TL;DR:

- Retirees benefit from blending multiple income sources like super, pension, and assets for resilience.

- Adequate super savings for a comfortable retirement are around 630,000 dollars for singles and 730,000 for couples.

- Building a flexible income system and regular review strategies leads to more secure and adaptable retirement income.

Most Australians approach retirement with a single financial anchor in mind, whether that's superannuation, the Age Pension, or a property portfolio. Yet relying on just one source leaves your retirement income exposed to market shifts, policy changes, and unexpected personal circumstances. The most financially secure retirees are those who blend multiple income streams, creating a system that is flexible, resilient, and tailored to how they actually want to live. This guide breaks down the core income categories available in Australia, explains what "enough" really looks like in dollar terms, and outlines practical strategies for building a retirement income mix that genuinely works for you.

Table of Contents

- Decoding the main retirement income streams

- How much is enough? Understanding retirement adequacy

- Optimising and diversifying your income mix

- Navigating the nuances: flexibility, trade-offs, and expert insights

- The myth of one perfect retirement formula

- Transform your strategy with smarter retirement tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Blend income streams | Combining superannuation, Age Pension, and non-super assets can create a more reliable retirement income. |

| Flexibility matters | Account-based pensions allow for adjustments as your lifestyle and needs change. |

| Use benchmarks wisely | ASFA targets are helpful but not set in stone—many retirees thrive with less if they optimise their resources. |

| Review your plan regularly | Adapt your income strategy as circumstances, rules, and opportunities shift. |

Decoding the main retirement income streams

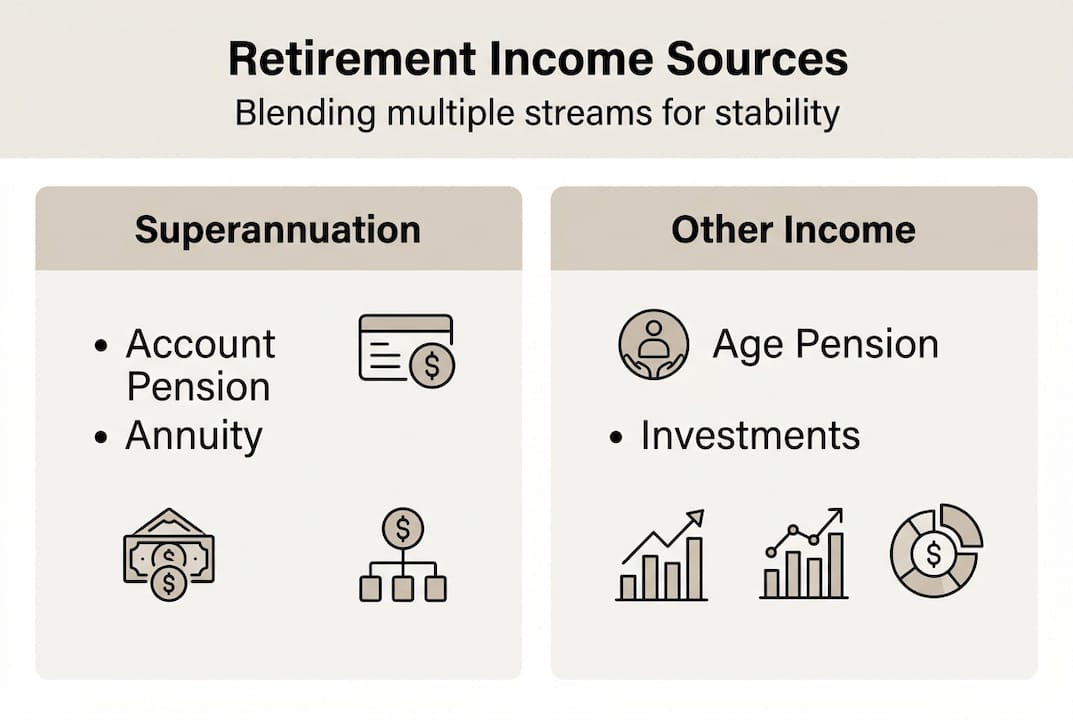

Understanding where your retirement income can come from is the essential first step. In Australia, retirement income sources broadly fall into three categories: the Age Pension, superannuation income streams, and non-super assets such as shares, property, and part-time work. Each plays a distinct role, and each comes with its own rules, tax treatment, and risk profile.

The Age Pension functions as a foundational safety net. More than 50% of Australians aged 67 and over receive some form of Age Pension, whether full or part. Eligibility is means-tested, which means your super balance and other assets will affect how much you receive. The full Age Pension currently provides around $29,754 per year for a single person and $44,855 per year for a couple combined. Importantly, it adjusts with inflation, which gives it a stability that market-linked assets can't always match.

Superannuation income streams are the largest source of private retirement income for most Australians. Once you reach your preservation age (currently 60 for those born after 30 June 1964) and meet a condition of release, you can draw from your super in several ways. Account-based pensions allow flexible drawdowns, meaning you can adjust how much you take each year. Annuities convert a lump sum into guaranteed income payments, which can be fixed for a set number of years or for life. Lump sum withdrawals are also possible, though these require careful tax and cashflow planning. Understanding the difference between tax-free retirement income and taxable components within super can also make a significant difference to your net income.

