TL;DR:

- Managed funds pool investors' money for professional asset management across various securities and property. They come in different structures, with active and passive management styles, and can be unlisted or listed on exchanges, offering diversification and convenience for Australian investors. Fees, including management expenses and transaction costs, significantly impact long-term returns and should be carefully compared before investing.

A managed fund is a pooled investment vehicle where multiple investors contribute money and a professional fund manager invests it on their behalf across assets such as shares, bonds, property, and cash. In Australia, managed funds typically operate as open-ended unit trusts, meaning investors hold units rather than owning the underlying assets directly. Understanding what are managed funds and how they work is the first step toward deciding whether they belong in your wealth-building strategy. For investors aged 30–55 building a diversified portfolio, managed funds offer a practical way to access professional investment management without needing to pick individual stocks or bonds yourself.

How do managed funds work?

When you invest in a managed fund, you purchase units in the fund. Each unit represents your proportional share of the total pool. The unit price fluctuates daily based on the net market value of the underlying assets, whether that is Australian shares, global equities, fixed income, or property. If the assets rise in value, your unit price rises. If they fall, so does your unit price.

The fund manager handles all the day-to-day investment decisions. They conduct research, select assets, and adjust holdings according to the fund's documented strategy and risk profile. You do not need to monitor markets or execute trades. That responsibility sits entirely with the manager.

Managed funds also generate income through distributions. These are payments made to unit holders from dividends, interest, or rental income earned by the fund's assets. Distributions are typically paid quarterly or annually, and you can usually choose to receive them as cash or reinvest them as additional units.

The open-ended structure of most Australian managed funds means new investors can enter and existing investors can exit at any time. When you redeem your units, the fund sells assets to return your capital. This differs from shares, which require a buyer on the other side of your trade.

Pro Tip: Before investing, read the fund's Product Disclosure Statement (PDS). It outlines the investment strategy, fee structure, and risk profile in plain language. Comparing PDS documents across funds is the most reliable way to make an informed choice.

What are the types of managed funds?

Managed funds come in several structures and management styles. Understanding the differences helps you match a fund to your goals and risk tolerance.

