TL;DR:

- Many Australians believe their super is entirely tax-free after age 60, but actual tax treatment depends on multiple factors, including fund phases and compliance. Withdrawals as lump sums or income streams have different tax implications based on age and contribution elements, with proper planning critical to minimizing taxes. Managing transfer balance caps, TRIS classifications, and asset timing is essential, as small oversights can lead to significant unexpected costs.

Many Australians heading into retirement carry a comforting but dangerously incomplete belief: that once you turn 60 and retire, your super is entirely tax-free. In reality, the tax treatment of your superannuation depends on a web of factors including your age, whether your fund holds taxed or untaxed elements, the phase your fund is in, and whether you've met minimum pension payment requirements. Missing a single compliance step or misjudging the timing of a phase transition can quietly cost you thousands of dollars each year. This article cuts through the complexity to give you a clear, actionable picture of how retirement taxation actually works.

Table of Contents

- How super withdrawals are taxed in retirement

- Understanding the retirement phase, transfer balance cap, and effective tax-free earnings

- Transition to Retirement (TRIS): Tax rules before and after retirement phase

- SMSFs and timing: Minimising tax and capital gains

- Common pitfalls and compliance traps in retirement tax planning

- Why compliance and timing matter more than most guides admit

- Get expert-powered strategies for your retirement tax planning

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Withdrawal method matters | Choosing lump sum versus income stream significantly impacts your tax bill in retirement. |

| Retirement phase is key | Moving super into retirement phase and respecting your transfer balance cap enables tax-free earnings within limits. |

| TRIS has special rules | Transition to Retirement Income Streams are not tax-free until they meet strict retirement phase conditions. |

| Timing saves tax | Planning the timing of asset sales and phase entry in SMSFs helps minimise capital gains tax. |

| Compliance avoids pitfalls | Keeping up with pension minimums and compliance avoids costly reclassification and unexpected tax bills. |

How super withdrawals are taxed in retirement

After clarifying the value of understanding your tax position, let's break down the taxation of super withdrawals.

Withdrawing super as a lump sum or as an income stream produces very different tax outcomes, and your age at the time of withdrawal matters enormously. The tax you pay depends on whether you withdraw as a lump sum or as a super income stream, and on your age and the tax components (taxable versus untaxed elements). Understanding this distinction is the first step toward building a tax-efficient retirement income.

Lump sum versus income stream: A quick comparison

| Withdrawal type | Under 60 | Age 60 and over |

|---|---|---|

| Lump sum (taxed element) | Taxed at marginal rate above low-rate cap | Generally tax-free |

| Lump sum (untaxed element) | Taxed at marginal rate | Up to $1.78 million tax-free, rest at 47% |

| Income stream (taxed element) | Taxed at marginal rate minus 15% offset | Tax-free |

| Income stream (untaxed element) | Taxed at marginal rate minus 10% offset | Taxed at marginal rate minus 10% offset |

The "taxed element" refers to super contributions and earnings that have already been taxed inside the fund at 15%. Most Australians in private sector funds hold entirely taxed elements. Untaxed elements are more common in some older government or defined benefit schemes, and they attract more tax even after age 60.

Key points to remember about super withdrawals:

- Your fund's accumulation phase earnings are taxed at 15%, whereas retirement phase earnings can be completely tax-free within limits.

- Income streams require you to draw a minimum percentage of your account balance each financial year (2% for those aged under 65, rising to 14% at age 95 and over).

- If you are under your preservation age (currently 60 for most people born after 1 July 1964), accessing super early requires meeting specific conditions of release.

- Planning your tax-free retirement income around the timing of turning 60 can meaningfully shift your tax position.

"Working backwards from what you want to spend in retirement is far more powerful than simply drawing down the maximum allowable. Structuring payments around tax thresholds and age milestones is where the real gains hide."

Pro Tip: Use an AlphaIQ super calculator to model your withdrawal scenarios across different ages and income levels. Seeing the after-tax numbers side by side makes timing decisions far clearer. You might also want to consider how much super is needed to retire before locking in a drawdown strategy.

