TL;DR:

- Retirement income taxation varies based on account type and contribution origin, affecting after-tax income. Strategic withdrawal sequencing, income timing, and Roth conversions can significantly reduce tax burdens and Medicare surcharges. Proper planning during the early retirement years maximizes tax efficiency and safeguards long-term financial stability.

Taxation in retirement is defined as the set of rules that determine how much tax you pay on income drawn from superannuation, pensions, investment accounts, and government benefits once you stop working. Many Australians approaching retirement are surprised to discover that not all retirement income is treated equally by the tax office. Some withdrawals are taxed as ordinary income, others are partially taxable, and some are entirely tax-free depending on the account type and your age. Understanding these distinctions is the foundation of sound tax planning for retirees, and getting it right can meaningfully increase your after-tax income over a 20 to 30 year retirement.

How retirement income is taxed: key principles

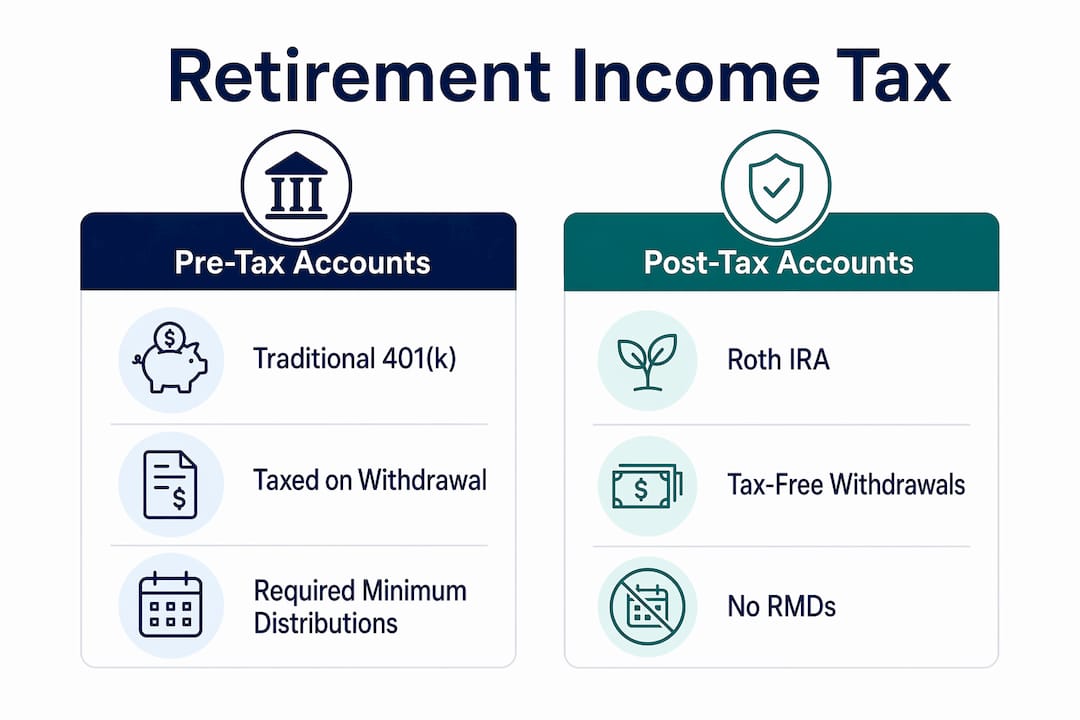

The tax treatment of your retirement income depends primarily on whether your original contributions were made with pre-tax or after-tax dollars. This single distinction drives most of the complexity in retirement taxation strategies.

Traditional pre-tax accounts, such as a standard 401(k) in the United States or a pre-tax superannuation accumulation account in Australia, defer tax until withdrawal. When you draw from these accounts in retirement, the full amount is generally taxed as ordinary income at your marginal rate. Roth-style accounts work in reverse: contributions are made from after-tax dollars, so qualified Roth withdrawals are federally tax-free. This distinction matters enormously for long-term planning because tax-free withdrawals do not count toward income thresholds that trigger Medicare surcharges or increase the taxable portion of Social Security benefits.

Required minimum distributions (RMDs) add another layer. RMDs generally start at age 73 for traditional retirement accounts, forcing taxable withdrawals whether you need the money or not. Roth accounts are not subject to RMDs during the original owner's lifetime, which is one reason many retirees convert portions of their traditional balances to Roth accounts in the years before RMDs begin.

| Account type | Tax on contributions | Tax on withdrawals |

|---|---|---|

| Traditional 401(k) / pre-tax super | Pre-tax (deductible) | Taxed as ordinary income |

| Roth 401(k) / after-tax super | After-tax (no deduction) | Tax-free if qualified |

| Taxable investment account | After-tax | Capital gains rates apply |

| Pension / defined benefit | Varies by plan | Generally taxable federally |

Pro Tip: If you are between retirement and age 73, you have a window to convert traditional account balances to Roth at potentially lower tax rates before RMDs force larger taxable withdrawals.

How are Social Security benefits taxed?

