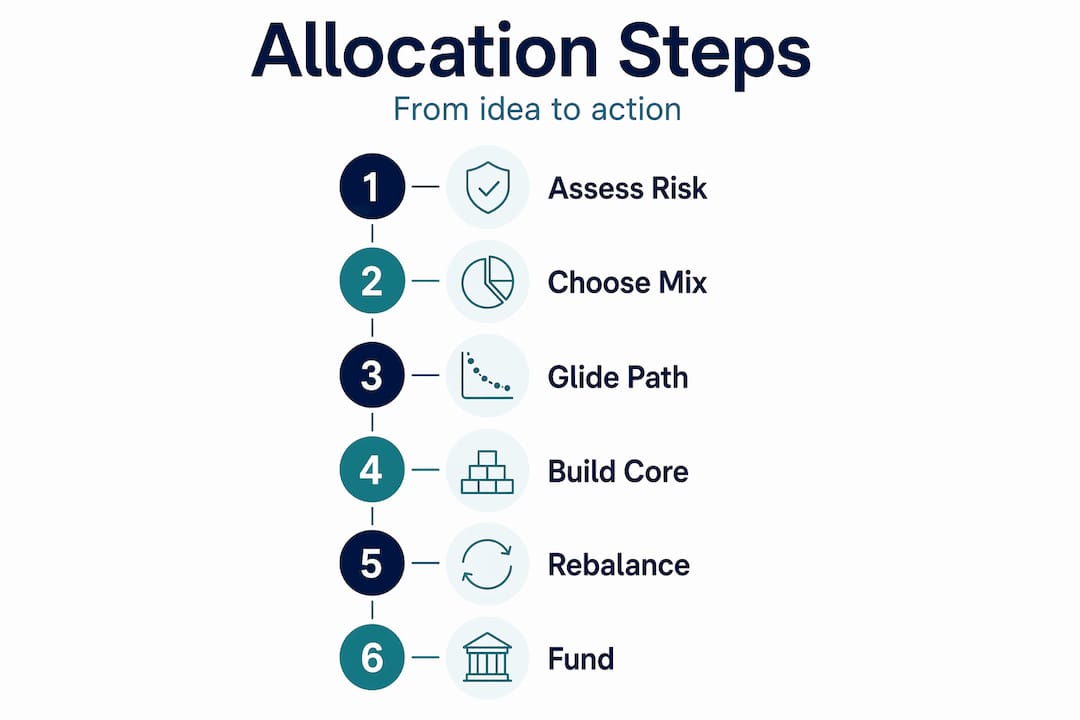

Step-by-step guide to building your allocation

This is where the stepwise asset investment process becomes concrete. Follow these steps in order. Skipping ahead tends to produce allocations that look good on paper but fall apart under real market conditions.

Step 1: Assess your risk tolerance and time horizon. Ask yourself three practical questions. First, how many years until you plan to access this money? Second, if your portfolio dropped 25% in a single year, what would you do? Third, what is your income security like over the next five years? Your honest answers to these questions should guide your risk profile classification, whether that is conservative, balanced, growth, or high growth.

Step 2: Select a target asset class mix. Once you know your risk profile, match it to a broad allocation framework. A balanced profile for a 50-year-old might sit at 60% growth assets and 40% defensive. A growth profile for a 42-year-old might be 80/20. These are starting points, not permanent prescriptions. The key is that your allocation should reflect your circumstances, not a generic template.

Step 3: Consider age-based glide paths. One of the most practical tools in modern investing is the target-date fund structure. These funds use glide paths to shift portfolio composition from aggressive to conservative as your retirement date approaches. You can replicate this logic manually by committing to review and nudge your allocation toward defensives every five years. It is a disciplined, automatic way to manage the risk reduction most investors forget to do.

Step 4: Build your portfolio using a core-satellite approach. The core of your portfolio (typically 70 to 80%) should sit in low-cost, broadly diversified index funds covering Australian shares, international shares, and bonds. Your satellite positions (20 to 30%) can reflect specific views, such as an overweight to Australian property securities or a small exposure to infrastructure. For most Australians, this means a combination of ASX-listed ETFs covering the ASX 200, a global index fund, and a bond fund. Keep costs in mind here. The true cost of ETFs includes tracking difference and securities lending, meaning some low-cost funds are even cheaper than their stated expense ratio suggests.

Pro Tip: Start with three funds maximum. One Australian share ETF, one global share ETF, and one bond or defensive ETF. Adding more funds rarely improves diversification and usually just creates complexity that makes rebalancing harder.

Step 5: Set your rebalancing triggers. The 5/25 rebalancing rule is a proven professional standard. Rebalance when a major asset class drifts more than 5 percentage points from its target, or when a smaller holding drifts by 25% in relative terms. For example, if your target is 40% international shares and it grows to 46%, that triggers a rebalance. This rule reduces unnecessary trading while keeping your risk profile intact.

Step 6: Plan how you will fund rebalancing. The most tax-efficient way to rebalance is to direct new contributions, whether into super or a brokerage account, toward the underweight asset classes rather than selling overweight ones. This avoids triggering capital gains tax and keeps your portfolio on target without the friction of selling.

Common mistakes and how to avoid them

Even investors who understand the theory of effective asset allocation make costly errors in practice. These are the most common ones, and how to sidestep them.

- Treating rebalancing as a performance play. Rebalancing is not about buying the asset you think will do best next. It is a risk management tool. You are selling what has grown beyond its target weight and buying what has fallen behind. That discipline is uncomfortable, but it is the entire point.

