TL;DR:

- Annuities convert a lump sum into guaranteed lifetime income, effectively addressing longevity risk in retirement. They come in various types like SPIAs, MYGAs, and FIAs, each suited to different financial goals and risk profiles. Integrating 20% to 30% of retirement savings into annuities provides dependable income while preserving liquidity for unexpected needs.

An annuity is a financial product that converts a lump sum into a guaranteed stream of income payments, making it one of the most direct tools for addressing longevity risk in retirement. The role of annuities in retirement has grown in relevance as fewer Australians retire with defined benefit pensions and superannuation balances must stretch across decades of spending. Products like Single Premium Immediate Annuities (SPIAs) and Multi-Year Guaranteed Annuities (MYGAs) fill the income gap left when guaranteed sources such as the Age Pension fall short of covering essential expenses. Understanding how these products work, what they cost, and where they fit in a broader portfolio is the foundation of a sound retirement income strategy.

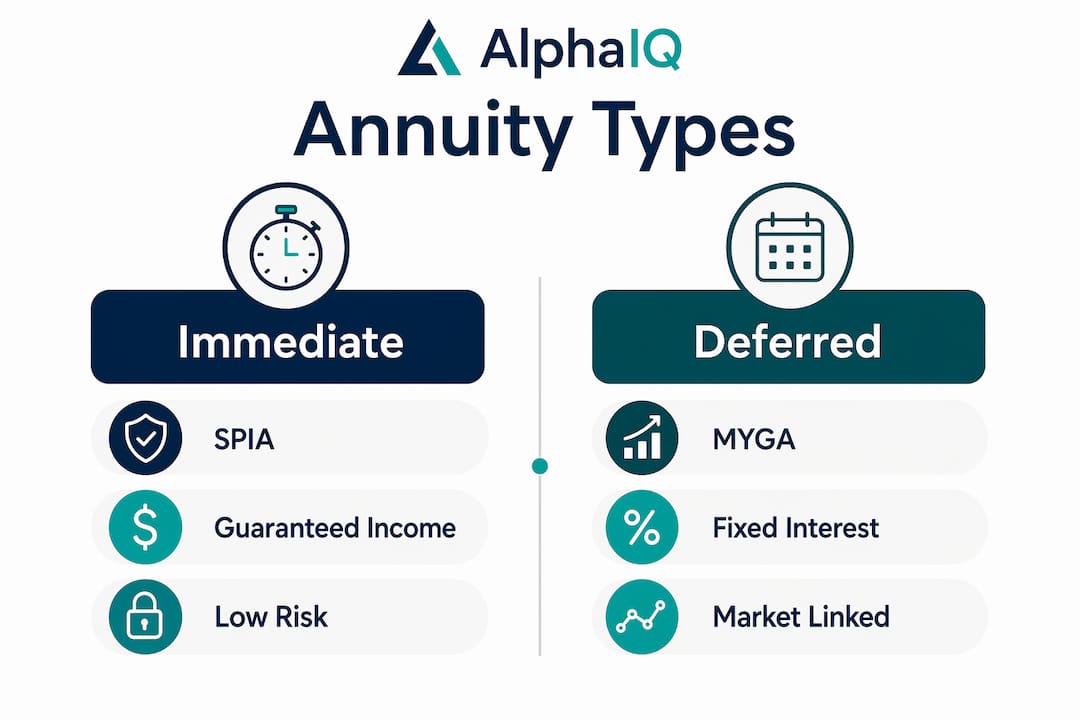

What types of annuities exist and how do they differ?

Three annuity types dominate retirement income planning: SPIAs, MYGAs, and Fixed Indexed Annuities (FIAs). Each serves a distinct purpose, and choosing the wrong type for your situation is one of the most common and costly mistakes retirees make.

A Single Premium Immediate Annuity (SPIA) begins paying income within one month of purchase. You hand over a lump sum and receive regular payments for life or a fixed term. A 65-year-old purchasing a SPIA in 2026 receives approximately $595 monthly per $100,000 invested, representing a 5.7% initial payout rate. That figure is meaningful because it exceeds what most conservative bond portfolios currently yield, and the income is guaranteed regardless of how long you live.

A Multi-Year Guaranteed Annuity (MYGA) functions more like a term deposit with tax-deferred growth. You lock in a fixed interest rate for a set period, typically two to ten years, without receiving immediate income. Top-rated 5-year MYGAs in 2026 offer rates between 4.75% and 5.25%, which currently exceeds standard term deposit rates. This makes MYGAs attractive for pre-retirees who want to grow a portion of their savings in a protected, tax-deferred environment before converting to income later.

