TL;DR:

- Net worth is assets minus liabilities, reflecting true financial health and retirement readiness.

- Regularly updating and accurately valuing assets and liabilities is essential for proper net worth calculation.

- Tracking net worth over time helps assess financial growth and guides smarter investment decisions.

Most Australians know roughly what's sitting in their bank account. Far fewer know their actual net worth. These are very different numbers, and confusing them can lead to some costly blind spots, particularly when you're building toward retirement. Your net worth is a complete financial snapshot: every asset you own, every debt you owe, and the gap between them. Understanding how to calculate it accurately gives you the foundation to make smarter investment decisions, set realistic retirement targets, and track whether your wealth is genuinely growing over time. This guide walks you through exactly how to do it.

Table of Contents

- What net worth really means and why it matters

- Breaking down the components: Assets and liabilities

- Step-by-step: How to accurately calculate your net worth

- Common pitfalls and mistakes in net worth calculation

- What most investors misunderstand about net worth

- Take control: Better net worth tracking with AlphaIQ

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Net worth defined | True net worth calculation considers all your assets minus all liabilities. |

| Holistic asset tracking | Including superannuation, property, shares, and debts ensures accuracy. |

| Actionable steps | A systematic process and regular reviews help you make smarter financial moves. |

| Avoid common pitfalls | Don’t overestimate assets or forget hidden debts in your calculation. |

What net worth really means and why it matters

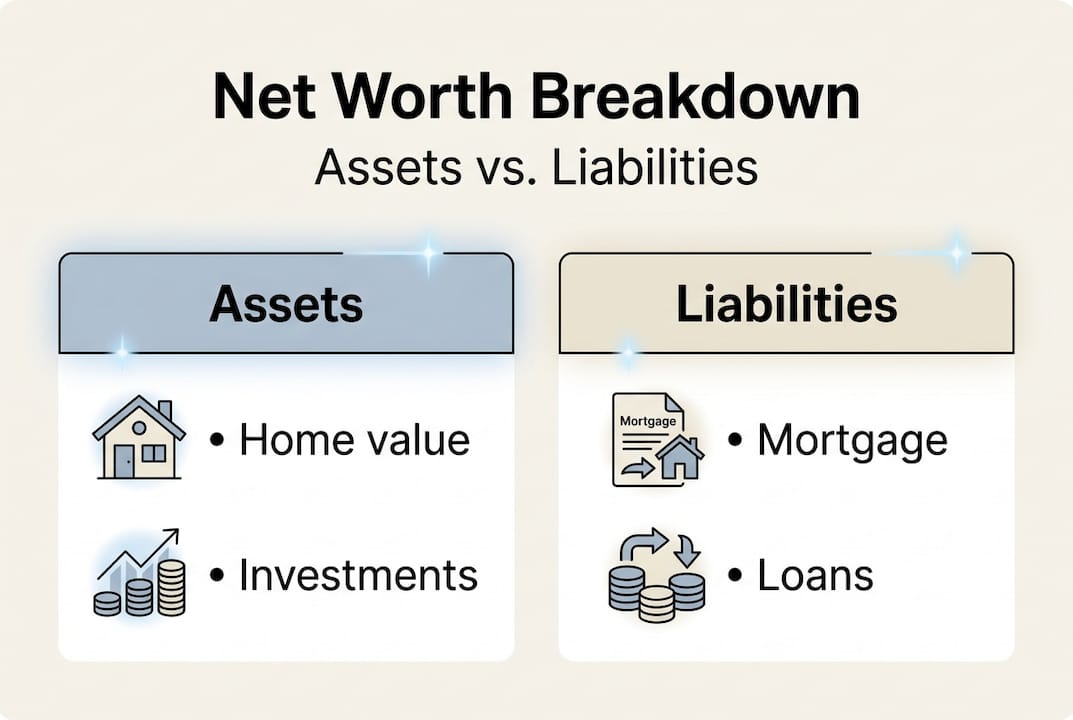

Net worth is the total value of assets minus liabilities, and that simple formula carries enormous weight for self-directed investors. Think of it as the financial equivalent of a progress report. It tells you not just where you are today, but whether the decisions you're making are actually moving you forward.