Social Security benefits are not fully tax-free, and the rules catch many retirees off guard. The taxable portion depends on your provisional income, which is calculated as your adjusted gross income plus non-taxable interest plus half of your annual Social Security benefit. This figure is distinct from your standard adjusted gross income, and understanding the difference is central to managing your retirement tax implications.

The thresholds work in tiers. Social Security benefits become taxable at up to 50% for single filers with provisional income between $25,000 and $34,000, and up to 85% above $34,000. For married couples filing jointly, the equivalent thresholds are $32,000 and $44,000. This means a retiree with a modest investment income could find the majority of their Social Security benefit subject to federal tax.

Filing status also matters significantly. Married taxpayers who file separately and lived with their spouse during the year face a zero base amount, meaning most of their benefits become taxable immediately. This is a filing trap that costs retirees thousands of dollars annually.

Strategies to reduce the taxable portion of your benefit include:

- Drawing from Roth accounts instead of traditional accounts, since Roth withdrawals do not count toward provisional income

- Deferring Social Security claiming to reduce the number of years subject to taxation

- Managing investment income carefully to stay below the 50% taxability threshold

- Timing large one-off income events, such as property sales, to years before or after Social Security commencement

Practitioners now treat retirement withdrawals as tax-return engineering across AGI, MAGI, and provisional income simultaneously. That framing captures how interconnected these calculations really are.

What is IRMAA and how does it affect your Medicare premiums?

IRMAA, the Income-Related Monthly Adjustment Amount, is a surcharge applied to Medicare Part B and Part D premiums when your income exceeds certain thresholds. It is one of the most financially significant and least understood retirement tax implications for higher-income retirees.

The calculation uses a two-year lookback. For 2026, IRMAA surcharges are based on your 2024 Modified Adjusted Gross Income (MAGI), with the first surcharge tier beginning at $109,000 for single filers and $218,000 for couples. This means income decisions you make today can affect your Medicare premiums two years from now.

The structure is a cliff, not a slope. Exceeding an IRMAA threshold by even one dollar triggers the full surcharge for that tier, which can add thousands of dollars per year to your healthcare costs. A one-time income spike from a Roth conversion, a capital gain, or an RMD can push you into a higher tier and keep you there for two years if the elevated income appears in consecutive tax years.

Here is how to manage IRMAA exposure:

- Model your MAGI two years ahead. Because premiums are based on prior income, planning must start well before retirement.

- Spread Roth conversions across multiple years. Converting smaller amounts annually avoids a single large income spike that crosses a tier boundary.

- Time capital gains carefully. Realising large gains in a year when other income is low reduces the risk of crossing a threshold.

- Appeal if a life event changed your income. The Social Security Administration accepts appeals based on qualifying life events such as retirement, divorce, or the death of a spouse.

- Review your MAGI annually. Regular review lets you make adjustments before the two-year lookback locks in your premium tier.

Pro Tip: Planning Roth conversions between retirement and Social Security claiming is one of the most effective windows for managing future IRMAA exposure, but each conversion adds to your income in the year it occurs, so model the full impact before acting.

Withdrawal sequencing strategies to minimise tax

The order in which you draw from different account types is one of the most powerful tools in retirement tax planning. Withdrawing first from taxable accounts, then from tax-deferred accounts, and finally from Roth accounts is the traditional sequencing approach. It preserves tax-free Roth growth for as long as possible while drawing down assets that would otherwise generate ongoing taxable income.

The logic behind this sequence is straightforward. Taxable investment accounts often hold assets with unrealised capital gains that are taxed at preferential rates, generally lower than ordinary income rates. Drawing these down first keeps your taxable income lower in early retirement, which can reduce Social Security taxation and keep you below IRMAA thresholds. Tax-deferred accounts are drawn next, and Roth accounts are preserved as a tax-free reserve for later years or for estate planning purposes.

Proportional withdrawal strategies offer an alternative. Rather than depleting one account type before touching another, you draw from all account types simultaneously in proportions designed to keep your total taxable income within a target bracket. This approach smooths your tax rate across retirement rather than front-loading or back-loading the tax burden.

Roth conversions fit into both strategies as a proactive tool. Careful Roth conversion planning between retirement and Social Security claiming can reduce future RMDs and lower provisional income in later years, but conversions increase income in the conversion year. The trade-off requires modelling across multiple scenarios.

Consider two retirees with identical account balances. Retiree A draws entirely from a traditional IRA, pushing income into a higher bracket and triggering 85% Social Security taxation. Retiree B draws the same total amount but splits withdrawals between a traditional IRA and a Roth account, keeping provisional income below the 50% Social Security threshold. Retiree B pays materially less tax on the same retirement income. That difference, compounded over 20 years, is significant.

You can explore tax-efficient withdrawal approaches in more detail to see how sequencing applies specifically to Australian superannuation structures.

Understanding pension and annuity tax treatment

Pensions and annuities are generally taxable at the federal level and potentially at the state level as well, though the taxable portion depends on whether after-tax contributions were made during the accumulation phase. This distinction is frequently misunderstood and can lead to retirees over-reporting or under-reporting their taxable income.

