Comparing multiple personal wealth planning tools while factoring in Australian tax, super and Age Pension rules often results in tedious spreadsheets and partial forecasts that miss local details. Many software options either hide advanced scenario testing and Monte Carlo simulations behind expensive subscriptions or skip critical rule-based modelling altogether. This guide reviews cost, simulation depth and privacy features across six Australian-focused wealth planning platforms so you can select one that fits your scenario testing needs and level of expertise.

Table of Contents

- AlphaIQ Wealth

- RetireConfident

- Canwi

- SuperCalc Pro

- ProjectionLab

- Property ROI Pro by Yieldley

- Detailed Comparison of Personal Wealth Planning Software

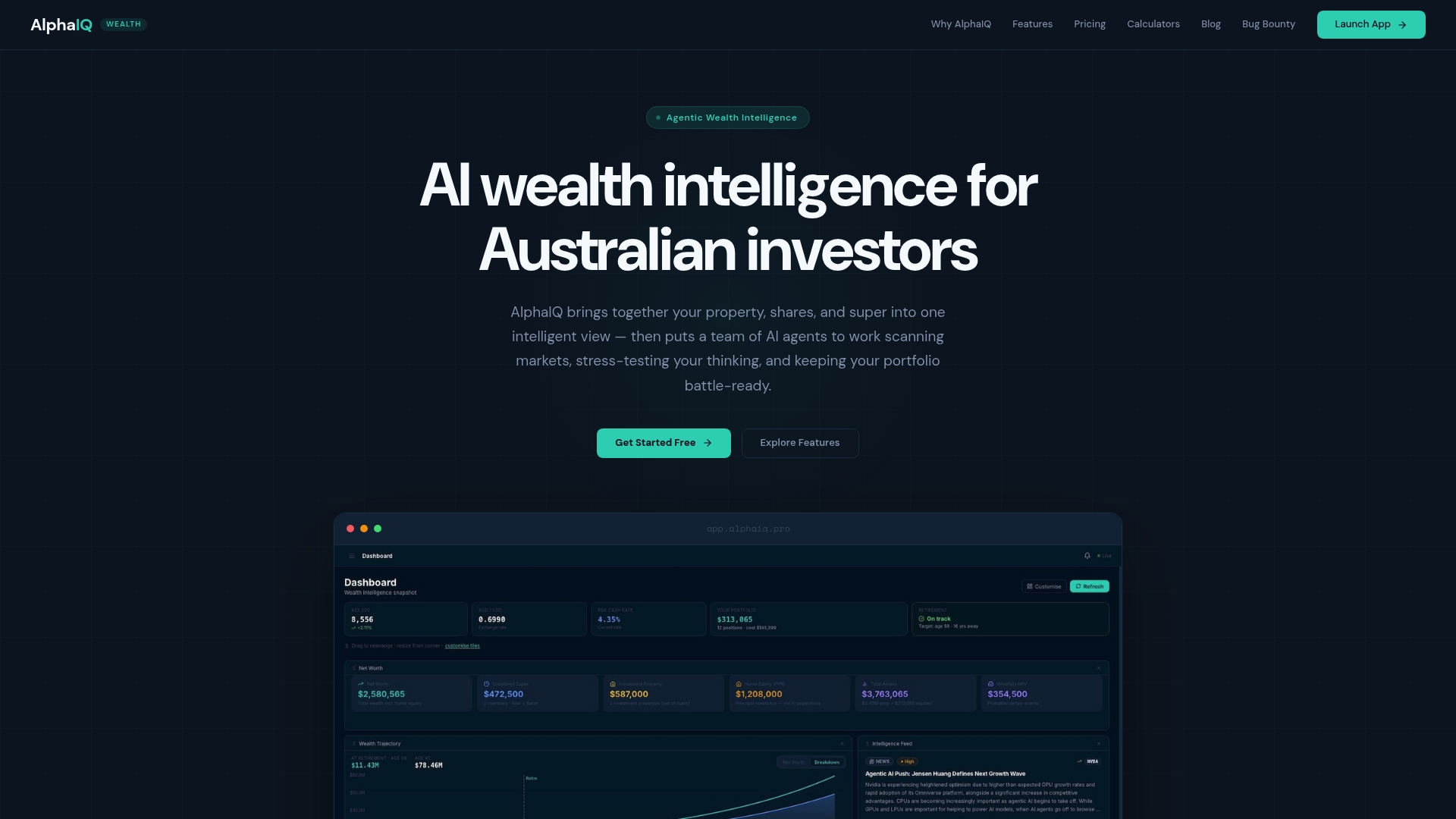

AlphaIQ Wealth

At a Glance

Proactive AI agents continuously scan markets and stress-test portfolios in real time while applying Australian tax and super rules. The system flags concentration risks and thesis issues so you spot problems before they become costly.

Core Features

- AI Thesis Interrogator that challenges stated assumptions and surfaces contradictory signals.