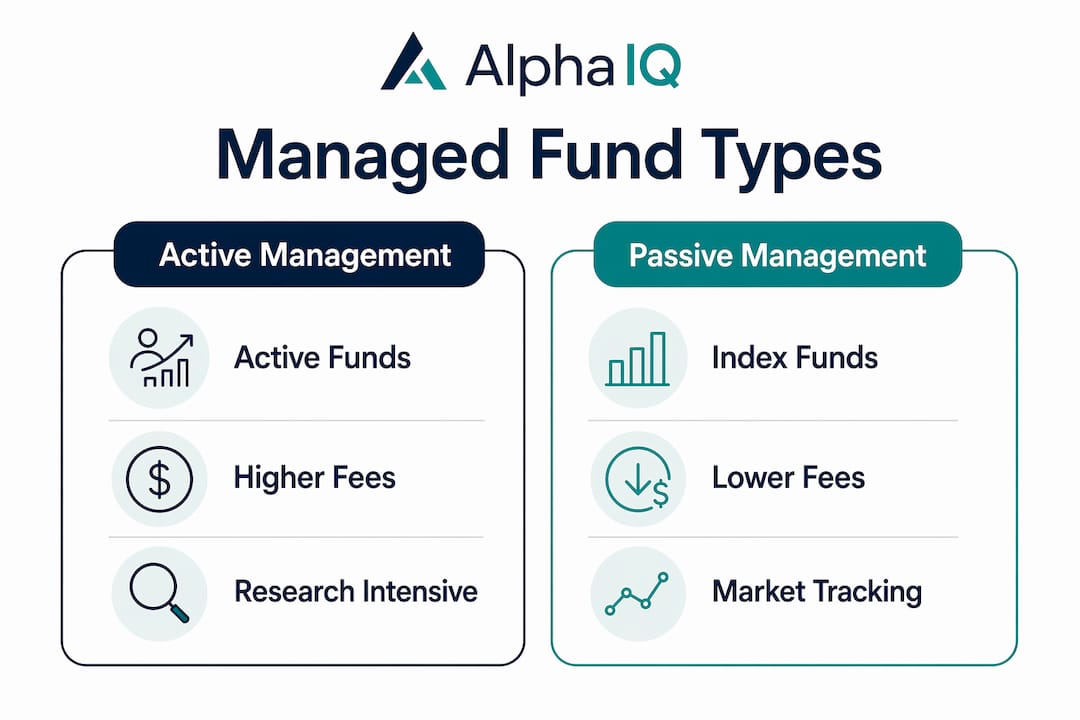

Active vs passive management

The most significant distinction is between active and passive management. Active funds aim to outperform a market benchmark by selecting assets the manager believes will deliver superior returns. Passive funds, by contrast, track an index such as the ASX 200 or the MSCI World Index, holding the same assets in the same proportions as the index itself.

Active management requires more research and trading, which means higher fees. Passive management is lower cost because it follows a rules-based approach with minimal human intervention. Neither style guarantees better outcomes. Active managers sometimes outperform their benchmarks, but many do not do so consistently over long periods.

Unlisted vs listed funds

The second key distinction is how you buy and sell the fund.

- Unlisted managed funds require you to apply directly to the fund's responsible entity. You transact at the next calculated unit price, which is typically determined at the end of each business day.

- Listed managed funds, commonly known as exchange-traded funds (ETFs), trade on the ASX just like shares. You buy and sell through a broker at market prices throughout the trading day.

The table below summarises the key differences between these two structures.

| Feature | Unlisted Managed Fund | Listed Fund (ETF) |

|---|---|---|

| How you buy | Apply to the fund directly | Buy via a stockbroker or trading platform |

| Pricing | End-of-day unit price | Real-time market price |

| Liquidity | Redeemed by the fund | Sold to another buyer on exchange |

| Typical fees | Higher (especially active funds) | Generally lower |

| Minimum investment | Often $1,000–$5,000 | Cost of one unit or share |

Asset class focus

Managed funds also differ by what they invest in. Single-asset funds focus on one category, such as Australian shares or global fixed income. Multi-sector funds, sometimes called balanced or diversified funds, spread money across several asset classes simultaneously. For investors who want broad portfolio diversification in a single product, multi-sector funds are often the starting point.

What are the advantages of managed funds for australian investors?

Managed funds offer several genuine benefits, particularly for investors who want market exposure without the time commitment of managing a portfolio themselves.

- Professional management. Fund managers handle buying, selling, income collection, and portfolio rebalancing on your behalf. You benefit from their research capabilities and market access without needing to replicate that work yourself.

- Diversification. Managed funds typically hold dozens or hundreds of securities across multiple sectors or geographies. This spreads risk across asset classes and reduces your exposure to any single company or market event.

- Accessibility. Many managed funds allow entry with relatively modest minimum investments. This gives you access to asset classes, such as commercial property or global infrastructure, that would otherwise require significant capital to access directly.

- Convenience for time-poor investors. If you are building wealth alongside a demanding career or family commitments, managed funds remove the need for daily market monitoring. The fund operates whether you are watching or not.

- Compatibility with superannuation. Many Australian superannuation funds invest your contributions into managed fund options, such as growth, balanced, or conservative portfolios. Understanding how these options work gives you more control over your superannuation investment choices and long-term retirement outcomes.

In New Zealand, KiwiSaver schemes operate as a form of managed fund with locked-in contributions and favourable tax treatment, demonstrating how managed fund structures can be embedded into national retirement savings systems. Australia's superannuation system works on a similar principle.

What fees are involved in managed funds?

Fees are one of the most important factors when comparing managed funds. They directly reduce your net return, so understanding what you are paying for matters.

- Management fee (MER). The management expense ratio is the annual cost of running the fund, expressed as a percentage of your investment. Active funds typically charge between 0.5% and 1.5% per year. Passive index funds often charge between 0.05% and 0.5% per year.

- Performance fee. Some active managers charge an additional fee when the fund outperforms its benchmark. This can be a reasonable structure if the manager consistently delivers, but it adds cost in strong market years regardless of whether the outperformance was skill or luck.