A Fixed Indexed Annuity (FIA) links growth to a market index such as the S&P 500 but protects your principal from losses. Growth is capped, but you cannot lose your initial investment due to market downturns. FIAs suit retirees who want some upside participation without full market exposure.

| Annuity type | How income works | Risk profile | Best suited for |

|---|---|---|---|

| SPIA | Immediate, guaranteed payments for life or term | Very low | Covering essential expenses from day one of retirement |

| MYGA | Fixed interest, deferred income | Very low | Pre-retirees growing savings before drawing income |

| FIA | Index-linked growth, protected principal | Low to moderate | Retirees wanting growth potential with downside protection |

Pro Tip: If you are within five years of retirement, a MYGA can serve as a holding vehicle for funds you plan to convert into a SPIA later, locking in today's rates while deferring the income start date.

What are the key benefits and potential drawbacks of annuities?

Annuities offer a set of protections that no other financial product replicates exactly. They also carry limitations that make them unsuitable for every dollar in your portfolio.

The core benefits

- Guaranteed lifetime income. Mortality credits pool longevity risk across all policyholders, enabling insurers to pay income for life at rates a self-managed withdrawal strategy cannot match. This pooling creates value that is genuinely unattainable through individual portfolio withdrawals.

- Sequence-of-returns protection. Annuities eliminate sequence-of-returns risk by funding essential expenses with a guaranteed floor, so you never need to sell growth assets at a loss during a market downturn to pay your bills. This is one of the most underappreciated advantages of annuities for retirees who hold shares or property alongside their income products.

- Behavioural benefits. Research from Fidelity confirms that guaranteed income reduces spending guilt and financial anxiety in retirement. Retirees with a secure income floor spend more confidently and report better financial wellbeing. This is not a soft benefit. It directly affects quality of life and how effectively you use your accumulated wealth.

- Tax-deferred growth. MYGAs and deferred annuities grow without annual tax on earnings, which can be a meaningful advantage when managing tax in retirement across multiple income sources.

The real drawbacks

- Reduced liquidity. Once you purchase a SPIA, the capital is generally inaccessible. Surrender charges on MYGAs and FIAs can apply for several years after purchase.

- Inflation risk. A fixed monthly payment loses purchasing power over time. Inflation protection riders such as cost-of-living adjustments reduce the initial payout rate but preserve real income over a long retirement.

- Carrier credit risk. Your income depends on the financial strength of the issuing insurer. Selecting highly rated carriers and understanding your state or territory's protection scheme is non-negotiable.

- Not suited to all goals. Annuities are not appropriate for retirees who prioritise aggressive portfolio growth, need immediate liquidity, or plan to leave a large estate.

Pro Tip: Always check the insurer's credit rating from a recognised agency before committing. An annuity is only as secure as the company backing it.

How do annuities compare to other retirement income strategies?

Annuities occupy a specific and irreplaceable position in the retirement income toolkit, but they work best alongside other strategies rather than as a standalone solution.

The most common alternative to an annuity is a portfolio withdrawal strategy, where you draw down a percentage of your investment portfolio each year. This approach preserves capital and offers flexibility, but it exposes you to sequence-of-returns risk and the psychological burden of watching your balance decline. A retiree drawing 5% annually from a share portfolio during a 30% market correction faces a compounding problem that a SPIA holder simply does not face.

Defined benefit pensions and the Age Pension function similarly to annuities in that they provide predictable, recurring income. Where these sources fall short of covering essential monthly expenses, an annuity fills the gap precisely. This is why financial planners often describe annuities as a way to extend your "pension floor" rather than replace your investment portfolio. Exploring diverse income streams in retirement is the most resilient approach, and annuities are one layer of that structure.

Bonds and term deposits offer capital preservation and predictable returns but do not provide lifetime income guarantees. A 10-year bond matures; a SPIA does not. For retirees concerned about outliving their savings, that distinction matters considerably.

| Income strategy | Lifetime guarantee | Market exposure | Liquidity | Best role in retirement |

|---|---|---|---|---|

| SPIA annuity | Yes | None | Very low | Covering non-negotiable monthly expenses |

| Portfolio withdrawals | No | High | High | Funding discretionary spending and growth |

| Age Pension | Yes (government) | None | N/A | Base income floor for eligible retirees |

| Term deposits / bonds | No | Low | Moderate | Short-term capital preservation |

Experts recommend allocating 20% to 30% of your retirement portfolio to annuities. This range balances the certainty of guaranteed income against the need to maintain liquid assets for unexpected expenses, healthcare costs, and discretionary spending. Going beyond 30% risks locking up too much capital in an illiquid product.

How to integrate annuities into your retirement plan

Knowing that annuities are useful is one thing. Knowing how much to buy, when to buy, and which type to choose is where the real planning work happens.

-

Calculate your income floor gap. Add up your essential monthly expenses: housing costs, utilities, food, healthcare, and insurance. Subtract your guaranteed income from the Age Pension and any existing pension or super drawdown. The income floor gap is the amount an annuity needs to cover. This figure, not a rule of thumb, determines how much annuity income you actually need.