- Portfolio health scoring covering concentration, thesis clarity, and risk indicators tailored to property, shares, super and cash.

- Document vault with AI-extracted data to speed tax record keeping and scenario inputs.

- Scenario modelling that runs Australian tax, negative gearing, CGT and franking credits into retirement projections.

- Free calculators for quick, no-signup checks and limited daily AI feeds on the free tier.

Key Differentiator

The standout mechanic is continuous, proactive AI monitoring that treats signals as ongoing alerts rather than one-off reports. That live feed of earnings, property factors and macro events is tuned to Australian rules so the triggers relate directly to your tax and retirement position.

Pros

-

Tailored calculations for Australian legislation make tax and super outcomes easier to compare across scenarios. This reduces guesswork when you test a debt recycling or extra super contribution play.

-

Proactive alerts keep you aware of thesis drift and concentration before a single bad quarter cascades. Those early warnings are useful for investors juggling multiple properties or share holdings.

-

Multiplied asset coverage means you see property, shares, super and cash in one place. That single view saves spreadsheet stitching that typically takes hours each quarter.

-

Free calculators let you validate a quick idea without signing up. Use them to sanity check a tax or retirement question in under five minutes.

Cons

- The platform has a learning curve; advanced features and the breadth of outputs can feel overwhelming until you build a few scenarios and templates.

Who It's For

Self-directed Australian investors, property owners and SMSF trustees who want deep, tax-aware scenario modelling without paying ongoing advice fees. Best for people willing to engage actively with modelling tools rather than passive dashboards.

Unique Value Proposition

Australian-specific modelling is embedded into the workflow, with the vendor stating the calculations are validated through over 150 automated tests. That validation claim matters when you are comparing tax-aware outcomes across retirement, CGT events and gearing strategies.

Real World Use Case

A property investor models replacing an investment with a new dwelling. They run the swap through AlphaIQ, compare CGT timing, test negative gearing impacts and project retirement income under three tax timing options. The platform highlights the scenario that preserves the most franking and reduces taxable income in the transition year.

Pricing

Free tier plus Starter at $29 per month and Pro at $59 per month with annual billing options. The free tier includes basic tracking, AI questions and limited daily AI feeds; paid tiers expand scenario runs and daily intelligence.