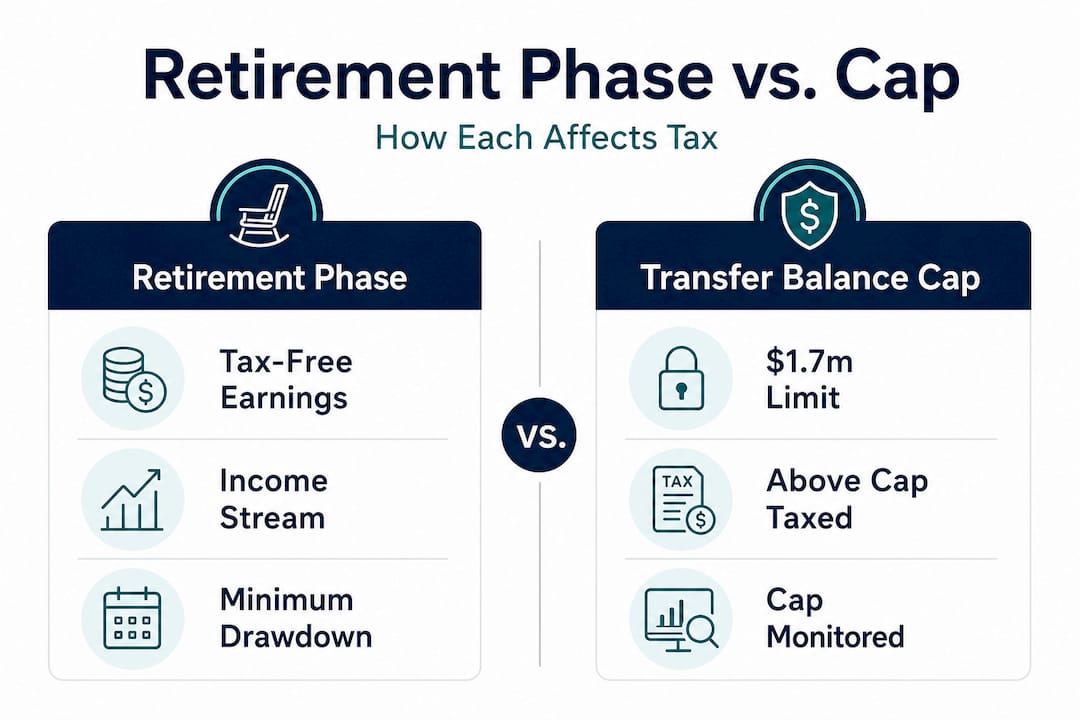

Understanding the retirement phase, transfer balance cap, and effective tax-free earnings

With the basics in mind, let's clarify how the retirement phase and caps can shape your tax position.

The "retirement phase" is a specific legal status your superannuation enters when you begin drawing an account-based pension or other qualifying income stream. Once in retirement phase, the earnings on assets supporting your pension can be entirely tax-free. However, this benefit is not unlimited.

The transfer balance cap is the cornerstone rule. Earnings on assets supporting pensions can be tax-free within limits, but this hinges on staying within your individual transfer balance cap when moving super into retirement phase. In 2026, the general transfer balance cap sits at $1.9 million, indexed in $100,000 increments based on the Consumer Price Index.

How the transfer balance cap affects your tax position

| Super balance transferred | Status | Tax on earnings |

|---|---|---|

| Below cap (e.g. $1.5 million) | Fully in retirement phase | Tax-free on all pension-supporting assets |

| At cap (e.g. $1.9 million) | Fully in retirement phase | Tax-free up to cap limit |

| Above cap (e.g. $2.3 million) | Excess must remain in accumulation | 15% tax on earnings for excess amount |

If you exceed your transfer balance cap, the ATO issues an excess transfer balance determination. You then face a tax on notional earnings calculated from when you first exceeded the cap. The longer you leave an excess unaddressed, the larger the bill.

Important considerations around the cap and retirement phase:

- Your personal transfer balance cap is set at the time you first move super into retirement phase. It does not increase just because the general cap increases, unless you've never used any of it.

- Amounts kept in the accumulation phase (above the cap) continue to be taxed at 15% on earnings.

- Retirement income planning that accounts for the cap from the outset avoids costly restructuring later.

- Roughly 0.5% of Australians have balances at or above $1.9 million, but the cap matters for a growing number of those with strong investment returns over a long accumulation phase.

Managing the boundary between accumulation and retirement phase is not a "set and forget" task. It requires active monitoring, especially in years of strong market growth when balances can shift unexpectedly.

Transition to Retirement (TRIS): Tax rules before and after retirement phase

Beyond ordinary account-based pensions, many Australians use Transition to Retirement Income Stream (TRIS) arrangements. This is where the tax implications can catch you out.

