TL;DR:

- Financial scenario planning is a structured process that analyzes multiple plausible futures to guide investment and strategic decisions. It involves defining key uncertainties, creating coherent scenarios, modeling financial impacts, and establishing decision triggers. Limiting scenarios to three to five and regularly updating them ensures effective, resilient planning aligned with real-world changes.

The financial scenario planning process is a structured method for building and analysing multiple plausible futures to inform investment decisions, business strategy, and contingency planning. Unlike a single-point forecast, it asks "what if?" across several coherent futures simultaneously, then maps the financial consequences of each. For self-directed investors and business leaders alike, this discipline converts uncertainty from a threat into a manageable input. Frameworks like Peter Schwartz's 8-step method and Shell's 2x2 matrix have shaped how organisations approach this work for decades, and today's financial scenario analysis platforms make the same rigour accessible to individuals managing their own wealth.

What are the essential steps in the financial scenario planning process?

A well-structured scenario process begins with a defined focal decision and a clear time horizon, typically three years for most planning contexts. Without this anchor, scenario work drifts into abstract storytelling rather than practical financial preparation. Every subsequent step flows from that initial clarity.

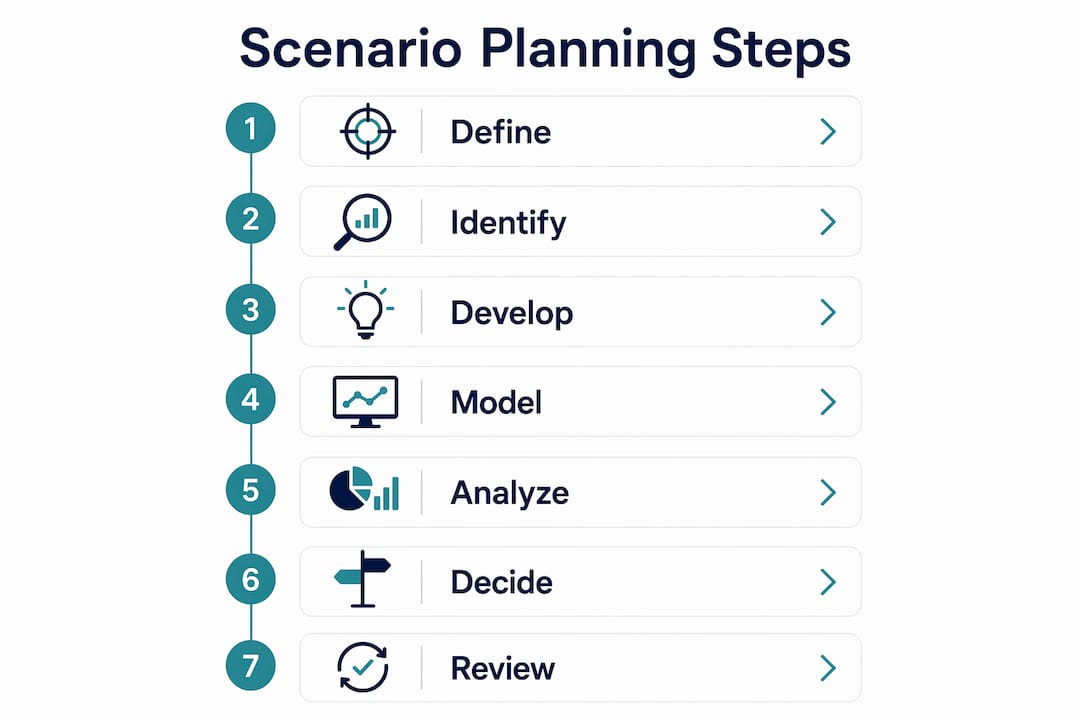

Follow these six steps to execute the process end to end:

-

Define the focal decision and time horizon. Identify the specific decision or strategic question driving the exercise. For an individual investor, this might be "Should I increase my property allocation before retirement?" For a business leader, it could be "How do we plan capital expenditure given interest rate uncertainty?" A three-year horizon suits most mid-term planning needs.