Website: https://alphaiq.pro

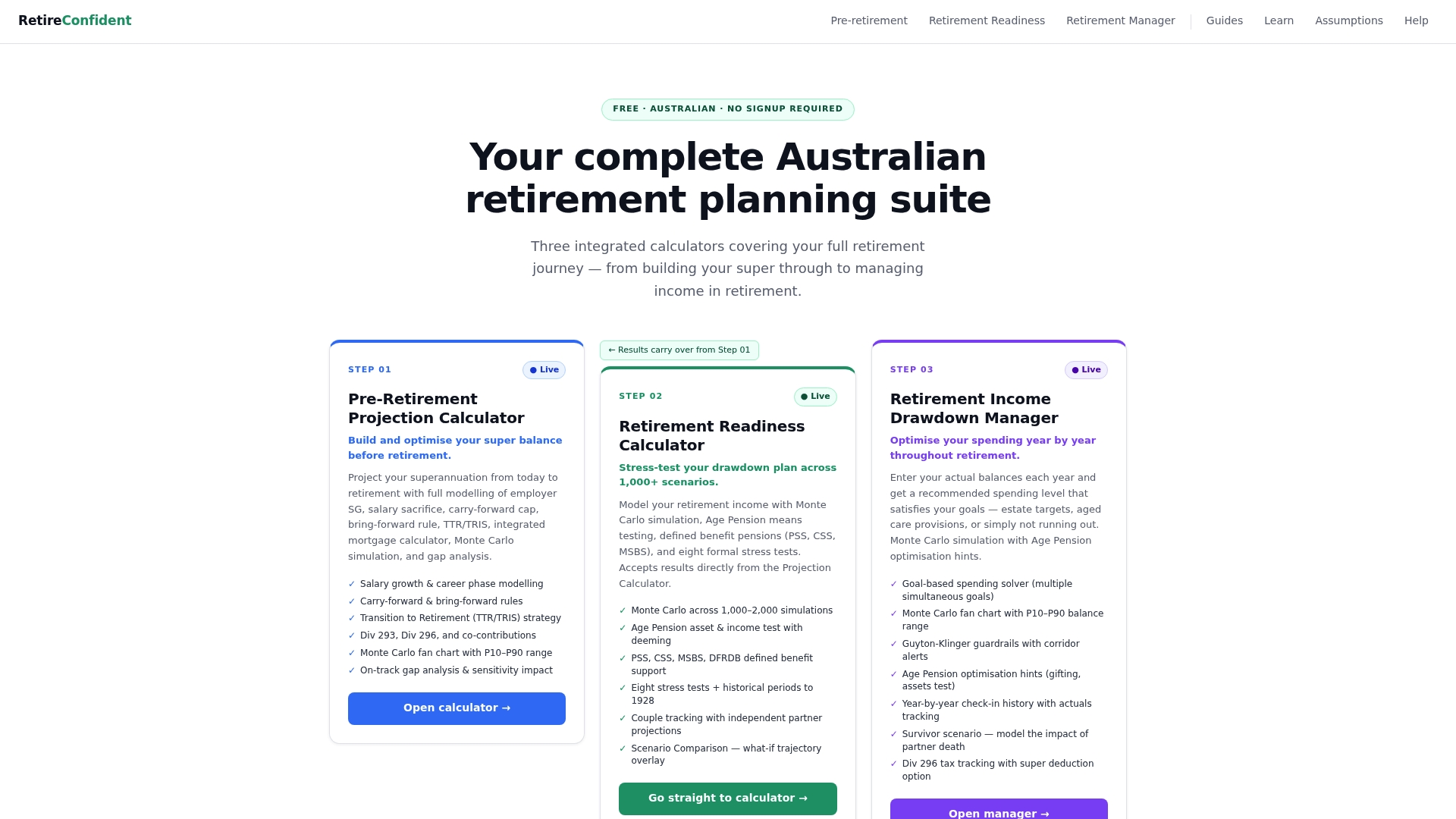

RetireConfident

At a Glance

RetireConfident's marketing materials advertise Monte Carlo simulation up to 2,000 scenarios, giving you probabilistic outcomes rather than a single forecast. The tool also models defined benefit pensions, Age Pension means testing and aged care costs, and it runs all calculations locally in your browser for added privacy.

Core Features

- Three integrated calculators: accumulation, retirement readiness, and drawdown management, with automatic handoff between phases.

- Full modelling of Australian retirement rules, including defined benefit pensions, Age Pension means testing, aged care costs, super contribution rules and tax scenario knobs.

- Monte Carlo simulations for probabilistic risk analysis and sensitivity comparisons across scenarios.

- Privacy-first design: all calculations execute locally in the browser, so no personal data is sent to servers.

Key Differentiator

RetireConfident uniquely combines detailed Australian retirement rules with a browser-based privacy posture. That means you can test dynamic withdrawal strategies, pension eligibility and aged care costs in one flow, without uploading client files to the cloud — a practical match for advisers who value data confidentiality and policy-specific modelling.

Pros

- Comprehensively models Australian-specific retirement mechanics, so you can compare defined benefit outcomes against super balances and Age Pension entitlements.

- The simulation approach above produces probabilistic ranges, which helps you quantify downside risk and spending shortfalls rather than rely on single-point estimates.

- Running locally preserves sensitive inputs on your device, which reduces client data exposure during adviser sessions.

- Seamless transfer between accumulation and drawdown phases keeps assumptions consistent when you move from saving to spending analysis.

- Detailed scenario comparison and sensitivity tools make it straightforward to test changes in retirement age, spending rates or contribution timing.

Cons

- The interface exposes many knobs and assumptions, creating a learning curve for casual users or advisers new to modelling.

- It does not model detailed capital gains tax or dividend imputation for non-super assets, instead offering approximate 'tax drag' controls.

- Some policy parameters are fixed in the tool, such as contribution caps and indexation settings, so results can diverge if rules change materially.

When It May Not Fit

If you need jurisdiction-agnostic modelling or an international client base, RetireConfident is narrowly Australian and will feel limited. Likewise, if your workflow requires line-by-line CGT or imputation credit modelling for taxable portfolios, the tool’s approximations will be a constraint. Casual users who want a simple retirement snapshot may find the depth overwhelming.

Who It's For

Australian pre-retirees and retirees who want to stress-test retirement plans, and financial advisers who model client pensions, super and Age Pension interactions. It suits users who prioritise privacy and policy-accurate projections over a minimalist, consumer-grade interface.

Real World Use Case

A 55-year-old approaching retirement uses RetireConfident to model super accumulation to age 67, then tests varying withdrawal rates and retirement ages. The adviser toggles aged care cost scenarios and sees how Age Pension means testing changes entitlements under different spending plans, all without sending client spreadsheets off-device.

Website: https://retireconfident.com.au

Canwi

At a Glance

Core features are free; Canwi Plus is listed at $39/month or $29/month billed annually. The tool uses Australian tax, super and capital gains rules and places side-by-side scenario comparison front and centre for modelling property and retirement outcomes.

Core Features

- Scenario modelling with drag-and-drop life events so you build alternate futures quickly and visually.

- Comparison view that places multiple financial futures side by side for direct, decade‑long comparisons.

- Built‑in Australian tax, super, CGT and benefit rules so assumptions reflect local regulation.

- Traceable calculations that let you drill into the maths behind a projection and check assumptions.

- Visualisation of income, wealth and cash flow across decades to highlight timing impacts.