A TRIS allows you to access a limited income stream from your super once you reach preservation age (60 for most), even while you continue working. It sounds advantageous, and it can be, but only if you understand exactly when and how it becomes tax-effective.

TRIS differs from a full retirement phase pension in a critical way: if the TRIS is not in the retirement phase, earnings remain taxed at 15% inside the fund. The TRIS does not count towards your transfer balance cap until it moves into retirement phase. This catches many investors off guard.

The steps for a TRIS to access retirement-phase tax treatment are:

- You must meet a "nil cashing restriction" condition of release, such as retiring permanently, reaching age 65, or becoming permanently incapacitated.

- Once that condition is met, the TRIS moves into retirement phase and earnings on supporting assets become eligible for the Exempt Current Pension Income (ECPI) treatment.

- The TRIS then counts towards your transfer balance cap and the tax-free earnings status applies.

- Until that transition occurs, the fund continues paying 15% tax on earnings, even though you are drawing income from it.

TRIS tax status comparison

| TRIS stage | Earnings tax | Counts toward transfer balance cap |

|---|---|---|

| Before retirement phase | 15% tax on earnings | No |

| After retirement phase trigger | Eligible for ECPI (tax-free) | Yes |

Common mistakes with TRIS arrangements include assuming the income stream is immediately tax-free upon commencement, failing to notify the fund when a retirement condition is met, and drawing the maximum 10% limit without checking whether this triggers a reassessment of the income stream type. The tax rules for TRIS are more nuanced than most introductory guides acknowledge.

Pro Tip: Do not assume your TRIS is generating tax-free earnings inside the fund just because you've reached your preservation age. Confirm whether your fund has classified the income stream as being in retirement phase. If you've retired or turned 65, take action to formally trigger the transition.

SMSFs and timing: Minimising tax and capital gains

Now, let's look at how SMSFs offer flexibility but also risk if timing is off.

Self-managed super funds give trustees direct control over investment decisions, which creates significant opportunities for tax optimisation. The most powerful of these is timing when you sell assets relative to the fund's phase.

For SMSFs, timing of asset sales between accumulation and pension phase is a core tax optimisation lever. Capital gains can be taxed in accumulation phase at up to 10% (after the one-third discount for assets held over 12 months), but they may be entirely exempt when the fund is wholly in retirement phase through the ECPI exemption rules. This is subject to whether the fund uses the segregated or proportional method.

Optimal timing tax strategies for SMSF trustees include:

- Delaying asset sales until after the fund has fully transitioned to retirement phase, where ECPI applies to the entire fund.

- Segregating assets so those supporting pensions are clearly identified and can access full ECPI treatment without the proportional calculation.

- Reviewing unrealised gains annually to identify opportunities to realise gains in a low-tax year before transitioning to retirement phase.

- Timing pension commencement to the start of a financial year to maximise ECPI coverage for the full period.

- Keeping detailed records of when assets are allocated to pension versus accumulation accounts, as the ATO scrutinises SMSF ECPI claims closely.

"The tax edge in an SMSF is real, but it evaporates instantly if you sell assets in the wrong phase or fail to document your segregation methodology."

Pitfalls to watch for include missed pension minimums (which can reclassify your pension as having ceased), holding property or unlisted assets in a mixed-phase fund without a clear proportional allocation, and inadvertently triggering lump sum treatment by commuting pension payments incorrectly. For those with property in their SMSF, capital gains tips and strategies to optimise property for retirement are worth reviewing alongside fund-level planning.

Property investors combining SMSF and direct property holdings should also consider smart property investment strategies to ensure both streams are coordinated for maximum retirement efficiency.

Common pitfalls and compliance traps in retirement tax planning

Finally, to pull it all together: here are real-world traps even savvy investors miss.

Pension minimums are the single most frequent compliance failure in SMSFs. Missed minimum pension payments can re-categorise later payments as lump sums for tax purposes. TRIS arrangements can only access retirement-phase earnings treatment after specific conditions are met. A minor oversight at year-end can mean the income stream is treated as if it never existed for that financial year.

Meeting minimum standards is essential: if an SMSF provides income streams that meet minimum payment standards, pension payments are treated as super income stream benefits for income tax purposes. Missing those minimums can cause the income stream to be treated as stopped, with significant tax consequences.