-

Identify and rank key uncertainties. Use a PESTLE analysis (Political, Economic, Social, Technological, Legal, Environmental) to surface the external forces most likely to affect your financial outcomes. Then apply a tornado diagram to rank variables by their potential impact on your key financial metric, whether that is net worth, operating cash flow, or retirement income.

-

Develop 2 to 4 internally consistent scenario narratives. Each scenario must tell a coherent story where all assumptions fit together logically. A scenario that combines high inflation with low interest rates, for example, is internally inconsistent and will produce unreliable outputs. Internally consistent scenarios improve credibility and ensure your quantitative outputs support sound decisions.

-

Quantify impacts across P&L and cash flow. Run each scenario through an integrated financial model covering revenue, costs, working capital, and debt. Pay particular attention to cash flow. A 10% revenue decline might appear tolerable on a profit and loss statement but prove fatal on cash flow depending on working capital timing. This is the step most individual investors underestimate.

-

Analyse strategic implications. For each scenario, ask what your current strategy achieves, where it falls short, and what adjustments would improve outcomes. This is where scenario planning connects directly to your investment portfolio decisions and business contingency planning.

-

Set monitoring signposts and decision triggers. Assign specific, observable leading indicators to each scenario. Define in advance what action you will take if those indicators are reached. This step converts the exercise from an intellectual one into an operational tool.

Pro Tip: Keep your scenario set to three or four narratives maximum. More than four scenarios tends to overwhelm decision-making rather than improve it, and the analytical value diminishes quickly beyond that number.

How does scenario planning differ from forecasting and stress testing?

Many investors and finance professionals use the terms "scenario planning," "sensitivity analysis," "forecasting," and "stress testing" interchangeably. They are not the same, and using the wrong method for the wrong question produces misleading results.

Here is how each technique differs in purpose and application:

- Single-point forecasting produces one expected outcome based on the most likely path. It is useful for budgeting and short-term operational planning but fails when the future is genuinely uncertain across multiple dimensions.

- Sensitivity analysis changes one variable at a time while holding all others constant. It is valuable for model validation and understanding which drivers matter most, but it does not capture how multiple variables interact simultaneously.

- Stress testing applies severe but plausible shocks to assess resilience. The Bank of England's 2024 stress test, for instance, modelled inflation at 12% and the Bank Rate at 9% over five years. Stress tests are not predictions. They are resilience assessments, and that mindset is equally valuable for business leaders.

- Scenario planning changes multiple variables simultaneously across several coherent futures. It bridges static budgeting and dynamic risk management, testing strategic resilience to volatility rather than predicting a single outcome.

The most common mistake is treating scenario planning as a more elaborate forecast. It is not. A forecast asks "what will happen?" Scenario planning asks "what should we do if this happens, or that happens, or the other thing happens?" The outputs are fundamentally different.

For Australian investors managing superannuation, property, and investment portfolios simultaneously, scenario planning is the most appropriate technique because your financial outcomes depend on several interacting variables: interest rates, property values, share market returns, and tax policy. No single-point forecast captures that complexity honestly.

What tools and methods support effective financial scenario models?

The quality of your scenario analysis depends heavily on the modelling approach you use. A model that only tracks profit misses the cash flow dynamics that determine whether a business survives or an investor meets their retirement income target.

| Modelling approach | Best suited for | Key limitation |

|---|---|---|

| Integrated three-statement model | Business leaders, complex portfolios | Requires financial modelling skill |

| Driver-based Excel model | Mid-market businesses, self-directed investors | Manual updates needed |

| Financial scenario analysis platforms | Individual investors, rapid scenario comparison | May lack customisation depth |

| Shell 2x2 matrix | Strategic narrative development | Qualitative, not quantitative |

Building integrated three-statement models that align revenues, costs, working capital, and debt schedules is the gold standard for credible financial scenario analysis. For most mid-market businesses and individual investors, a well-structured Excel model with 5 to 10 key drivers covers the majority of planning needs effectively.

