TL;DR:

- Superannuation in Australia is a mandatory savings system reducing reliance on the Age Pension and providing retirement income. Access depends on reaching preservation age, with structured drawdowns and income streams being key to financial security. Recent changes, like the 12% contribution rate and flexible planning tools, enhance retirees' ability to optimise their super long-term.

Superannuation is Australia's compulsory savings system, designed to accumulate funds during your working life and deliver a primary source of income in retirement. The role of superannuation in retirement extends well beyond simply having a nest egg. It determines how much you can spend each year, how long your money lasts, and how much you rely on the Age Pension. For Australians aged 45 to 65, understanding how super works, when you can access it, and how to draw it down efficiently is the difference between a retirement that feels secure and one that feels uncertain.

What is the role of superannuation in retirement income?

Superannuation was introduced to reduce reliance on the publicly funded Age Pension by shifting retirement income responsibility toward individual savings. That original intent still shapes how the system works today. Your employer contributes a percentage of your salary into a super fund throughout your career, and those funds grow in a tax-advantaged environment until you retire.

The Superannuation Guarantee rate reached 12% as of July 2025, meaning more of your working income is now being set aside than at any previous point in the system's history. This matters for anyone aged 45 to 65 because even a decade of contributions at this rate can meaningfully change your retirement balance. Super does not replace the Age Pension entirely for most Australians, but it reduces the amount you need from it and gives you far greater control over your income timing and spending.

The importance of superannuation becomes clearest when you model retirement income across multiple decades. A couple retiring at 65 today may need their savings to last 25 to 30 years. Super, structured well, is the primary tool for making that work.

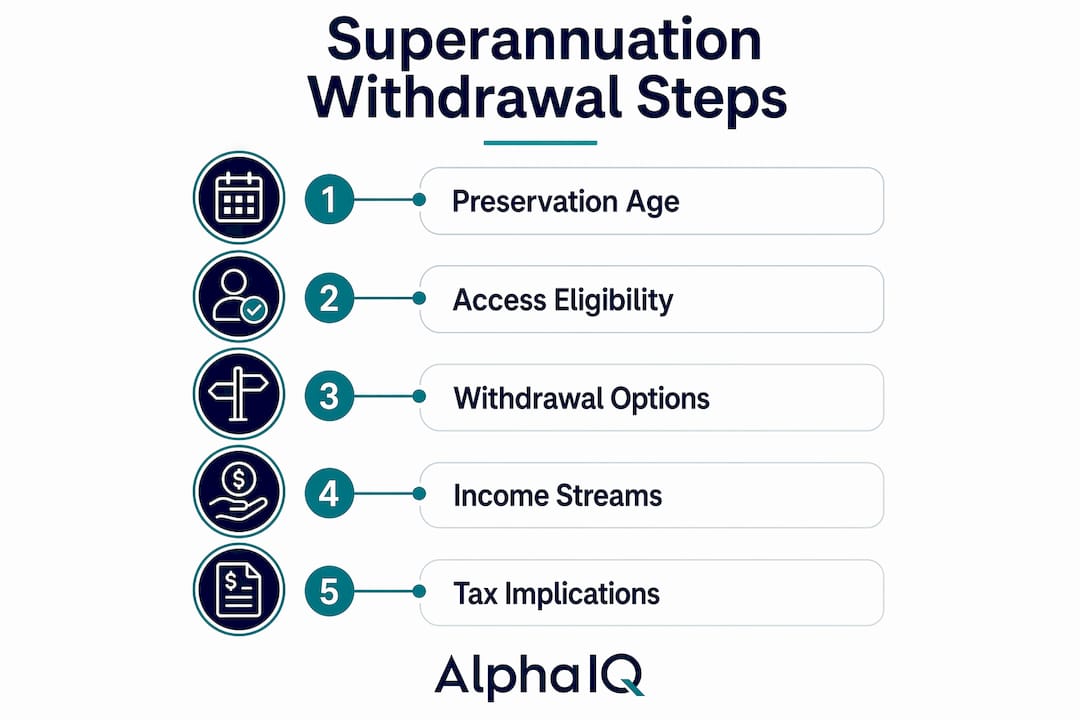

How and when can you access your superannuation?

Accessing your super depends on reaching your preservation age, which is separate from the Age Pension age of 67. Your preservation age is determined by your birth year and generally falls between 55 and 60. If you were born after 30 June 1964, your preservation age is 60.

Reaching preservation age does not automatically unlock your super. You also need to meet a condition of release, the most common being retirement or reaching age 65. Here is how the key access milestones work:

- Preservation age (60 for most): You can begin a Transition to Retirement Income Stream (TRIS) while still working, or access your super fully if you have retired.

- Age 65: You can access your super regardless of whether you have retired, with no conditions attached.

- Age 67: Age Pension eligibility begins, subject to income and assets tests.