Key Differentiator

Canwi’s standout feature is the combination of transparent, drill‑down calculations with native Australian rules. That pairing makes scenario outputs easier to justify in conversations with accountants or advisers, rather than relying on generic offshore models.

Pros

- Modern visual interface speeds analysis. The charts and side‑by‑side comparisons make differences obvious at a glance.

- Australian modelling covers super, tax and CGT, which reduces manual adjustment for local rules when you test property and retirement scenarios.

- Free standard account lowers the barrier to trial and lets users validate the tool before paying for advanced features.

- Traceable calculations help you and your adviser interrogate assumptions rather than accept opaque forecasts.

- Useful for preparing focused questions for a financial adviser or accountant before paying for personal advice.

Cons

- Third‑party review volume is limited, suggesting the user community is relatively small compared with more established platforms.

- Vendor content and public materials give only partial detail on edge‑case limitations and data import workflows.

- Advanced scenario features sit behind the Plus subscription, so power users will face ongoing subscription cost.

When It May Not Fit

If you run high‑volume modelling for many clients or need integrations with accounting packages, Canwi’s feature set and community size may feel restrictive. Likewise, teams that demand automated feeds from tax or investment custodians will find manual data entry slows throughput.

Notable Integrations

No third‑party integrations are explicitly listed in the vendor materials available for review.

Who It's For

Australians who prefer a DIY approach to financial planning and want transparent, local modelling for property, super and retirement. Property investors and self‑directed investors aged 35–65 who value hands‑on scenario testing will find it relevant.

Real World Use Case

A 45‑year‑old investor models early retirement against buying a second property. They toggle contribution rates, delayed retirement and different sale timings, then compare projected assets and pension outcomes to decide which strategy preserves cash flow and tax efficiency.

Pricing

Core features are free. Canwi Plus is advertised at $39/month or $29/month billed annually, which unlocks deeper scenario controls and premium outputs.