Peter Schwartz's 8-step method adds rigour to the narrative side of scenario development. It moves from identifying the focal question through to selecting scenario logics, fleshing out scenarios, and identifying implications. The Shell 2x2 matrix then plots scenarios across two critical uncertainties to create four distinct quadrants, each representing a different future state.

Pro Tip: Limit your driver-based model to 5 to 10 key variables. More than that creates a false sense of precision and makes the model harder to update when conditions change. Focus on the variables that genuinely move your financial outcomes.

For individual investors using personal finance modelling approaches, the same principles apply. Identify your three to five most important financial drivers, such as superannuation contribution rate, property capital growth, and drawdown rate in retirement, then model each scenario consistently across all of them.

How do you link scenario planning to real investment decisions?

Scenario analysis only earns its place in your planning process when it changes what you actually do. The connection between scenario outputs and concrete decisions is where most planning exercises break down.

The most effective mechanism is the pre-committed decision trigger. Pre-committing leading indicators and decision triggers enables organisations to react three to four weeks faster than competitors without that discipline. For an individual investor, this translates directly into faster, less emotional responses to market shifts.

Practical examples of decision triggers include:

- Hiring freeze trigger: If monthly revenue falls below a defined threshold for two consecutive months, freeze all discretionary hiring immediately.

- Portfolio rebalancing trigger: If the share market falls more than 20% from its peak, rebalance the portfolio toward defensive assets according to a pre-agreed allocation.

- Superannuation contribution trigger: If after-tax income exceeds a set level for two consecutive quarters, increase voluntary super contributions to the concessional cap.

- Liquidity trigger: If cash reserves fall below three months of operating expenses, pause capital expenditure and activate the pre-agreed cost reduction plan.

The table below illustrates how scenario outcomes translate into specific financial responses:

| Scenario | Key indicator | Pre-agreed response |

|---|---|---|

| Upside growth | Revenue 15% above forecast | Accelerate capital investment, increase super contributions |

| Base case | Revenue within 5% of forecast | Maintain current strategy, review quarterly |

| Downside | Revenue 10% below forecast | Reduce discretionary spend, review working capital |

| Stress case | Revenue 25% below forecast | Activate contingency plan, draw on credit facility |

Integrating these triggers into your regular budgeting and rolling forecast cycle means scenario planning becomes a living discipline rather than an annual document. Understanding investment risk in this context means knowing in advance which signals matter and what you will do when they appear.

What pitfalls should you avoid in scenario planning?

The most common failure in scenario planning is producing scenarios that look rigorous but never influence a single decision. Scenarios yield greatest value when linked to decision triggers and governance structures. Without those links, the work becomes an academic exercise.

Watch for these specific pitfalls:

- Too many scenarios. Best practice sits at 3 to 5 scenarios with assigned probabilities: a base case at 50 to 60%, an upside and downside each at 15 to 20%, and an optional stress case at around 5%. More than five scenarios overwhelms leadership and dilutes focus.

- Internally inconsistent assumptions. Each scenario must hold together as a coherent story. Mixing incompatible assumptions, such as high consumer spending alongside high unemployment, produces outputs that cannot be trusted.

- Treating scenarios as predictions. Regulators emphasise that stress test scenarios are for resilience learning, not forecasts. The same mindset applies to business and investment scenario planning. You are preparing responses, not predicting outcomes.

- Neglecting cash flow. The hardest operational challenge is translating scenario outcomes into cash-focused survival maps. P&L-only models miss the liquidity risks that can determine whether a business or investment portfolio survives a downturn.

- Siloed development. Scenarios built only by the finance team miss operational realities. Involve people from strategy, operations, and investment management to stress-test assumptions from multiple angles.