-

Determine your break-even age. Divide your total annuity premium by the annual payout to find the number of years required to recoup your investment. This break-even calculation helps you assess whether a lifetime annuity makes financial sense given your health, family history, and inheritance goals. For a 65-year-old paying $200,000 for a SPIA returning $11,400 annually, the break-even point is approximately 17.5 years, or age 82.5.

-

Choose the right timing. SPIAs and lifetime income annuities are generally most efficient when purchased between ages 60 and 70, when payout rates are higher and the income period is long enough to justify the premium. MYGAs can be purchased at any age as a savings vehicle, with the intention of converting to income later.

-

Decide on joint or single cover. If you have a partner, a joint-life annuity continues payments to the surviving spouse. Single-life annuities pay more per month but cease at death. The right choice depends on your partner's independent income sources and your combined financial position.

-

Consider inflation protection. Adding a cost-of-living adjustment rider reduces your starting payout but protects purchasing power over a 20 to 30-year retirement. For retirees in their early 60s, this trade-off is often worth making.

Pro Tip: Do not commit your entire annuity budget at once. Laddering purchases across several years lets you capture different rate environments and adjust your income floor as your spending needs become clearer.

Understanding how annuities interact with your broader investment risk profile is the final piece of the puzzle. Annuities reduce portfolio risk by removing the income dependency on volatile assets, which in turn allows the remaining portfolio to be invested with a longer time horizon and higher growth potential.

Key takeaways

Annuities provide the most reliable solution to longevity risk in retirement by converting capital into guaranteed lifetime income that no portfolio withdrawal strategy can replicate.

| Point | Details |

|---|---|

| Annuity types vary significantly | SPIAs provide immediate income, MYGAs offer deferred growth, and FIAs link returns to a market index with principal protection. |

| Allocation should stay within 20–30% | Exceeding 30% of your portfolio in annuities reduces liquidity and limits your ability to respond to unexpected costs. |

| Income floor gap drives sizing | Calculate essential expenses minus guaranteed income to determine exactly how much annuity income you need, not a percentage guess. |

| Behavioural benefits are real | Guaranteed income reduces spending anxiety and allows retirees to use their wealth more effectively throughout retirement. |

| Inflation riders reduce but protect | Cost-of-living adjustments lower your starting payout but are worth considering for retirements spanning 25 years or more. |

Why I think most people get annuities wrong

Most of the hesitation I see around annuities comes from a misunderstanding of what they are for. People compare them to investment products and conclude they offer poor returns. That is the wrong comparison. A SPIA is not competing with your share portfolio. It is competing with the anxiety of not knowing whether your income will last.

The retirees who benefit most from annuities are not those with the largest balances. They are the ones whose essential expenses exceed their guaranteed income from the Age Pension and super drawdown. For that group, an annuity is not a luxury. It is the difference between a retirement spent confidently and one spent rationing.

The pitfall I see most often is over-allocation. Putting 60% or 70% of a retirement portfolio into annuities leaves almost no flexibility for healthcare surprises, home repairs, or simply wanting to help a child with a house deposit. The 20% to 30% guideline exists for good reason. Treat it as a ceiling, not a target.

The other mistake is ignoring inflation. A fixed income that feels comfortable at 65 can feel tight at 80 if prices have risen substantially. Paying slightly less per month now for a cost-of-living adjustment is a decision your future self will appreciate.

Annuities are not the answer to every retirement income problem. But for covering the non-negotiable expenses that must be paid regardless of what markets do, they are the most direct and reliable tool available.

— Jonathan

Model your annuity strategy with Alphaiq

Understanding the role of annuities in retirement is one thing. Seeing how a specific allocation affects your projected income, tax position, and portfolio longevity is where real decisions get made.

Alphaiq's retirement projection calculator lets you model different annuity allocations alongside your superannuation balance, investment portfolio, and Age Pension entitlements. You can test scenarios, adjust income start dates, and see the long-term impact of adding a guaranteed income floor to your retirement plan. The Alphaiq platform gives you the numbers to make confident, informed decisions without the cost of ongoing financial advice.

FAQ

What is the role of annuities in retirement?

Annuities provide guaranteed income payments that cover essential living expenses, reducing dependence on volatile investment returns and protecting retirees from outliving their savings.

How do fixed and variable annuities differ?

Fixed annuities, including SPIAs and MYGAs, pay a set income or guaranteed interest rate. Variable annuities link returns to investment sub-accounts, meaning income can rise or fall with market performance.

How much of my retirement savings should go into an annuity?

Experts recommend allocating no more than 20% to 30% of your retirement portfolio to annuities, preserving enough liquidity for unexpected expenses and discretionary spending.

When is the best time to buy a lifetime income annuity?

Purchasing a lifetime income annuity between ages 60 and 70 typically offers the most efficient payout rates, as the income period is long enough to justify the premium and rates reflect your age at purchase.

Do annuities protect against inflation?

Standard fixed annuities do not automatically adjust for inflation, but cost-of-living adjustment riders are available. These riders reduce the initial payout rate but help maintain purchasing power over a long retirement.