TL;DR:

- Tax planning in Australia involves legally reducing taxable income through strategies like timing income and deductions, maximising super contributions, and managing capital gains. Effective planning requires year-round decisions, modelling, and working with advisers, especially ahead of 2027 CGT rule changes. Alphaiq offers tools to simulate the impact of these strategies before making investment decisions.

Tax optimisation is the practice of legally reducing your taxable income to improve your after-tax financial position. For Australians aged 35–65, this optimise tax position guide covers the strategies that matter most: timing income and deductions, maximising superannuation contributions, managing capital gains, and structuring investments for tax efficiency. The Australian Taxation Office (ATO) sets the rules; your job is to work within them as deliberately as possible. Proactive year-round planning produces far better outcomes than a last-minute scramble before 30 june.

Which tax optimisation strategies provide the greatest benefit?

The most effective tax planning strategies reduce your taxable income before the financial year closes. Each of the following techniques is legal, ATO-compliant, and available to most Australian taxpayers.

- Prepay deductible investment loan interest. You can prepay up to 12 months of deductible investment loan interest before 30 june, provided the service period ends before 30 june the following year. This shifts a future expense into the current financial year, reducing your taxable income now.

- Defer income where possible. If you expect lower income next financial year, delay invoicing or asset sales until after 30 june. The deferred income is then taxed at a lower marginal rate.

- Make concessional superannuation contributions. Contributions to super are taxed at 15% inside the fund, well below most marginal tax rates. This is one of the most powerful deductions available to Australians in the 35–65 age bracket.

- Claim gifts to Deductible Gift Recipients (DGRs). Donations to ATO-registered DGRs of $2 or more are fully deductible. Timing a larger donation before 30 june can meaningfully reduce your taxable income.

- Manage Medicare Levy Surcharge (MLS) exposure. The MLS applies if your income exceeds the relevant threshold and you do not hold private hospital cover. Prepaying deductible expenses is most beneficial near income thresholds such as the MLS trigger; below those thresholds, the cash flow cost may outweigh the tax saving.

Pro Tip: Review your income estimate in may each year. Knowing where you sit relative to the MLS threshold, HECS repayment triggers, and your marginal rate gives you time to act before 30 june.

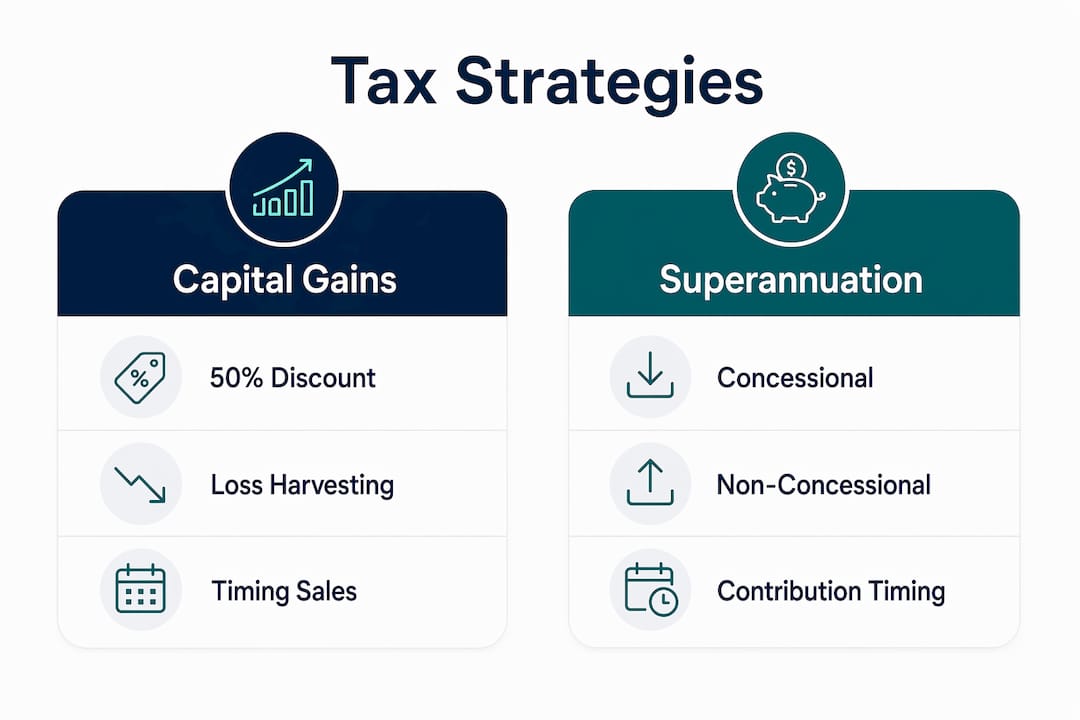

How can managing capital gains and losses optimise your tax position?