Non-super assets are often underestimated as an income source. Rental income from investment property, dividends from a share portfolio, and income from part-time or casual work can all meaningfully supplement your super and pension income. These sources give you flexibility and, in some cases, continued engagement with work or investment that many retirees find personally rewarding.

Here is a comparison of the three main income categories:

| Income stream | Key feature | Main advantage | Key risk |

|---|---|---|---|

| Age Pension | Means-tested, indexed | Stable, inflation-linked | Reduced if assets/income rise |

| Account-based pension | Flexible drawdown from super | Tax-free from age 60 | Dependent on market performance |

| Annuity | Guaranteed income payments | Certainty and predictability | Less flexibility, lower returns |

| Shares and dividends | Market-linked income | Growth potential, franking credits | Market volatility |

| Rental property | Passive income from tenants | Inflation hedge, capital growth | Vacancies, maintenance costs |

| Part-time work | Earned income | Flexibility, social engagement | Physical and energy constraints |

If you're thinking about how much super you need to retire at 60, it's worth factoring in all of these streams rather than viewing super in isolation.

How much is enough? Understanding retirement adequacy

After mapping out the key income streams, the next question is: how much do you actually need to achieve your retirement goals?

The Association of Superannuation Funds of Australia (ASFA) provides the most widely used benchmarks in Australia. The ASFA Retirement Standard (December 2025 figures) sets the following annual income targets:

| Lifestyle | Singles | Couples |

|---|---|---|

| Comfortable | $54,840/yr | $77,375/yr |

| Modest | $35,000/yr | $51,000/yr |

To fund a comfortable retirement, ASFA estimates you need approximately $630,000 in super at age 67 if you're single, and $730,000 as a couple. For a modest retirement, the figures drop to around $110,000 for singles and $120,000 for couples, because the Age Pension covers a much larger proportion of spending at that level.

These figures assume a combination of investment returns from your super balance and a part Age Pension where applicable. They also assume you own your home outright, which is a significant factor. Renters in retirement typically need considerably more income to cover housing costs, something the standard benchmarks do not fully address.

Key insight: The ASFA figures are a useful starting point, but they represent average spending patterns. If you plan to travel extensively, support adult children, or maintain a particular lifestyle, your personal target may be meaningfully higher.

It's also worth understanding the assumptions baked into these benchmarks. They typically assume a real (after-inflation) investment return of around 6% per year on your super balance, a drawdown rate that exhausts your capital by age 92, and wage growth in line with historical averages. If returns are lower than expected or you live longer than average, the numbers shift.

Many Australians find themselves in a middle zone: too much super or assets to qualify for the full Age Pension, but not enough to feel truly secure on private income alone. This is sometimes called the "retirement income gap," and it's exactly where smart income layering becomes most valuable. You can use a superannuation calculator to model where you're likely to land, or start from your desired lifestyle spend and work backwards to understand your financial independence number.

The key lesson from the adequacy question is this: chasing a single number is less useful than building a system. A retiree with $500,000 in super, a paid-off home, a modest share portfolio generating $8,000 per year in franked dividends, and eligibility for a part Age Pension may well live more comfortably than someone with $700,000 in super and no other assets, particularly if they approach drawdown thoughtfully. Consider using retirement income planning steps to map your own position clearly.

Optimising and diversifying your income mix

Once you know your target, it's time to think strategically about how best to blend your income sources.

The concept of layering income streams is straightforward but powerful. Rather than drawing everything from one source, you deliberately combine income types that behave differently under different conditions. When markets fall, a guaranteed annuity or Age Pension keeps income flowing. When markets perform strongly, your account-based pension grows and can fund discretionary spending. Rental income from property tends to rise with inflation. Dividends from Australian shares often come with franking credits, which can reduce your tax bill or even result in a refund.

Here are five practical steps to begin optimising your income mix:

- Map your existing sources. List every potential income source you'll have in retirement: super balance, expected Age Pension entitlement, property, shares, any defined benefit pension, and likely part-time income. Assign a rough annual income figure to each.

- Identify gaps and risks. Look for single points of failure. If 80% of your income depends on your super balance performing well, you're exposed to sequence-of-returns risk (the danger that poor early returns permanently reduce your capital).

- Consider a "core and satellite" approach. Allocate a portion of your income to guaranteed or stable sources (the core), such as the Age Pension or an annuity. Use more flexible and growth-oriented sources (the satellite) to fund discretionary spending and manage inflation over time.

- Review Centrelink implications. Non-super income sources and assets are included in Centrelink's income and assets tests. A financial decision that increases your assets may reduce your Age Pension entitlement. This interaction requires careful modelling before you act.

- Revisit annually. Your income needs, health, and asset values will change. A strategy that works at 67 may need adjustment at 75. Build in a regular review, even if it's just an annual check of your drawdown rate and spending patterns.