- Over-relying on optimisation models. Complex mean-variance optimisation and similar frameworks can look precise but perform poorly under uncertainty. The models are only as reliable as the assumptions behind them. Simpler, robust rules, like the 60/40 split or the core-satellite structure, have a strong track record precisely because they do not depend on fragile forecasts. A broader discussion of optimisation model limits in financial planning is worth reading if you are tempted by complex tools.

- Letting drift go unaddressed. Markets move. A portfolio that starts at 70/30 can become 80/20 after a strong equity run, dramatically increasing your risk exposure without you making a single active decision. Ignoring drift is one of the most common causes of investors experiencing far more volatility than they expected.

- Ignoring tax when rebalancing. Selling appreciated assets in a taxable account triggers capital gains tax. Many investors forget that directing new contributions to underweight assets achieves the same rebalancing outcome without realising a taxable gain.

Pro Tip: Set a calendar reminder every six months to check your allocation against your targets. Do not wait for a market event to prompt the review. Discipline comes from routine, not reaction.

Tracking effectiveness and adjusting over time

Building your allocation is the first act. Maintaining it is the ongoing work that actually determines your long-term results.

![]()

Portfolio tracking platforms let you compare your current allocation against your target at a glance. What you are looking for is simple: has any major asset class drifted enough to breach your rebalancing thresholds? If not, no action is required. If it has, apply the 5/25 rule and adjust using new contributions where possible.

Understanding your portfolio's risk-adjusted return adds another layer of insight. The Sharpe ratio measures how much return you are generating per unit of risk taken. A higher Sharpe ratio means you are being compensated more efficiently for the volatility you are accepting. You do not need to calculate this manually. Most modern portfolio tracking tools report it automatically.

Beyond the routine checks, set a strategic review at least once a year where you step back and ask whether your allocation still fits your life circumstances. The right allocation for a 48-year-old with a stable salary and a 17-year horizon is not the right allocation for that same person at 55 with a target retirement date three years away. Investment strategies for pre-retirees in Australia often require a deliberate shift in thinking at precisely this stage.

| Rebalancing frequency | Approach | Best suited to |

|---|---|---|

| Threshold-based (5/25 rule) | Rebalance only when drift breaches set limits | Most investors with low-cost index portfolios |

| Calendar-based (annual) | Rebalance on a fixed date each year | Simpler portfolios or super fund members |

| Contribution-directed | Apply new funds to underweight assets | Investors with regular contributions and tax sensitivity |

| Target-date fund (automatic) | Fund rebalances internally to a glide path | Hands-off investors comfortable with a single fund structure |

Target-date funds come in two forms worth knowing: "To" versus "Through" structures. A "To" fund reaches its conservative allocation exactly at your nominated retirement date. A "Through" fund continues adjusting past that date, which suits investors who plan to draw down over a long retirement. Understanding which type you hold matters, because the risk profile in your early retirement years can differ significantly between the two.

My honest take on asset allocation

What I have observed over years of working with investment frameworks is that most people start the process backwards. They buy the shares first and think about allocation second. By then, their portfolio reflects market conditions at the time of purchase more than it reflects their own goals and risk tolerance.

The uncomfortable truth I have come to is that perfect timing and optimal portfolios are illusions. I have seen complex allocation models fail in volatile conditions precisely because they were built on assumptions that only hold in calm markets. Simple rules outperform complex models when conditions get uncertain, and uncertain conditions are the only ones that actually test your portfolio.

What I have found actually works is this: clarity on your real risk tolerance, a straightforward split across three or four asset classes, and the discipline to rebalance using new contributions rather than selling. That last point alone saves most investors from unnecessary tax drag. And using target-date fund structures, or manually replicating their glide path logic, removes a lot of the behavioural errors that cost investors far more than any suboptimal asset split ever would.

Consistency beats precision every time.

— Jonathan

How Alphaiq helps you take control

If you have worked through this guide and want to model your actual numbers rather than work from generic templates, Alphaiq is built precisely for that. The Alphaiq AI Wealth Intelligence Platform gives Australian self-directed investors the tools to model their investment position across shares, super, property, and retirement income in one place, with tax-aware scenario modelling built in.

You can use Alphaiq to test different allocation splits, run capital gains scenarios before rebalancing, and see how changes to your super contributions affect your retirement projection. The super projection calculator is particularly useful for aligning your allocation decisions with a concrete retirement income target, rather than making allocation choices in isolation. Whether you are at the portfolio-building stage or reviewing an existing structure, Alphaiq gives you the clarity to act with confidence.

FAQ

What is asset allocation and why does it matter?

Asset allocation is how you divide your investment portfolio across different asset classes such as shares, bonds, and cash. Research shows it accounts for over 93% of performance variance, making it the most important structural decision in any investment strategy.

How do I know what asset allocation suits my age?

Your allocation should reflect your investment horizon, risk tolerance, and income security rather than your age alone. Common rules of thumb, such as holding more in defensive assets as you near retirement, are a useful starting point, but your personal circumstances should guide the final mix.

What is the 5/25 rebalancing rule?

The 5/25 rule means you rebalance when a major asset class drifts more than 5 percentage points from its target, or when a smaller holding drifts 25% in relative terms. It reduces unnecessary trading while keeping your portfolio's risk profile on track.

Should I use a target-date fund or build my own portfolio?

Target-date funds automate the glide path and reduce behavioural errors, making them well suited to hands-off investors. Building your own allocation gives more control over costs and tax outcomes, but requires the discipline to rebalance consistently.

How can I rebalance without triggering capital gains tax?

Direct new contributions toward your underweight asset classes instead of selling overweight ones. This contribution-based rebalancing approach keeps your allocation on target without realising taxable gains.