Website: https://canwi.com.au

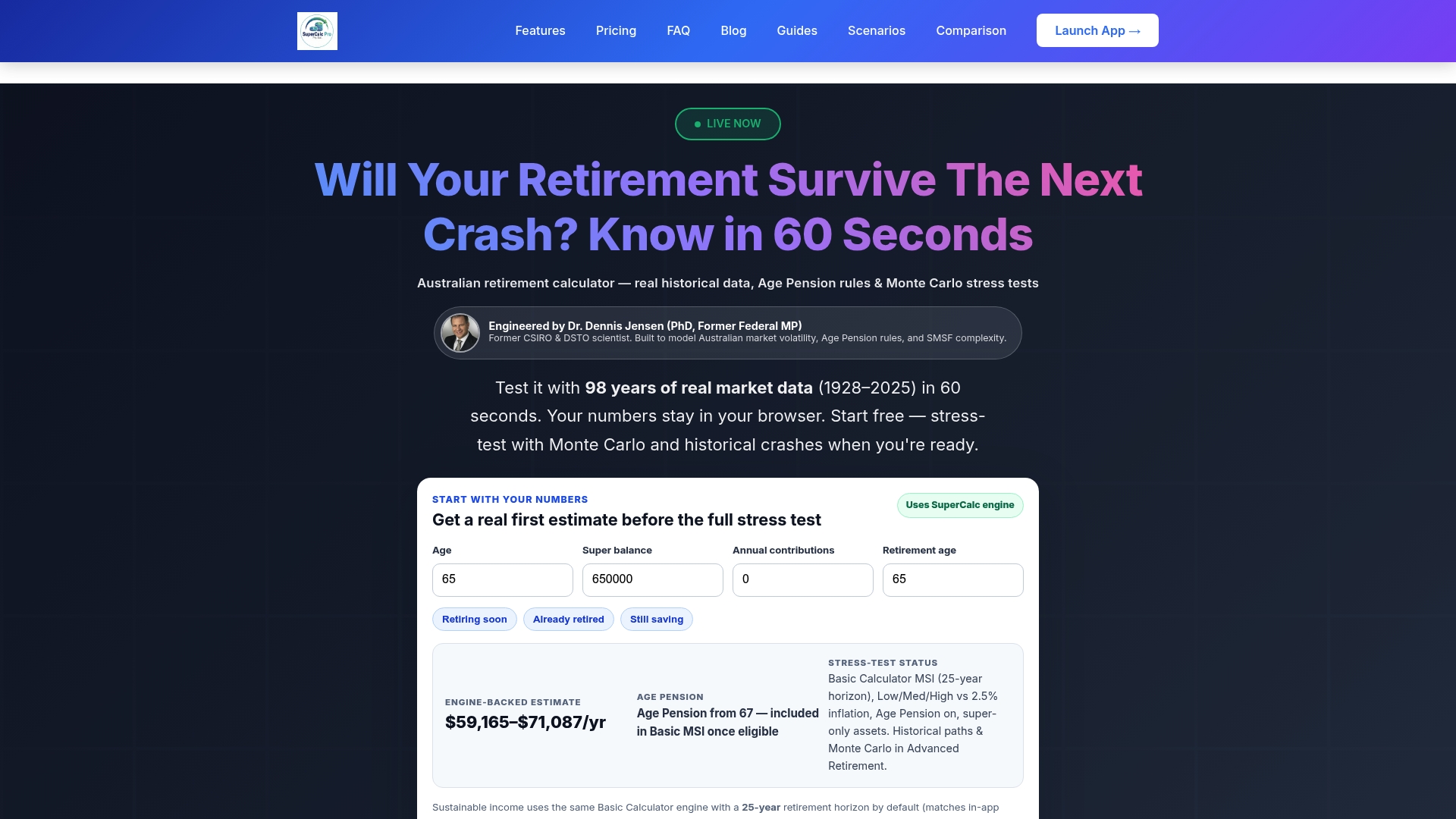

SuperCalc Pro

At a Glance

SuperCalc Pro's marketing materials state it draws on 98 years of real market data to power Monte Carlo runs and historical crash backtests. That dataset underpins its focus on retirement resilience rather than quick estimates.

The platform emphasises privacy with client-side calculations and targets serious scenario testing for Age Pension and SMSF planning.

Core Features

-

Monte Carlo simulations with 1,000-plus runs using the 98-year dataset the vendor advertises, enabling probability-based success estimates.

-

Historical backtesting against major market crises, including GFC and stagflation periods, to test sequence of returns risk.

-

Policy-aware modelling of Australian superannuation and Age Pension rules, plus phased retirement options for couples where retirement ages differ.

-

Advanced withdrawal, contribution and tax optimisation tools geared to SMSF trustees and high-net-worth individuals on higher tiers.

Key Differentiator

SuperCalc Pro pairs long-run historical data with policy-specific rules for Australia and models couples' phased retirement in detail. That combination of an extensive dataset plus couple-level modelling is uncommon in local retirement tools.

The platform also performs calculations client-side, which supports privacy for sensitive scenarios.

Pros

-

Depth for stress testing. The historical crash testing and probabilistic runs give you a defensible way to compare withdrawal strategies under tough past conditions.

-

Policy-accurate outputs. Age Pension and superannuation rules are built into the engine so your scenarios reflect Australian tax and benefit mechanics rather than generic assumptions.

-

SMSF-capable toolset. The product includes features aimed at trustees and advisers who need withdrawals, contributions and tax optimisation modelled precisely.

-

Privacy-first execution. Client-side calculations mean scenarios run in the browser and are not stored on vendor servers, which appeals to privacy-conscious users.

-

Report exports. You can produce PDF reports to share with an accountant or adviser without exposing raw data online.

Cons

-

Cost reflects the target market. The tiered pricing is aimed at serious planners and may feel expensive for casual users or those who want quick ballpark figures.

-

Learning curve. The platform assumes a level of financial literacy; non-technical users will take time to use advanced features effectively.

-

Feature gating. Some advanced SMSF tools and optimisation routines are locked behind higher subscription tiers, limiting access unless you pay more.

-

Educational only. The tool does not replace regulated financial advice or legal compliance checks, so professional guidance remains necessary.

When It May Not Fit

If you want a simple, fast retirement estimate for a single household, SuperCalc Pro is more than you need and slower to learn. If hiring a planner is already part of your process, you may prefer adviser-managed modelling rather than a subscription.

Small-scale users who prioritise low cost over scenario depth will find the pricing and tier model restrictive.

Who It's For

Australian retirees, SMSF trustees and financial professionals who require long-horizon scenario testing and policy-aware projections. The tool suits people who will spend time learning the engine and who need defensible, data-driven trade-offs.

Real World Use Case

An Australian couple models phased retirement where one partner retires at 60 and the other at 67. They test multiple withdrawal sequences across the historical crashes above and adjust contributions to maximise Age Pension access while tracking success probabilities over a 30-year horizon.

The couple exports PDFs to discuss with their accountant and fine-tune tax timing.

Pricing

Plans start at $14.99 per month for advanced features and rise to $39.99 per month for the tiers that include comprehensive SMSF tools and optimisation routines. Trial availability is described on the vendor site.

