TL;DR:

- Independent financial advice offers unbiased guidance from the whole market, ensuring recommendations align with clients' interests. Restricted advisers operate within limited product sets and face higher conflict risks, impacting advice quality. Assessing a true independent adviser involves reviewing conflict management processes and product access, especially during major financial life events.

Independent financial advice is defined as unbiased, whole-of-market guidance where your adviser has no structural obligation to recommend any particular product or provider. For Australians aged 30–60 facing decisions about superannuation, investments, and retirement income, the stakes of getting advice wrong are high. Understanding why seek independent advice matters comes down to one core principle: your adviser's interests must align with yours, not with a product panel or a licensee's revenue targets. Regulatory bodies like ASIC, the CFP Board, and MoneyHelper all point to conflict management as the defining feature of genuine independence.

What is independent financial advice and how does it differ from restricted advice?

Independent financial advisers can recommend any product from across the whole market, while restricted advisers work within a limited product set tied to specific providers or platforms. That distinction matters enormously when you are trying to find the best superannuation fund, investment structure, or insurance product for your specific situation.

The difference is not primarily about fees. Many restricted advisers charge similar fees to independent ones. The real difference lies in the scope of what they can consider when building your financial plan.

| Feature | Independent adviser | Restricted adviser |

|---|---|---|

| Product access | Whole of market | Limited panel or provider |

| Conflict of interest | Minimised by structure | Higher structural risk |

| Regulatory standard | Must manage all conflicts | Disclosure may suffice |

| Recommendation scope | Any suitable product | Products within approved list |

Key distinctions to understand:

- Market access. An independent adviser can compare products across the entire market, not just those on an approved list.

- Conflict structure. Restricted advisers may receive volume bonuses, platform rebates, or other incentives tied to specific products.

- Documentation. Independent advisers must document why a recommendation was made and what alternatives were considered.

- Suitability. Advice quality depends on how recommendations are generated and documented, not just on the independence label.

The independence label alone does not guarantee quality. What matters is the process behind the recommendation and the controls in place to manage conflicts.

Why is independent advice important for investors aged 30–60?

The period between 30 and 60 is when financial decisions carry the most long-term weight. Superannuation contribution strategies, debt recycling, property investment, and retirement income planning all interact with each other in ways that generic or restricted advice often misses.

Holistic planning by CFP® professionals improves clients' preparedness, reduces anxiety, and motivates goal attainment. That outcome is not accidental. It reflects what happens when an adviser can consider your full financial picture without being constrained by a product panel.

Life transitions are where the value of unbiased guidance becomes most visible:

- Changing jobs. Rolling over superannuation, reassessing insurance cover, and adjusting contribution rates all require whole-of-market thinking.

- Buying property. Structuring debt correctly from the start affects capital gains tax and borrowing capacity for decades.

- Approaching preservation age. Decisions about transition-to-retirement income streams and drawdown sequencing have permanent tax consequences.

- Divorce or business exit. Complex personal financial events produce the highest payoff from independent advice because the stakes and the variables are both elevated.

ASIC's December 2025 update to RG 181 requires financial firms to map conflicts across remuneration and relationships, and review decisions to mitigate bias risk. This regulatory shift means that the bar for what counts as genuine independence is rising. Advisers who rely on disclosure alone no longer meet the standard.

Pro Tip: Ask your adviser to show you their conflict register before your first meeting. A genuine independent adviser will have one and will be comfortable sharing it.

How do you identify genuinely independent financial advice?

Identifying a truly independent adviser requires more than checking their licence. ASIC-licensed advisers operating under an Australian Financial Services Licence (AFSL) must comply with best interests obligations, but the quality of conflict management varies significantly between firms.

Follow these steps to assess genuine independence:

- Ask about product access. Request a list of the platforms and products your adviser can recommend. If the list is short or tied to one institution, the advice is restricted regardless of how it is marketed.

- Request the conflict register. ASIC expects tailored conflict controls including on remuneration. A credible adviser will have a documented framework, not just a disclosure statement.

- Ask how alternatives are considered. The critical question is not what they recommend but how they rule out alternatives. Ask them to walk you through their research process.

- Review the Statement of Advice. A genuine independent adviser's Statement of Advice will document the alternatives considered and the reasons for rejection, not just the recommended product.