Capital gains tax (CGT) is one of the largest tax costs for Australian investors. Managing it well requires understanding both the rules and the timing of your decisions.

-

Understand the 50% CGT discount and its upcoming replacement. Assets held for more than 12 months currently attract a 50% CGT discount for individuals. The Australian Government is replacing this discount with cost-base indexation from 1 july 2027. That change requires a fundamental rethink of how you structure and time asset disposals.

-

Time asset disposals to align with lower-income years. Selling an asset in a year when your income is lower means the capital gain is taxed at a lower marginal rate. If you are approaching retirement or taking a career break, that window can be valuable.

-

Use tax-loss harvesting. Tax-loss harvesting lets you sell underperforming assets to realise capital losses, which offset your capital gains and reduce your net tax liability. Market volatility creates these opportunities regularly. Be aware of wash sale rules: the ATO may disallow a loss if the sole purpose of the sale was to obtain a tax benefit.

-

Know the difference between contract date and settlement date. The contract date determines the financial year in which a CGT event occurs, not the settlement date. A contract signed on 28 june triggers a CGT event in the current financial year, even if settlement happens in august.

-

Diversify to balance taxable returns. Holding a mix of growth assets, income-producing assets, and tax-advantaged structures reduces the concentration of taxable events in any single year.

| CGT strategy | Key benefit | Timing consideration |

|---|---|---|

| 50% discount (pre-2027) | Halves the taxable gain on assets held 12+ months | Dispose before 1 july 2027 to access current rules |

| Cost-base indexation (from 2027) | Adjusts cost base for inflation | Plan portfolio restructure before the change takes effect |

| Tax-loss harvesting | Offsets gains with realised losses | Best executed before 30 june each year |

| Income-year timing | Lowers marginal rate applied to gains | Align disposals with lower-income years |

For a detailed calculation of your current CGT exposure, the Alphaiq CGT calculator models your position under both the current discount rules and the incoming indexation method.

What role does superannuation play in optimising your tax position?

Superannuation is the most tax-effective savings vehicle available to most Australians. Used well, it reduces your taxable income today and builds wealth at a concessional tax rate over time.

- Concessional contributions cap. The concessional contributions cap is $30,000 for the 2025–26 financial year. Contributions within this cap are taxed at 15% inside the fund, which is significantly lower than the 32.5%, 37%, or 45% marginal rates that apply to most working Australians.

- Salary sacrifice. Arranging salary sacrifice contributions through your employer reduces your assessable income before tax is calculated. The saving is immediate and compounds over time inside the super environment.

- Personal deductible contributions. If your employer does not offer salary sacrifice, you can make personal contributions and claim a tax deduction directly in your return, provided you lodge a valid notice of intent with your fund before lodging your tax return.

- Carry-forward unused cap amounts. If your total super balance was below $500,000 on 30 june of the prior year, you can carry forward unused concessional cap amounts from the previous five years. This allows a larger deductible contribution in a high-income year.

- Tax treatment over age 60. Once you reach age 60, super withdrawals from a taxed fund are generally tax-free. Planning your transition to retirement around this threshold can significantly reduce your lifetime tax bill.

Pro Tip: Make your concessional contributions before 25 june each year, not on 30 june. Processing delays mean contributions made in the final days of june may not be credited until july, missing the current-year deduction entirely.

How can structuring investments and income streams improve tax efficiency?

Where you hold an asset matters as much as what you hold. Deliberate asset placement in low-tax environments or superannuation preserves tax alpha without requiring you to take on more investment risk.

Tax alpha is the additional after-tax return generated by structuring investments efficiently. It does not require picking better stocks or timing markets. It requires placing the right assets in the right structures.

| Asset type | Tax-inefficient structure | Tax-efficient structure |

|---|---|---|

| High-yield bonds or cash | Personal name (taxed at marginal rate) | Superannuation (taxed at 15%) |

| Australian shares with franking credits | Superannuation (credits may be wasted) | Personal name (credits offset tax payable) |

| Growth assets held long-term | Trust or company (no 50% discount in company) | Personal name or trust (access to 50% discount) |

| Property | Personal name (full rental income taxable) | Consider timing and structure based on income level |

Franked dividends deserve particular attention. When you hold Australian shares personally and receive fully franked dividends, the attached franking credits reduce your tax payable dollar for dollar. If your marginal rate is below the 30% company tax rate, you may receive a refund of the excess credits. This benefit is reduced or lost inside a company structure.