Pro Tip: Account-based pensions offer considerable flexibility because you can adjust your drawdown each year. The government sets minimum annual drawdowns (ranging from 4% at age 65 to 14% at age 95+), but there is no maximum in most circumstances. This means you can take more in years with higher spending needs, such as a holiday or a home renovation, and less in quieter years.

Retirement calculators and tools that model different drawdown scenarios can help you see the long-term impact of these decisions, especially when combined with property income or a property investment strategy for retirement.

The Retirement Standard makes clear that account-based pensions offer the most flexibility of all super income stream options, while annuities provide the greatest certainty. For many retirees, the best outcome comes from holding both.

Navigating the nuances: flexibility, trade-offs, and expert insights

With the core strategies outlined, it's important to consider some expert perspectives and critical nuances.

The ASFA lump sum targets, while widely cited, have been questioned by actuaries as potentially conservative. Some retirees achieve a comfortable lifestyle with considerably less by optimising how they layer income sources, structuring their super drawdowns strategically, and taking full advantage of available government entitlements. This doesn't mean the benchmarks are wrong, but rather that they represent one scenario among many.

There are several important trade-offs to understand when designing your personal income mix:

- Flexibility versus certainty. An account-based pension gives you control over how much you draw and lets you leave residual capital to your estate. An annuity removes that flexibility but eliminates the risk of outliving your income. The right balance depends on your health, life expectancy, and how much you value predictability.

- Liquidity versus returns. Property can generate strong long-term returns but is illiquid. If you need $50,000 quickly for a medical expense, you cannot sell half a bedroom. Balancing property with liquid assets like shares or cash is therefore important.

- Tax efficiency versus simplicity. Structuring income to minimise tax across super, the Age Pension, and non-super sources can be complex. It may involve decisions about when to withdraw from super, how to structure an investment portfolio, and whether an SMSF versus an industry super fund better suits your needs.

"The best retirement income plan is one you can actually manage and adjust over time, not the one that looks optimal on paper at age 60."

Pro Tip: If you're unsure where to start, a retirement planning checklist can help you identify what you've already addressed and what still needs attention. Working through a structured checklist is often more productive than trying to optimise everything at once.

One commonly overlooked element is the role of part-time or flexible work in the early years of retirement. Many Australians retire from a full-time role but continue to work casually, consult in their field, or generate income from a small business or creative pursuit. This "transition income" reduces the pressure on super and other savings, allowing capital to continue growing during a period when returns can still have a significant long-term impact.

The most successful retirement income strategies tend to share a common quality: they are built to evolve. Rather than locking in a single approach and hoping it works for 30 years, they include built-in flexibility, regular review points, and the ability to shift between income sources as circumstances change.

The myth of one perfect retirement formula

Here is an uncomfortable truth: the financial services industry often sells retirement planning as though there is a correct answer, a magic number, a single portfolio allocation, or a specific product that will solve everything. There isn't.

Australian retirees who genuinely thrive are not those who hit an exact super balance at 67. They're the ones who build a system that responds to real life. They might reduce their drawdown during a market downturn, pick up some consulting work for two years, reassess their property when maintenance costs climb, and take a full holiday when the market recovers. They review their position regularly and make small adjustments rather than waiting for a perfect plan to play out.

The most resilient retirement strategies treat income as a living system, not a set-and-forget mechanism. Chasing a secure retirement future isn't about perfection at the starting line. It's about building enough flexibility to handle what you don't yet know is coming. That mindset, more than any particular product or number, is what separates the retirees who feel financially secure from those who feel anxious about every market move.

Transform your strategy with smarter retirement tools

If you're ready to move from knowledge to action, AlphaIQ can support your journey with purpose-built tools designed for self-directed Australian investors.

AlphaIQ gives you the ability to project your superannuation balance under different contribution and return scenarios, so you can see exactly where you're headed before you get there. You can also run debt recycling calculations to understand whether restructuring debt could accelerate your wealth position heading into retirement. If you want to see everything in one place, explore the full suite of AlphaIQ tools built to help you model, optimise, and stress-test your retirement income plan, without the ongoing cost of financial advice.

Frequently asked questions

What are the main sources of income in Australian retirement?

The main sources include the Age Pension, superannuation income streams such as account-based pensions and annuities, and non-super assets like shares, property, and part-time work.

How much super do I need to retire comfortably in Australia?

ASFA recommends $730,000 for a couple or $630,000 for a single person at age 67 to fund a comfortable retirement lifestyle, assuming a part Age Pension.

Is the Age Pension enough to live on in retirement?

For most Australians, the Age Pension alone does not cover a comfortable retirement and is typically combined with super or other income streams to bridge the gap.

What if I can't reach the ASFA lump sum targets?

Some retirees achieve a comfortable lifestyle with less by thoughtfully layering income sources across super, the Age Pension, property, and investments rather than depending on super alone.

How can I make my retirement income more stable?

Diversifying across super, the Age Pension, investments, and flexible work can reduce reliance on any single source, providing greater stability as highlighted by Australian retirement income guidance.