The gap between preservation age and Age Pension eligibility is where planning becomes critical. If you retire at 62, you have five years before the Age Pension becomes available. Your super needs to cover that period without being drawn down so aggressively that it undermines your long-term income.

Pro Tip: If you retire before 67, model your super drawdown carefully across the gap years. Drawing too heavily early can reduce your balance just as Age Pension entitlements kick in, limiting the complementary income effect.

Lump sum or income stream: which withdrawal approach suits you?

Retirement withdrawals can be taken as a lump sum, a regular income stream, or a combination of both. Each approach carries different tax and cashflow implications, and the right choice depends on your spending needs, tax position, and how long you expect your retirement to last.

| Withdrawal type | Tax treatment | Cashflow | Best suited to |

|---|---|---|---|

| Lump sum | Tax-free after age 60 (taxed component rules apply under 60) | One-off, flexible | Paying off debt or large expenses |

| Account-based income stream | Tax-free after age 60; earnings in retirement phase tax-free | Regular, structured | Ongoing living expenses |

| TRIS (Transition to Retirement) | Earnings taxed at 15%; drawdown capped at 10% of balance | Flexible while working | Phasing into retirement |

The account-based income stream is the most widely used product in the retirement phase. You transfer your super balance into a retirement phase account, and the fund pays you a regular income. Earnings on assets supporting that income stream are tax-free, which is one of the most significant tax advantages available to Australian retirees.

Key considerations when choosing your withdrawal structure:

- The transfer balance cap (currently $1.9 million) limits how much you can move into the tax-free retirement phase.

- Minimum annual drawdown rates apply to income streams, starting at 4% for those aged 60 to 64 and rising with age.

- A TRIS allows phased access from preservation age while you continue working, but earnings remain taxed at 15% until you fully retire.

Pro Tip: Taking a partial lump sum to clear a mortgage at retirement, then living off an account-based income stream, is a common and tax-effective strategy. Run the numbers on both before committing to one approach.

How does super fit with the Age Pension and other income sources?

Superannuation and retirement savings work best when planned alongside the Age Pension and any personal savings or investments you hold. Most Australians will draw on a combination of these sources, and the interaction between them affects both your tax position and your total income.

The Age Pension is means-tested, which means your super balance and income stream payments can reduce your entitlement. This is not necessarily a problem. A well-structured super drawdown can actually complement the Age Pension by tapering your super income as your balance falls, allowing Age Pension payments to increase over time.

Practical ways to integrate multiple income sources for sustainable retirement cashflow include:

- Drawing on super between preservation age and 67 to bridge the gap before Age Pension eligibility.

- Holding personal savings or term deposits as a liquidity buffer for unexpected expenses, rather than drawing extra from super.

- Timing super withdrawals to manage your assessable income and minimise the impact on Age Pension entitlements.

- Considering whether a spouse's super balance and income affect your combined means test position.

The broader point is that retirement income planning is not a single-product exercise. Super is the centrepiece, but it works alongside other assets and entitlements. Modelling all of these together gives you a far clearer picture of what you can actually afford to spend each year.

What recent changes affect your super retirement strategy?

The superannuation system is not static, and several recent shifts directly affect how Australians aged 45 to 65 should approach their planning. Longevity risk and economic uncertainty are now central concerns for retirement system designers and individual retirees alike.

The most significant recent changes include:

- Superannuation Guarantee at 12%: From July 2025, employer contributions reached 12%, the highest rate in the system's history. For those still working, this accelerates balance growth in the final years before retirement.

- Longevity risk: Australians are living longer, and a retirement that begins at 62 or 65 may need to fund 25 to 30 years of spending. This demands a drawdown strategy that preserves capital in the early years.

- Inflation and market volatility: Both erode the real value of your super balance. A fund invested entirely in cash or low-growth assets may not keep pace with living costs over a 25-year retirement.

- Digital planning tools: Personalised modelling tools now allow retirees to simulate different drawdown rates, investment scenarios, and income combinations without paying for ongoing financial advice.

Key insight: Ageing Australians face longevity risk and inflation volatility simultaneously, which means a fixed drawdown rate set at retirement is unlikely to remain appropriate for the full retirement period. Reviewing your strategy every two to three years is not optional. It is necessary.

Choice in fund selection and investment options is a defining feature of Australia's system, and that choice now extends to sophisticated income stream products and digital planning support. Using these tools well is increasingly part of what separates a comfortable retirement from a constrained one.

Practical steps to optimise your super before and during retirement

Getting the most from your super requires deliberate decisions across both the accumulation phase (while you are still working) and the decumulation phase (once you start drawing down). Here are the steps that make the most difference for Australians aged 45 to 65:

- Consolidate multiple super accounts. Duplicate accounts mean duplicate fees. Find and merge lost or inactive accounts through myGov before retirement to avoid eroding your balance unnecessarily.