Website: https://supercalcpro.com.au

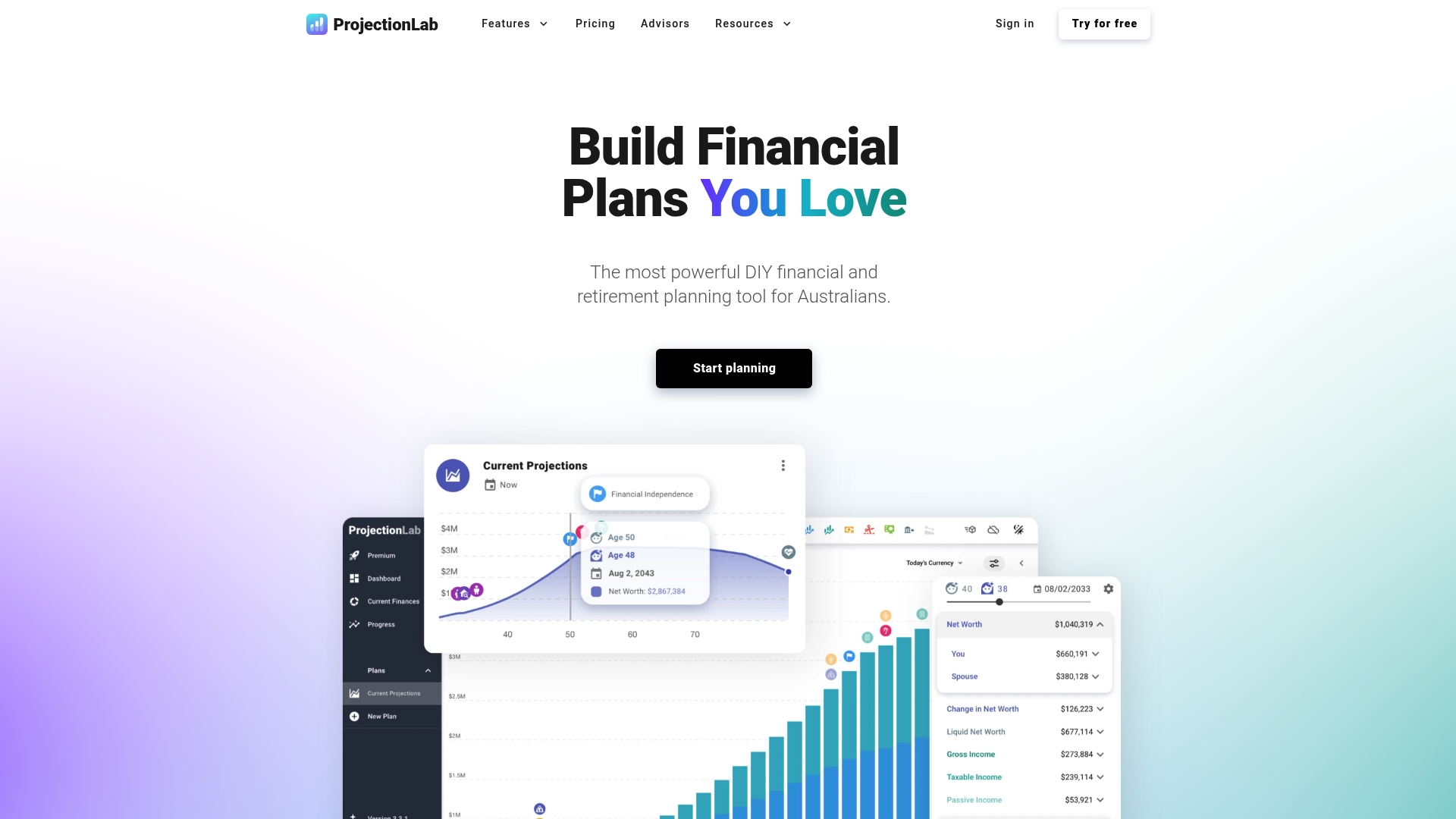

ProjectionLab

At a Glance

ProjectionLab includes native Australian account types such as Superannuation and does not require account linking, which makes it privacy-friendly for Australian planners. The interface emphasises scenario testing and Monte Carlo runs so you can compare long term outcomes for early retirement or estate plans.

Core Features

ProjectionLab focuses on retirement and cash flow modelling with tools tailored to Australian rules and tax treatment.

- Monte Carlo simulations to assess the probability of success across market variance.

- Sankey diagrams for cash flow visualisation so you can see money moving between accounts and goals.

- Tax analytics and estate planning modules that factor in Superannuation and cross border scenarios.

- Scenario testing for early retirement, large purchases and inheritance outcomes.

Key Differentiator

The tool is built specifically around Australian account types and offers international scenario support while deliberately avoiding account linking. Compared with AlphaIQ, ProjectionLab is narrower in scope and more simulation focused; it is a specialist modelling tool rather than an all-in-one wealth dashboard.

Pros

-

Highly detailed modelling makes it possible to test nuanced strategies for Superannuation and non Super accounts, which helps clarify trade offs between tax and timing.

-

No account linking reduces onboarding friction and keeps sensitive data offline, appealing for privacy conscious users and small advisory practices.

-

Scenario tweaks are fast once inputs are set. You can copy scenarios, change assumptions and instantly compare projected cash flows.

-

International scenario support lets Australians test UK or US tax situations without rebuilding models from scratch.

-

Active community feedback and user discussion help with advanced techniques and template sharing.

Cons

-

Initial setup requires time and attention to enter accurate balances, contribution schedules and tax assumptions before the outputs are useful.