Pro Tip: Schedule a scenario review every six months at minimum, and immediately after any major market event or policy change. Scenarios built in 2024 may not reflect the interest rate and inflation environment of 2026 without updating.

Key takeaways

Effective financial scenario planning requires integrating decision triggers, cash flow modelling, and regular reviews to convert analysis into real strategic advantage.

| Point | Details |

|---|---|

| Anchor every scenario to a decision | Define the focal question first; scenarios without a decision context produce no actionable output. |

| Cash flow matters more than profit | A 10% revenue decline can be manageable on P&L but critical on cash flow depending on working capital. |

| Keep scenarios to 3 to 5 | More than five scenarios overwhelms decision-making and reduces the quality of strategic response. |

| Pre-commit your triggers | Decision triggers set in advance enable faster, less emotional responses to changing conditions. |

| Review regularly | Scenarios built without regular updates lose relevance as market conditions shift. |

Why decision triggers are the part most people skip

After working through financial scenario planning with investors and business leaders across different contexts, the pattern I see most often is this: the scenario narratives are well-crafted, the models are technically sound, and then the whole exercise sits in a folder until the next annual planning cycle. The decision triggers never get written. That is where the value is lost.

The scenarios themselves are not the product. The pre-agreed responses are the product. When markets move or a business metric slips, you do not want to be convening a meeting to decide what to do. You want to be executing a plan you already agreed on when you were thinking clearly, not under pressure.

I have also noticed that cash flow is consistently underweighted in scenario models, particularly among individual investors. People model their superannuation balance or their property equity, but they do not model the timing of cash flows in retirement or the liquidity impact of a market drawdown on their drawdown rate. That gap can be the difference between a comfortable retirement and a forced asset sale at the wrong time.

The other thing worth saying plainly: scenario planning is not a one-time exercise. The economic environment in Australia in 2026 looks materially different from 2022 or even 2024. Interest rates, inflation, superannuation policy, and property market dynamics have all shifted. If your scenarios have not been updated to reflect that, they are not protecting you. They are giving you false confidence.

The investors and business leaders who get the most from this process treat it as a quarterly habit, not an annual report. That shift in cadence changes everything.

— Jonathan

Model your retirement scenarios with Alphaiq

Scenario planning principles apply directly to retirement projections, and Alphaiq's Super Calculator for 2025 to 2026 puts that capability in your hands without the cost of ongoing financial advice.

The calculator lets you model your superannuation balance across multiple contribution and return scenarios, factoring in concessional contributions, employer contributions, and projected drawdown rates. You can adjust key variables to see how different futures affect your retirement income, which is exactly the driver-based modelling approach described in this article. For self-directed investors aged 35 to 65 who want real numbers behind their retirement planning, it is a practical starting point for building your own scenario-based financial picture.

FAQ

What is the financial scenario planning process?

The financial scenario planning process is a structured method for developing and analysing multiple plausible futures to inform financial decisions. It involves defining a focal question, identifying key uncertainties, building coherent scenarios, modelling financial impacts, and setting decision triggers.

How many scenarios should you build?

Best practice is three to five scenarios, typically a base case, an upside, a downside, and an optional stress case. More than five scenarios tends to overwhelm decision-making without adding proportional analytical value.

How does scenario planning differ from forecasting?

Forecasting produces a single expected outcome, while scenario planning explores multiple simultaneous variable changes across several coherent futures. Scenario planning tests strategic resilience rather than predicting one outcome.

Why is cash flow more important than profit in scenario models?

A revenue decline that appears manageable on a profit and loss statement can be critical on cash flow depending on working capital timing. Cash flow models reveal liquidity risks that P&L-only analysis consistently misses.

How often should you update your financial scenarios?

Scenarios should be reviewed at least every six months and immediately after significant market events or policy changes. Scenarios that are not updated regularly lose relevance and can produce false confidence in outdated assumptions.