Avoiding unnecessary portfolio turnover also protects your tax position. Each sale is a potential CGT event. Investors who focus on after-tax returns rather than gross returns naturally trade less and retain more of their gains.

Pro Tip: Before restructuring assets between entities, model the tax cost of the transfer itself. Moving an asset from your personal name into a trust or company can trigger a CGT event at the point of transfer, which may outweigh the future tax saving.

For a broader view of how tax-aware investing compounds over time, the difference between a 2% and 3% after-tax return over 20 years is substantial.

Key takeaways

Effective tax optimisation requires year-round decisions across superannuation, capital gains, deductions, and investment structure, not a single action before 30 june.

| Point | Details |

|---|---|

| Act throughout the year | Year-round planning consistently outperforms last-minute EOFY adjustments. |

| Max out concessional super | The $30,000 cap offers a direct reduction in taxable income at a 15% tax rate inside the fund. |

| Know your CGT timing | Contract date, not settlement date, determines the financial year for capital gains events. |

| Place assets deliberately | Holding tax-inefficient assets in super and franked shares personally improves after-tax returns. |

| Prepare for 2027 CGT changes | The replacement of the 50% CGT discount with cost-base indexation requires portfolio review now. |

The mistake I see most often in tax planning

Most Australians treat tax planning as a once-a-year event. They gather receipts in june, lodge a return in august, and consider the job done. That approach leaves real money on the table every year.

The strategies that move the needle most, including timing asset sales, structuring contributions, and placing assets in the right entities, require decisions made months before 30 june. By the time you are sitting with your accountant in july, most of the opportunities for the prior year are already closed.

The other pattern I see regularly is an excessive focus on gross investment returns. An investor who earns 9% but pays 3% in tax each year is worse off than one who earns 8% and pays 1% in tax. Tax alpha is a real and measurable source of wealth. Ignoring it is the equivalent of leaving a consistent annual bonus unclaimed.

The upcoming CGT discount changes from 1 july 2027 make this even more pressing. Investors who have not reviewed their capital gains strategies in light of cost-base indexation are carrying a risk they may not have priced. The time to model that impact is now, not in june 2027.

Work with a tax adviser and a financial planner who communicate with each other. Integrated advice, where your investment structure, super contributions, and income timing are considered together, produces outcomes that siloed advice cannot. And use modelling tools that show you the numbers before you commit to a decision.

— Jonathan

How Alphaiq helps you model your tax position

Alphaiq is an Australian wealth intelligence platform built for self-directed investors aged 35–65 who want clarity on their financial position without paying for ongoing advice. The platform models capital gains, superannuation contributions, franking credits, and retirement income in one place, so you can see the after-tax impact of each decision before you make it.

The Alphaiq superannuation calculator lets you model different concessional contribution scenarios and see how each one affects your taxable income and projected retirement balance. For investors reviewing their position ahead of the 2027 CGT changes, the Alphaiq platform provides scenario simulation across asset structures and disposal timing. Real numbers, before you act.

FAQ

What does it mean to optimise your tax position?

Optimising your tax position means legally reducing your taxable income and structuring your finances to minimise the tax you pay. It involves year-round decisions across superannuation, investments, deductions, and income timing.

How much can I contribute to super to reduce my tax?

The concessional contributions cap is $30,000 for the 2025–26 financial year. Contributions within this cap are taxed at 15% inside the fund, which is lower than most marginal tax rates.

When does a capital gains tax event occur: contract date or settlement date?

The contract date determines the financial year for a CGT event, not the settlement date. A contract signed before 30 june triggers the gain in that financial year, even if settlement occurs after.

What is tax-loss harvesting and is it legal in Australia?

Tax-loss harvesting involves selling underperforming assets to realise capital losses that offset capital gains. It is legal in Australia, but the ATO may disallow losses where the sole purpose of the sale was to obtain a tax benefit.

How will the 2027 CGT changes affect my investment strategy?

From 1 july 2027, the 50% CGT discount for individuals will be replaced by cost-base indexation. Investors should model the impact on their current portfolio and consider timing disposals before the change takes effect.