- Buy/sell spread. When you enter or exit a fund, you may pay a small spread that covers the transaction costs of buying or selling the underlying assets. This is not a fee paid to the manager but a cost embedded in the unit price.

- Platform or administration fees. If you invest through a wrap account or investment platform, additional administration fees may apply on top of the fund's own charges.

Fees compound over time in the same way returns do. A 1% difference in annual fees on a $200,000 portfolio over 20 years can amount to tens of thousands of dollars in lost wealth. That is not a trivial difference. Comparing fees across funds with similar strategies is one of the highest-value steps you can take before committing capital.

Pro Tip: Use the fund's PDS to find the total MER, not just the base management fee. Some funds list fees separately, and the total cost only becomes clear when you add them together. For a practical framework on comparing investment fees, look at fee structures across account types before you invest.

Key takeaways

Managed funds give Australian investors access to professional portfolio management and broad diversification, but the right fund depends on your goals, time horizon, and fee tolerance.

| Point | Details |

|---|---|

| Managed fund definition | A pooled investment vehicle where a professional manager invests on behalf of unit holders. |

| Active vs passive | Active funds aim to beat a benchmark; passive funds track one. Passive funds typically cost less. |

| Unlisted vs listed | Unlisted funds transact at end-of-day prices; ETFs trade on the ASX in real time. |

| Fees reduce returns | A 1% annual fee difference compounds significantly over a 20-year investment horizon. |

| Super connection | Most Australian super funds invest contributions into managed fund options. Knowing this gives you more control. |

Why i think most investors underestimate the fee question

After spending years working through investment decisions with Australian self-directed investors, the pattern I see most often is this: people spend considerable time choosing between fund managers and almost no time comparing fees. That is the wrong order of priorities.

The research on active management is clear enough. Most active managers do not consistently outperform their benchmark after fees over long periods. That does not mean active funds are always the wrong choice. There are asset classes, such as small-cap equities or emerging markets, where skilled active management can add genuine value. But in large-cap Australian or US equities, the evidence for paying a premium is thin.

What I find more useful than the active-versus-passive debate is thinking about managed funds as a complement to your broader wealth management strategy, not a replacement for it. A managed fund inside your super, combined with a direct share portfolio and perhaps an investment property, gives you diversification across structures as well as asset classes. That layering is where the real benefit shows up over time.

The investors I see make the best decisions are those who know exactly what they own, what it costs, and how it fits their overall financial position. Managed funds are a tool. Like any tool, they work well when used with intention.

— Jonathan

See your full financial picture with Alphaiq

Understanding managed funds is one piece of the puzzle. Knowing how they fit alongside your superannuation, property, and other investments is where the real clarity comes from.

Alphaiq is an Australian wealth intelligence platform built for self-directed investors who want to model their financial position with real numbers. You can run scenario simulations across your investments, use the superannuation calculator to project your retirement income, and see how managed fund choices interact with your tax position, franking credits, and super contributions. Explore the Alphaiq platform to take control of your wealth decisions with confidence.

FAQ

What is the managed fund definition in simple terms?

A managed fund is a pooled investment where multiple investors contribute money and a professional manager invests it across assets such as shares, bonds, property, and cash. Investors hold units representing their share of the pool rather than owning the underlying assets directly.

How do managed funds differ from etfs?

Both are types of managed funds, but ETFs trade on a stock exchange like shares, with real-time pricing throughout the day. Unlisted managed funds transact at an end-of-day unit price calculated by the fund's responsible entity.

Should i invest in managed funds through my super?

Most Australian superannuation funds already invest your contributions into managed fund options such as growth, balanced, or conservative portfolios. Reviewing which option your super is invested in and whether it matches your risk profile and time horizon is a practical starting point.

What fees should i expect from a managed fund?

Managed funds charge a management expense ratio, typically between 0.05% and 1.5% per year depending on whether the fund is passive or active. Some funds also charge performance fees and a buy/sell spread on entry and exit.

Are managed funds suitable for building long-term wealth?

Managed funds suit investors who want diversified market exposure without managing individual securities. They work well as part of a broader investment strategy that may include direct shares, property, and superannuation, particularly for investors with a time horizon of five years or more.