- Check remuneration structure. Fee-for-service advisers who charge a flat fee or hourly rate have fewer structural conflicts than those who earn commissions or asset-based fees tied to product placement.

Warning signs of restricted or biased advice include: a very short list of recommended platforms, vague answers about how alternatives are assessed, and Statements of Advice that lack documented rationale for rejecting other options.

Pro Tip: Cross-check your adviser's registration on the ASIC Financial Advisers Register at moneysmart.gov.au. It shows their licence, qualifications, and any disciplinary history.

What are the measurable benefits of independent advice?

The benefits of independent advice are not just theoretical. Research consistently shows that advised households accumulate more wealth and make better financial decisions over time.

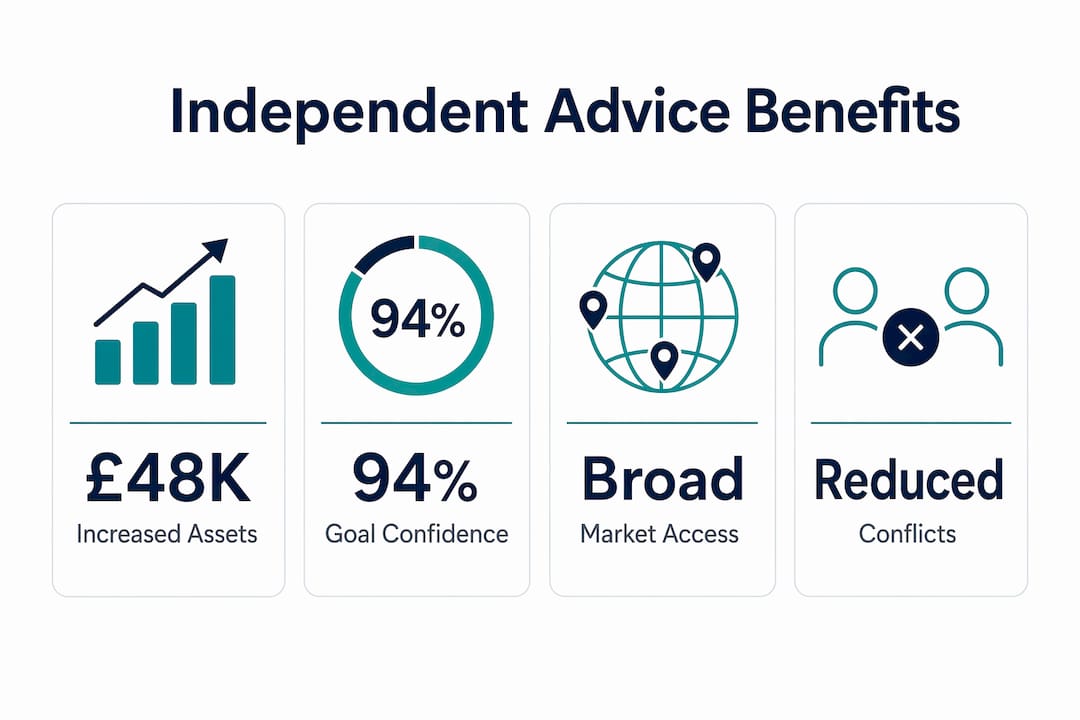

Professional financial advice recipients increased their pension and financial assets by nearly £48,000 over 10 years compared to those without advice. That figure represents the compounding effect of better product selection, tax efficiency, and contribution timing.

| Outcome area | Advised households | Unadvised households |

|---|---|---|

| Confidence in achieving goals | 94% | 81% |

| Emergency fund in place | Higher rate | Lower rate |

| Will or estate plan completed | Higher rate | Lower rate |

| Retirement income plan documented | Higher rate | Lower rate |

The CFP Board research shows 94% of households advised by CFP® professionals feel confident in achieving their financial goals, versus 81% of unadvised households. That 13-percentage-point gap reflects the practical difference between having a plan and hoping things work out.

For Australians specifically, the value of integrated advice on superannuation, investments, tax, and cashflow is highest when those elements are treated together. Tailored advice reduces the risk of recommendations that are technically correct but contextually wrong for your situation. A contribution strategy that works perfectly for a 45-year-old employee may be entirely wrong for a 45-year-old business owner with variable income.