-

The interface expects some financial literacy. Users without a basic grasp of tax treatment, investment returns or contribution rules will need guidance to interpret results.

-

Some advanced capabilities sit behind a paid tier. The more sophisticated estate and advisor tools are part of the subscription options.

When It May Not Fit

If you want automatic account aggregation and live bank feeds, ProjectionLab is the wrong choice because it intentionally avoids linking accounts. If you prefer a turnkey, hand holding experience, the learning curve here and the manual data entry will feel burdensome.

Who It's For

Australians planning for retirement or financial independence who want granular, scenario driven modelling. Also suitable for financial advisers who need a simulation engine to present tax aware retirement pathways without uploading client credentials.

Real World Use Case

A member aiming to retire at 58 builds scenarios with different savings rates, asset mixes and withdrawal sequences. They run Monte Carlo tests to compare failure probabilities, adjust Superannuation contribution timing and use the Sankey view to communicate expected cash flows to their adviser.

Pricing

Free tier covers basic modelling and scenario work. Premium at $129/year unlocks advanced tools and additional scenario types. Adviser level is $549/year for Pro features and client management workflows.

Website: https://projectionlab.com/australia

Property ROI Pro by Yieldley

At a Glance

A one-time $5 lifetime access fee unlocks Property ROI Pro's market-driven calculator and comparison tools — an unusually low entry point for property analysis. The vendor advertises results in under 5 seconds, a speed claim that shapes expectations around rapid screening.

Core Features

- Instant calculation of rental yield, ROI, cash flow, mortgage payments and stamp duty from basic inputs.

- Uses real market data as the basis for its estimates rather than relying solely on user-entered figures.

- Minimal input required: purchase price, rent and expenses produce key metrics in seconds.

- A free basic calculator is available for trial use before paying.

Key Differentiator

Property ROI Pro pairs a very simple interface with market-data-driven outputs aimed specifically at Australian investors. Where many calculators force spreadsheet export, this tool delivers immediate, comparable metrics for multiple properties without setup or templates.

Pros

- Fast screening. The speed claim above means you can check several properties during a site visit or auction recess, speeding decision cycles.

- $5 lifetime access makes experimenting with the tool low risk compared with subscription alternatives or paid advisory sessions.

- Market-based estimates reduce the manual work of sourcing comparable rents and stamp duty figures for an initial assessment.

- No spreadsheet skills required; the interface is focused on clarity so non-technical investors can read cash flow and ROI instantly.

- The free basic calculator lets you validate the UI and outputs before buying access.

Cons

- Depth is limited: the calculator handles basic scenarios but lacks multi-asset modelling, tax layering or detailed financing permutations.

- Not a substitute for professional financial planning or tailored tax advice; outputs are indicative rather than definitive.

- Early-stage product status means features will change as the vendor improves the tool, which may affect workflows you build around it.

When It May Not Fit

If you need scenario modelling across multiple properties with tax-aware projections, debt recycling or retirement income forecasts, this tool will be insufficient. Similarly, if you require compliance checks or legal structuring advice, you must complement it with expert services.

Who It's For

Individual Australian property investors who want quick, reliable screening metrics to shortlist opportunities. It suits buyers who prioritise speed and affordability over deep, bespoke financial modelling or adviser-level outputs.

Real World Use Case

You spot three nearby rentals on a weekend and want a rapid comparison. Enter address, purchase price and expected rent into Property ROI Pro; within seconds you get yield, cash flow and a rough ROI ranking to prioritise which property to inspect first.

Pricing

The vendor lists a one-time fee of $5 for lifetime access, plus a free basic calculator for trial users. That single-payment model removes ongoing subscription budgeting for investors who prefer pay-once tools.

Website: https://yieldley.com

Detailed Comparison of Personal Wealth Planning Software

The selection of personal wealth planning software necessitates careful consideration of each option’s specific focus and methodology. Below, we provide a detailed comparative analysis of the leading tools, highlighting unique strengths and trade-offs to guide decision-making.

Feature Coverage and Specialisation

AlphaIQ Wealth distinguishes itself with its proactive alert system that monitors Australian-specific portfolio indicators, offering real-time insights on market shifts and tax implications. In contrast, RetireConfident excels in privacy-conscious, browser-based modelling of retirement scenarios, focusing on probabilistic risk assessments. SuperCalc Pro supplements scenario-testing fidelity with historical return analysis, producing stress tests for retirement planning.

Usability and Pricing Accessibility

While AlphaIQ Wealth includes extensive scenario modelling capabilities tailored to Australian financial rules, the learning curve necessitates user dedication to maximise benefits. For more straightforward needs, Property ROI Pro offers quick, simplified property-specific calculations at a significantly lower upfront cost. Canwi balances accessibility and functionality with its visual comparison tools, which streamline scenario evaluations without overly technical inputs.