"Missing a single compliance deadline can turn expected tax-free income into unexpected tax bills."

The top five errors and how to address them:

- Missing the annual pension minimum. Check your required minimum each year. Amounts vary by age. Set a calendar reminder for June each year to confirm payments have been made.

- Not notifying the fund when a TRIS condition of release is met. Formally notify your fund trustee in writing and have the documentation filed. This triggers the retirement phase status.

- Confusing lump sum and income stream tax treatment. Commuting a pension to take a lump sum changes the tax classification. Understand the difference before acting.

- Exceeding the transfer balance cap without a remediation plan. If you receive an excess determination, act promptly by commuting the excess back to accumulation to limit the notional earnings calculation.

- Selling assets in the wrong fund phase. If the fund is in accumulation, capital gains will be taxed. Ensure phase transitions are complete before triggering large asset sales.

If a mistake has already occurred, engage a specialist accountant immediately. The ATO has remediation pathways for certain errors, but they are time-sensitive. Reviewing SMSF versus industry super options is also worthwhile if the compliance burden of an SMSF begins to outweigh the tax benefits.

Why compliance and timing matter more than most guides admit

Having navigated the technical details, let's reflect on what most guides under-emphasise when it comes to retirement tax.

The prevailing narrative around super and retirement tax tends to focus on the destination: "once you're in retirement phase, earnings are tax-free." What that framing misses is the journey. The transitions, the timing windows, the annual obligations, and the phase classifications are where real-world outcomes are determined.

What we consistently see is that careful, well-intentioned investors make costly errors at exactly the moments when they feel most confident. Entering pension phase feels like crossing a finish line. But it is actually the start of an ongoing set of obligations that require at least as much attention as the accumulation years. One missed minimum pension payment, one forgotten TRIS notification, one asset sold in the wrong phase can undo years of careful planning.

The investors who get this right are not necessarily those with the largest balances. They are those who treat compliance as an active, recurring discipline rather than a box ticked once at retirement. Reviewing your fund's phase status, minimum payments, and transfer balance account at least annually is not overcaution. It is simply good financial management.

For those who want to go deeper, exploring advanced tax strategy lessons alongside regular compliance reviews creates the foundation for genuinely tax-efficient retirement income. The gap between what retirees expect to pay in tax and what they actually pay is almost always explained by timing and compliance, not by the rules themselves.

Pro Tip: Schedule an annual "retirement phase audit" each July. Confirm your pension minimum has been met, check your transfer balance account on the ATO portal, and verify that any TRIS has been correctly classified. Thirty minutes a year can prevent a very expensive surprise.

Get expert-powered strategies for your retirement tax planning

Ready to put this knowledge to work in your own portfolio?

Understanding the rules is only half the equation. Seeing how they apply to your specific balance, age, fund structure, and income needs is where the numbers become real. AlphaIQ is built for exactly this purpose.

The AlphaIQ wealth platform lets you model your retirement phase transitions, run scenario comparisons across accumulation and pension phases, and see the after-tax impact of different withdrawal strategies, all without the cost of ongoing advice. You can also use the debt recycling calculator to explore how pre-retirement debt strategies can maximise the assets you bring into retirement phase. Whether you are managing an SMSF, an industry fund, or a mix of both, AlphaIQ gives you the clarity to act with confidence.

Frequently asked questions

What is the tax treatment for lump sum super withdrawals after turning 60?

If your super is from a taxed fund and you are over 60, lump sum withdrawals are usually tax-free, but untaxed elements such as those from certain government schemes may still attract tax at your marginal rate.

Can I have more than one super income stream in retirement?

Yes, you can run multiple income streams, but the total amount moved into retirement phase cannot exceed your personal transfer balance cap, with earnings on retirement-phase accounts being tax-free within that limit.

When do TRIS earnings become tax-free?

Earnings only become tax-free once the TRIS enters retirement phase, which generally occurs when you turn 65 or satisfy a nil cashing restriction condition such as permanently retiring.

What happens if I miss the minimum pension payment in my SMSF?

Missing minimum pension payments can cause your income stream to be considered stopped for tax purposes, meaning later payments may be taxed as lump sums rather than as income stream benefits.

Are capital gains within my SMSF always tax-free in retirement?

No. Only gains on assets held in retirement phase are potentially exempt from capital gains through the ECPI rules, and mixed-phase funds or timing errors can result in gains being partially or fully taxed.