When a pension includes after-tax contributions, those contributions are returned to you tax-free over the life of the payments. The taxable portion is shown on Form 1099-R in the United States, or on equivalent tax statements for Australian income streams. The taxable amount on Form 1099-R is what you report as income, not the total payment received. Where Box 2b on the form is marked as "taxable amount not determined," you are responsible for calculating the exclusion ratio yourself, which is where many retirees encounter problems.

Practical steps to manage pension taxation accurately:

- Review your annual tax statement carefully and compare the total payment to the stated taxable amount

- Keep records of all after-tax contributions made during your working years, as these reduce your taxable pension income

- Confirm whether your state taxes pension income, since several states exempt pension income entirely or partially

- Seek professional advice if your pension includes a mix of pre-tax and after-tax contributions, as the exclusion ratio calculation can be complex

- Check whether withholding on your pension payments aligns with your actual tax liability to avoid underpayment penalties

For Australians, the equivalent consideration applies to account-based pensions drawn from superannuation, where the tax-free and taxable components of your super balance determine the tax treatment of each payment. Understanding diverse retirement income streams and their respective tax treatments is worth reviewing as part of your broader income plan.

Key takeaways

Effective retirement tax planning requires coordinating withdrawal sequencing, account type selection, and income timing across superannuation, pensions, Social Security, and investment accounts simultaneously.

| Point | Details |

|---|---|

| Account type determines tax | Pre-tax accounts are taxed on withdrawal; Roth and after-tax accounts may allow tax-free income. |

| Social Security is partially taxable | Up to 85% of benefits can be taxed depending on your provisional income level. |

| IRMAA creates premium cliffs | Exceeding Medicare income thresholds by one dollar triggers the full surcharge for that tier. |

| Withdrawal order changes outcomes | Drawing from taxable accounts first, then tax-deferred, then Roth reduces overall tax across retirement. |

| Pension tax requires careful review | The taxable portion of pension payments depends on after-tax contributions and must be verified annually. |

Why most retirees underestimate their tax burden

I have seen this pattern repeatedly: retirees who planned their income carefully during their working years arrive at retirement with a clear budget in mind, then discover their after-tax income is significantly lower than expected. The gap is almost always explained by the interaction of Social Security taxation, IRMAA surcharges, and RMDs arriving simultaneously in their mid-seventies.

The uncomfortable truth is that retirement tax planning is not a one-time exercise. The rules interact in ways that are genuinely difficult to model without running multiple scenarios. A Roth conversion that looks attractive in isolation can push you into a higher IRMAA tier and increase the taxable portion of your Social Security benefit in the same year. That compounding effect is what catches people off guard.

My view is that the window between retirement and age 73 is the most valuable planning period most retirees ignore. Income is often lower, RMDs have not started, and you have real flexibility to convert balances, realise capital gains at lower rates, and shape your future tax position. Waiting until RMDs force the issue removes most of that flexibility.

The coordinated, client-centred approach that tax professionals recommend, integrating bracket management, withdrawal sequencing, and Medicare surcharge awareness, is not overcomplicated advice. It is the minimum required to avoid leaving significant money on the table. Start modelling early, review annually, and treat your tax position as a dynamic variable rather than a fixed cost.

— Jonathan

Model your retirement tax position with Alphaiq

Understanding the theory of retirement taxation is one thing. Seeing how it applies to your specific super balance, income mix, and withdrawal timeline is where real decisions get made.

Alphaiq is built for Australian investors who want to model exactly this kind of scenario. The AlphaIQ platform combines tax-aware financial modelling with superannuation projections, letting you test different withdrawal sequences, Roth-equivalent conversion strategies, and income timing decisions against your actual numbers. The superannuation calculator gives you a clear projection of your retirement income with tax considerations built in, so you can plan with confidence rather than guesswork.

FAQ

How is superannuation taxed in retirement in Australia?

Superannuation income streams paid from a taxed fund are generally tax-free for members aged 60 and over. Below age 60, the taxable component of super income is taxed at your marginal rate with a 15% tax offset.

What is provisional income and why does it matter?

Provisional income is your adjusted gross income plus non-taxable interest plus half your Social Security benefit. It determines what percentage of your Social Security benefit is subject to federal tax, with up to 85% taxable above the relevant threshold.

When do required minimum distributions start?

RMDs generally begin at age 73 for traditional retirement accounts in the United States. Roth accounts are not subject to RMDs during the original owner's lifetime, making them a useful tool for managing taxable income in later retirement.

What triggers an IRMAA surcharge on Medicare premiums?

IRMAA surcharges apply when your MAGI from two years prior exceeds the relevant threshold, starting at $109,000 for single filers in 2026. Crossing a threshold by even one dollar triggers the full surcharge for that income tier.

Can I reduce the tax on my pension income?

Yes. If your pension includes after-tax contributions, those amounts are returned tax-free and reduce your taxable income. Reviewing your annual tax statement and keeping records of after-tax contributions are the first steps to ensuring you are not overpaying tax on your pension payments.