"The biggest risk in financial advice is not misinformation. It is guidance that is right in theory but wrong for your specific context." — Wealthtender

The FCA's Consumer Duty framework reinforces this point by requiring firms to deliver fair value and avoid foreseeable harm. Independent advisers are structurally better placed to meet that standard because they are not constrained by product panels that may not serve your interests.

For Australians approaching retirement, the investment options for pre-retirees that deliver the best outcomes are rarely the default ones. Independent advice gives you access to the full range of choices.

Key takeaways

Independent advice delivers measurable financial outcomes because it combines whole-of-market access, documented conflict management, and personalised planning that restricted advice structurally cannot match.

| Point | Details |

|---|---|

| Independence means market access | Independent advisers can recommend any product, not just those on an approved panel. |

| Conflict management is the standard | ASIC's updated RG 181 requires firms to map and mitigate conflicts beyond simple disclosure. |

| Advised households accumulate more | Research shows advised households gained nearly £48,000 more in assets over 10 years. |

| Life transitions demand unbiased guidance | Retirement, divorce, and business exit are when independent advice delivers the highest value. |

| Process matters more than the label | Assess how recommendations are generated and documented, not just whether the adviser claims independence. |

The uncomfortable truth about "independent" advice in Australia

Most Australians assume that paying for advice automatically means getting unbiased guidance. That assumption is wrong, and it costs people real money.

I have seen situations where an adviser operating under a major institution's licence recommends products that happen to sit on that institution's approved platform. The advice is technically compliant. The conflicts are disclosed. But the client never knows what they did not get access to. That is not independence. It is disclosure dressed up as objectivity.

The distinction that matters is not the label on the door. It is the process behind the recommendation. When I look at whether an adviser is genuinely independent, I ask one question: can you show me the alternatives you considered and why you ruled them out? An adviser who cannot answer that question clearly has not done the work.

For Australians aged 30–60, the financial decisions you make in the next decade will shape your retirement for 30 years. Getting advice that is right in theory but wrong for your specific tax position, your super balance, and your income structure is not good enough. The cost of financial advice versus DIY investing is a real consideration, but the cost of structurally biased advice is far higher and far harder to see until it is too late.

My view is that Australians should treat adviser selection with the same rigour they apply to any major financial decision. Check the conflict register. Review the Statement of Advice carefully. Ask hard questions about product access. The advisers who welcome those questions are the ones worth trusting.

— Jonathan

How Alphaiq supports your independent financial decisions

Making confident financial decisions requires more than a single advice meeting. You need to model scenarios, test assumptions, and understand how your super, investments, and tax position interact over time.

Alphaiq is an Australian wealth intelligence platform built for self-directed investors aged 35–65. It gives you tax-aware financial modelling across superannuation, property, investments, and retirement income, all in one place. Use the Alphaiq super calculator to project your superannuation outcomes under different contribution strategies, or model your full retirement income picture on the Alphaiq platform. Alphaiq does not replace independent financial advice. It gives you the numbers you need to walk into any advice conversation with clarity and confidence.

FAQ

What is independent financial advice?

Independent financial advice is guidance from an adviser who can recommend products from across the whole market without being constrained by a product panel or provider relationship. The defining feature is the absence of structural conflicts of interest.

When should you seek independent advice?

Independent advice is most valuable during complex life transitions such as approaching retirement, changing jobs, buying property, or exiting a business. These events involve multiple financial variables that interact in ways generic advice often misses.

How do you check if an adviser is truly independent?

Ask to see their conflict register, the full list of products they can recommend, and a sample Statement of Advice showing how alternatives were considered. You can also verify their licence and history on the ASIC Financial Advisers Register at moneysmart.gov.au.

Does independent advice cost more than restricted advice?

Not necessarily. Independence relates to market access and conflict management, not to fee structure. Fee-for-service advisers who charge a flat or hourly rate exist across both independent and restricted categories.

What does ASIC require from financial advisers on conflicts of interest?

ASIC's updated RG 181 requires Australian Financial Services Licence holders to map conflicts across remuneration and relationships, and to implement tailored controls that go beyond simple disclosure to actively mitigate bias risk.