Best Fit Scenarios

- AlphaIQ Wealth: For self-directed investors requiring integrated portfolio supervision across diverse asset classes with tax-aware scenario planning.

- RetireConfident: Preferable for financial advisers prioritising data privacy during the modelling of retirement and pension scenarios.

- Canwi: Beneficial for users valuing scenario visualisation and requiring local Australian rule adjustments for financial forecasting.

- Property ROI Pro: Suitable for rapid property investment screening during auctions or time-sensitive purchasing decisions.

Our Pick

Among the reviewed options, AlphaIQ Wealth proves most advantageous for Australian investors seeking centralised asset supervision combined with directly applicable tax and superannuation calculations. It is less suited, however, to users requiring minimalist interfaces or international tax adjustments. For these cases, the alternatives detailed above merit strong consideration based on specific user priorities.

Personal Wealth Planning Software Comparison

Select the ideal platform by evaluating their distinctive features, user focus, and limitations.

| Product Name | Core Features | Key Differentiator | Best For | Pricing | Notable Limitation |

|---|---|---|---|---|---|

| AlphaIQ Wealth | AI-driven portfolio analysis, tax and retirement planning, free calculators | Australian-specific proactive AI monitoring and risk alerts | Self-directed Australian investors and SMSF trustees | Free tier, $29/month for Starter, $59/month for Pro | Initial learning curve for advanced features |

| RetireConfident | Monte Carlo simulations, Australian retirement mechanics, local browser privacy | Privacy-first design with comprehensive Australian retirement modelling | Australian pre-retirees and retirees | Not disclosed | Complex interface for casual users |

| Canwi | Scenario modelling, Australian tax and retirement rules, side-by-side finances | Transparent, drill-down calculations with local compliance | Australians aged 35–65 preferring DIY financial planning | Free tier, $39/month or $29/month billed annually | Limited third-party reviews and documentation |

| SuperCalc Pro | Monte Carlo runs, sequence of returns historical backtests, SMSF optimisation | Historical crash testing backed by extensive datasets | Australian SMSF trustees and data-driven planners | $14.99/month basic, $39.99/month higher tiers | Steep learning curve for casual users |

| ProjectionLab | Monte Carlo models, cash flow scenarios, estate planning tools | Privacy-focused Australian account modelling with international support | Australians planning retirement with granular scenarios | Free tier, $129/year Premium, $549/year Adviser | Time-intensive data entry for setup and interpretation |

Take Control of Your Wealth with AlphaIQ

If you are exploring homeyield.com.au alternatives, you likely want clear insights into managing your investments, superannuation, property, and retirement planning all in one place. AlphaIQ is tailored for Australian self-directed investors aged 35–65 who want to stop guessing and start using tax-aware scenario modelling that reflects real Australian rules and maximise your financial outcomes with confidence.

Experience proactive AI-powered portfolio health scoring and real-time alerts designed to catch risks before they impact your wealth. Visit AlphaIQ now to model your capital gains, debt recycling strategies, and franking credits efficiently. Import your investment details and see tax and retirement projections clearly within minutes.

Frequently Asked Questions

What makes Alphaiq a strong choice for personal wealth planning?

Alphaiq excels in proactive AI monitoring, which continuously scans markets and stress-tests portfolios in real time. This feature allows users to spot concentration risks and thesis issues before they lead to significant losses. Engage with Alphaiq to utilize these real-time insights for your investment strategies.

How does Alphaiq compare to RetireConfident in terms of retirement planning?

RetireConfident offers comprehensive Monte Carlo simulations that model defined benefit pensions and aged care costs, providing a range of probabilistic outcomes for planning. In contrast, Alphaiq focuses on ongoing alerts and alerts regarding thesis drift and concentration risks for self-directed investors. If you are looking for dynamic scenario modelling shaped by Australian tax rules, Alphaiq might suit your active investment approach better.

Which platform provides privacy-first features for financial planning?

RetireConfident operates with a privacy-first approach, executing all calculations locally in the browser, ensuring no data is sent to servers. In contrast, Alphaiq’s unique feature is continuous AI monitoring, providing real-time intelligence while managing Australian tax-aware scenarios. Evaluate how critical data privacy is for your financial planning needs, as both tools cater to different aspects of user concerns.

Can I use Alphaiq if I need advanced scenario comparisons?

Alphaiq is suitable for users who want tailored calculations for Australian regulations while efficiently covering multiple assets. Its portfolio health scoring helps assess concentration and risk indicators across various investment types. If you frequently test different financial scenarios, Alphaiq’s capabilities will give you clear insights into your options.

What advantage does Canwi have for DIY financial planning?

Canwi provides a user-friendly visual interface for scenario modelling, allowing users to build alternate financial futures quickly. While Alphaiq focuses on proactive monitoring and alerts, Canwi's drag-and-drop features may appeal to those who prefer hands-on experimentation. Consider your preferred style of financial planning when exploring these alternatives.