For investors aged 35 to 65, net worth is especially important because it connects directly to retirement readiness. You may have a strong income, a well-performing share portfolio, and a growing superannuation balance. But without knowing how these interact with your debts, you can't see the full picture. That's where net worth steps in.

Your assets in this calculation include:

- Property (your home, investment properties)

- Shares and managed funds

- Superannuation balances

- Cash and term deposits

- Vehicles and personal valuables

- Business interests

Your liabilities include:

- Home loan and investment property loans

- Credit card balances

- Personal loans and car finance

- HECS/HELP debts

- Tax liabilities owed to the ATO

Net worth is not a fixed number. It shifts with market movements, property values, interest rates, and life events like inheritance or divorce. Reviewing it regularly gives you an accurate, up-to-date financial position rather than a stale snapshot.

Many investors make the mistake of assuming a high income equals high net worth. It doesn't. High earners with heavy debt loads can have a surprisingly low net worth. Conversely, someone with a modest income who has been consistently investing and reducing debt over many years can build substantial wealth. The retirement calculators guide explains why this snapshot is foundational to any retirement planning process. MoneySmart net worth advice reinforces that tracking your position regularly is one of the most effective habits for long-term financial health.

Breaking down the components: Assets and liabilities

Understanding your complete asset and liability profile is essential to accurate net worth calculation. This is where many investors stumble, either by forgetting assets altogether or by applying outdated values to what they do include.

What counts as an asset?

| Asset type | Examples | Notes |

|---|---|---|

| Physical assets | Home, investment property, vehicle | Use current market value, not purchase price |

| Financial assets | Shares, ETFs, managed funds | Use current market price |

| Superannuation | All super fund balances | Include all accounts, including lost super |

| Cash and savings | Bank accounts, term deposits | Include all institutions |

| Business interests | Ownership stakes, goodwill | Use realistic, conservative valuations |

| Personal valuables | Jewellery, art, collectibles | Only if genuinely sellable at value |

What counts as a liability?

- Home loans and investment property mortgages

- Credit card balances (use the current outstanding balance)

- Personal loans and car finance

- HECS/HELP debt (check your current balance via myGov)

- Tax debts, including any outstanding ATO obligations

- Business loans or guarantees you've provided

A few points worth noting. Vehicles depreciate quickly, so resist using the purchase price. Check current resale values through a platform like RedBook. Super balances, particularly if you've had multiple employers, may be spread across several funds. ATO superannuation info outlines how to locate lost super and consolidate accounts. Optimising your assets is far easier when you have a complete picture of what you actually own.

Pro Tip: Build a simple spreadsheet with two columns: assets and liabilities. Update values at least once a year. Better still, use wealth intelligence tools that connect to your accounts and automate much of this process.

Step-by-step: How to accurately calculate your net worth

With assets and liabilities defined, it's time for the practical part. Here is a clear, repeatable process you can follow right now.

- List every asset you own. Include property, shares, super, savings, vehicles, and any other items of significant value. Be thorough. Missing an asset is just as distorting as missing a debt.

- Assign a current market value to each asset. Use recent property appraisals, current share prices, and up-to-date super statements. Avoid using purchase prices or wishful estimates.

- List every outstanding liability. Pull out your latest mortgage statement, check your credit card balance, log in to myGov for HECS/HELP, and note any other debts.

- Total your assets, then total your liabilities.

- Subtract total liabilities from total assets. The result is your net worth.