- Review your fund's investment options and fees. A fund charging 1.5% annually versus 0.5% annually can cost tens of thousands of dollars over a decade. Compare performance net of fees, not gross returns.

- Model your drawdown rate before you retire. Working backwards from what you want to spend each year tells you how long your balance will last at different drawdown rates. Use a super projection calculator to run these scenarios with your actual numbers.

- Consider a TRIS if you are winding down work gradually. A Transition to Retirement Income Stream lets you supplement a reduced salary with super income, making a phased retirement financially viable.

- Plan your tax position across the transition. Moving assets into the retirement phase at the right time, and in the right amounts, affects both your tax bill and your Age Pension entitlement. Retirement tax strategies are worth understanding before you make irreversible decisions.

- Revisit your strategy regularly. Markets move, legislation changes, and your spending needs shift. A plan built at 60 may need updating at 65 and again at 70.

Pro Tip: If you are within five years of retirement, consider making voluntary concessional contributions to boost your super balance while reducing your taxable income. The annual concessional cap is $30,000 for 2025-26, and unused cap amounts from prior years may be carried forward.

Key takeaways

Superannuation is the primary self-funded income source for Australian retirees, and its effectiveness depends on when you access it, how you draw it down, and how well it integrates with the Age Pension and other savings.

| Point | Details |

|---|---|

| Preservation age governs access | Most Australians born after June 1964 can access super from age 60, not 67. |

| Income streams beat lump sums for longevity | Account-based income streams provide tax-free income and preserve capital more effectively than lump sum withdrawals. |

| Super and Age Pension interact | Drawing down super strategically can increase Age Pension entitlements as your balance reduces over time. |

| Recent policy changes matter | The Superannuation Guarantee reached 12% in July 2025, accelerating balance growth for those still working. |

| Modelling is non-negotiable | Running personalised drawdown scenarios before retirement prevents both under-spending and running out of money. |

What I have learned about super and retirement planning

After working closely with retirement income data and the decisions Australians make around their super, one pattern stands out clearly. Many retirees default to minimum drawdowns despite having the capacity to spend more and live better. The fear of running out of money is real, but it often leads to unnecessary self-deprivation in the early, healthiest years of retirement.

The uncomfortable truth is that most people do not plan their decumulation phase with anywhere near the same rigour they apply to accumulation. They spend decades focused on growing their super balance, then reach retirement without a clear framework for spending it. The result is either anxiety-driven under-drawing or, in some cases, poorly timed lump sum withdrawals that trigger unnecessary tax.

What actually works is modelling your retirement income across multiple scenarios before you stop working. Not once, but repeatedly, as your circumstances change. The interaction between super, the Age Pension, and personal savings is complex enough that a single static plan will not hold for 25 years. The retirees I see managing this well are the ones who treat their income strategy as a living document, not a one-time decision.

Technology has genuinely changed what is possible here. Personalised modelling tools now give self-directed retirees access to the kind of scenario analysis that previously required a financial planner. That does not mean advice is irrelevant. It means you can arrive at an advice conversation far better informed, and make decisions with real confidence rather than guesswork.

— Jonathan

Plan your retirement with Alphaiq's super tools

Knowing the theory is one thing. Seeing how your actual super balance, drawdown rate, and income sources interact over 20 or 30 years is where real clarity comes from.

Alphaiq's Super Calculator lets you model your retirement projections with your real numbers, including super balance growth, drawdown scenarios, Age Pension interaction, and tax implications. The AI Wealth Intelligence platform goes further, combining super modelling with investment, property, and income stream analysis in one place. For Australians aged 45 to 65 who want to make confident, informed decisions about their retirement without paying for ongoing advice, Alphaiq gives you the tools to do exactly that.

FAQ

What is the preservation age for accessing super in Australia?

For most Australians born after 30 June 1964, the preservation age is 60. This is the earliest point at which you can access your super, provided you have also met a condition of release such as retiring from the workforce.

How does superannuation affect Age Pension eligibility?

Your super balance and income stream payments are assessed under the Age Pension income and assets tests. A higher super balance or drawdown amount can reduce your Age Pension entitlement, but strategic drawdown planning can help manage this interaction over time.

What is a Transition to Retirement Income Stream (TRIS)?

A TRIS allows you to access super income from preservation age while you are still working. Drawdowns are capped at 10% of your balance annually, and earnings remain taxed at 15% until you fully retire and move into the retirement phase.

Is super tax-free in retirement?

Super income stream payments are generally tax-free for Australians aged 60 and over. Earnings on assets supporting a retirement phase account are also tax-free, making the retirement phase one of the most tax-effective structures available to Australian investors.

How much super do I need to retire comfortably in Australia?

The Association of Superannuation Funds of Australia (ASFA) estimates a couple needs approximately $690,000 in super to fund a comfortable retirement lifestyle, alongside a part Age Pension. A single person requires around $595,000. These figures assume retirement at 67 and spending across a roughly 25-year retirement period.