Here's a sample calculation for a typical Australian household:

| Item | Value |

|---|---|

| Family home (current market value) | $950,000 |

| Investment property (current market value) | $620,000 |

| Share portfolio | $85,000 |

| Superannuation (combined) | $310,000 |

| Savings and term deposits | $45,000 |

| Vehicle | $22,000 |

| Total assets | $2,032,000 |

| Home loan outstanding | $480,000 |

| Investment property loan | $390,000 |

| Credit card balance | $4,500 |

| HECS/HELP debt | $12,000 |

| Total liabilities | $886,500 |

| Net worth | $1,145,500 |

Using digital tools can streamline the calculation process considerably, reducing the risk of errors and saving you time. Personal wealth platforms can integrate with your accounts and update values automatically. The Canstar net worth guide also provides useful context for benchmarking your position.

Pro Tip: Recalculate your net worth at least once a year and always after major life events such as buying property, receiving an inheritance, or changing employment.

Common pitfalls and mistakes in net worth calculation

Even with the right methods, people make common errors that can distort their financial picture. Knowing what to watch for helps you avoid them.

The most frequent mistakes include:

- Overvaluing property. Many investors use their purchase price or an optimistic estimate rather than a current market appraisal. Property values shift, and using an inflated figure gives you a false sense of wealth.

- Forgetting smaller debts. Tax debts, family loans, and HECS/HELP balances are easy to overlook. They are still liabilities and must be included.

- Missing super accounts. Many Australians forget to include superannuation or underestimate their liabilities, especially when they have accounts sitting with former employers. Search for lost super via the ATO portal.

- Using outdated values. A share portfolio or investment property valued 18 months ago is not an accurate number today. Markets move, and your figures should reflect that.

- Ignoring depreciation on vehicles. A car worth $40,000 when purchased may now be worth $25,000. Always use current resale value.

According to ABS household wealth data, Australian household wealth varies significantly by age and asset composition, with many households concentrated in property and superannuation. This makes it even more important to accurately track both, since errors in either category have an outsized impact on your net worth figure.

Consistently using wealth tracking platforms reduces these errors materially. If you're also working toward a specific financial independence target, understanding how net worth feeds into your FI number calculation is a logical next step.

What most investors misunderstand about net worth

Here's a perspective worth sitting with. Most investors treat net worth as a score. They calculate it once, feel good or bad about the result, and then move on. That's the wrong way to use it.

Net worth is most powerful as a trend, not a figure. A net worth that grows consistently by $50,000 per year tells you far more than a static number of $800,000. The trajectory reveals whether your decisions are working: your investment choices, debt reduction strategy, and spending habits.

We've seen investors with high net worth figures who are actually in a fragile position because their wealth is illiquid, concentrated in one asset, or built on debt that's barely being managed. The number looked good. The underlying structure didn't.

True financial clarity comes from tax-aware wealth building combined with regular net worth reviews. When you track your net worth over time and tie it to specific decisions, you stop guessing and start optimising. The goal isn't just a big number. It's a growing, well-structured number that you understand and can act on.

Take control: Better net worth tracking with AlphaIQ

Now that you have a clear framework for calculating your net worth, the next step is making it easy to maintain that clarity over time.

AlphaIQ is built specifically for self-directed Australian investors who want to model and optimise their financial position without paying for ongoing financial advice. The platform brings your investments, superannuation, property, and debt into one place, so your net worth is always current and always useful. Use the superannuation calculator to project your super balance forward, or explore debt recycling tools to see how restructuring your debt could lift your net worth more quickly. Start with the AlphaIQ wealth platform and see your financial position with the clarity it deserves.

Frequently asked questions

What is included in net worth?

Net worth is assets minus liabilities, covering everything from property and investments to superannuation and savings, less any mortgages, loans, and credit card balances.

How often should I calculate my net worth?

Review net worth regularly, ideally once a year or after any significant financial change such as buying property, paying off a major debt, or receiving a windfall.

Do I need to include superannuation in my net worth?

Yes. Superannuation forms a key part of your asset base in Australia and should always be included, particularly as balances grow significantly in the years approaching retirement.

What is a common mistake investors make when calculating net worth?

Investors often overvalue assets or omit debts, particularly property values that haven't been updated to reflect current market conditions or smaller liabilities like tax debts and personal loans.